Buried Deep in Chevron's Q3 Earnings Are Signs of Life

On the surface, Chevron's (NYSE: CVX) earnings results pretty much followed the track of prior results: Lower oil and gas prices continued to weigh on upstream profits that were largely offset by downstream operations. But if you look deeper into the results, you can start to see the effects of management's decisions over the past several years to cut costs and make a leaner, meaner Chevron for the upswing.

Here's a quick look at the company's results, how Chevron is doing more with less, and how that will play out over the coming quarters.

Image source: Chevron investor presentation.

Chevron's results: The raw numbers

| Metric | Q3 2016 | Q2 2016 | Q3 2015 |

|---|---|---|---|

| Revenue | $30,140 | $29,282 | $34,315 |

| Net income | $1,283 | ($1,470) | $2,037 |

| Earnings per share | $0.68 | ($0.78) | $1.09 |

| Operational cash flow | $5,311 | $2,531 |

$5,360 |

Data source: Chevron earnings release. Figures in millions, except per-share data.

After a few quarters in a row where Chevron took several billion dollars' worth of asset writedowns and goodwill impairments, this is the first quarter in a while in which we get to see a "clean" earnings report from the company. Without those charges, Chevron is showing that it's still generating profits, albeit modest ones. The one part of the business that continues to drag things down from a profitability standpoint is its U.S. upstream production.

Data source: Chevron earnings releases. Author's chart.

Looking at those numbers in isolation would make it seem that the company is still struggling with eking out a profit from its U.S. operations. If you dig a little deeper, though, you can start to see some of the effects of Chevron's huge cost-cutting efforts. The best way to show this progress is the price realizations the company received for oil and gas this past quarter and the prior year.

| Price Realization For: |

Q3 2016 | Q3 2015 |

|---|---|---|

| U.S. crude | $40.10 | $45.56 |

| U.S. natural gas | $1.89 | $1.96 |

| International crude | $41.08 | $44.85 |

| International natural gas | $4.18 | $4.68 |

Data source: Chevron earnings release. Crude oil prices are per barrel, and natural gas prices are per thousand cubic feet.

So even though Chevron averaged 10% less revenue per barrel equivalent of production, it was able to improve upstream earnings by $405 million.

The one stain on Chevron's earnings is the continued dismal cash-flow gap. The company's operational cash flows are still well short of its capital spending, especially after it committed to the$36.8 billion expansion of theTengiz project in Kazakhstan with ExxonMobil (NYSE: XOM). This past quarter alone, Chevron spent $2 billion on the expansion.

As a result of this additional spending, the company took on another $500 million in debt for the quarter, and its debt-to-capital ratio jumped to 23.7%.

What happened with Chevron this quarter?

- Overall upstream production was down slightly, from 2.54 million barrels of oil equivalent per day (mmboe/d) in 2015 to 2.51 mmboe/d this past quarter. It should be noted, though, that a large portion of this change was from turnaround activity at Tengiz. civil unrest in Nigeria that has shut in production, and asset sales in the Gulf of Mexico.

- Management expects production to be in the range of 2.65 mmboe/d to 2.7 mmboe/d by the end of the year, thanks to a completed turnaround at Tengiz, ramp-ups at the Jack/St.Malo platform and Gorgon LNG facility, and completed turnaround activity at Angola LNG.

- Speaking of Gorgon, Train 2 of the three-train facility came online at the end of October. It expects the final train to be up and running by the second quarter of 2017. Its sister facility, Wheatstone, expects to ship its first cargoes mid-2017.

- Asset sales for the first nine months of the year have totaled $2.2 billion. Management says it's confident it can meet its asset sales target for the year of $5 billion to $10 billion, but that's unlikely unless we see some major sales in the last two months of the year.

- Chevron's board of directors approved a $0.01 increase in the company's quarterly dividend. It may be a token increase, but it's enough to keep the company's streak of 29 straight years of dividend payments alive without putting too much of a dent in the company's cash flow.

What management had to say

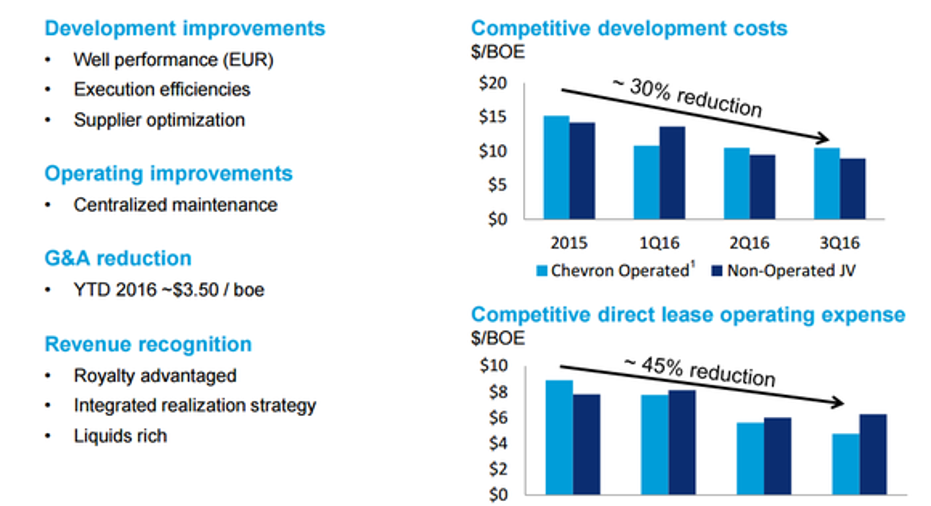

Typically, Chevron's earnings releases and press conferences are rather dull affairs, but this quarter, the company went into quite a bit of detail about its U.S. shaleproduction in the Permian Basin. Aside from its massive holdings in the basin -- north of 2 million acres -- the company has been driving down costs rather quickly. According to Bruce Niemyer, vice president of U.S. mid-continent operations:

Image source: Chevron investor presentation.

Thanks to these efficiency gains, Chevron is ahead of its production targets for shale without significant additions to its capital spending:

Image source: Chevron investor presentation.

10-second takeaway

There are some good things coming out of Chevron right now that suggest it's getting back to profitability. The most encouraging sign is the operational cost reductions that have drastically improved upstream results compared with this time last year. At the same time, the company is still struggling with a capital spending gap that's increasing its debt levels to their highest in over a decade. Hopefully, as oil prices improve, this funding gap will repair itself soon and the company can focus on spending within its means and trimming that debt load.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Tyler Crowe owns shares of ExxonMobil.You can follow him at Fool.comor on Twitter, @TylerCroweFool.

The Motley Fool owns shares of ExxonMobil. The Motley Fool recommends Chevron. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.