Bond ETF: How to Pick a Great Bond Fund

Image source: Getty Images.

Low-fee exchange-traded funds can be excellent bond funds because they are inexpensive, diversified across thousands of bonds in an index, and easy to buy and sell. But there are some risks -- fixed income ETFs have to be picked carefully.

Here are four things to look for before buying a bond ETF.

1. Credit risk

Buying a good bond ETF isn't just about picking the ETF with the highest yield. The saying that high returns can only be achieved by taking higher risks is absolutely true.

When surveying a bond ETF, I like to look at the ETF's holdings by credit rating. Bonds are rated on a sliding scale from D (bonds in default) to AAA (the lowest-risk bonds). While credit ratings agencies occasionally get things very wrong -- some highly rated bonds performed horribly during the financial crisis -- as a whole, bond ratings tend to be very accurate in forecasting relative risk. Bonds that get higher ratings have defaulted less frequently than bonds with low ratings.

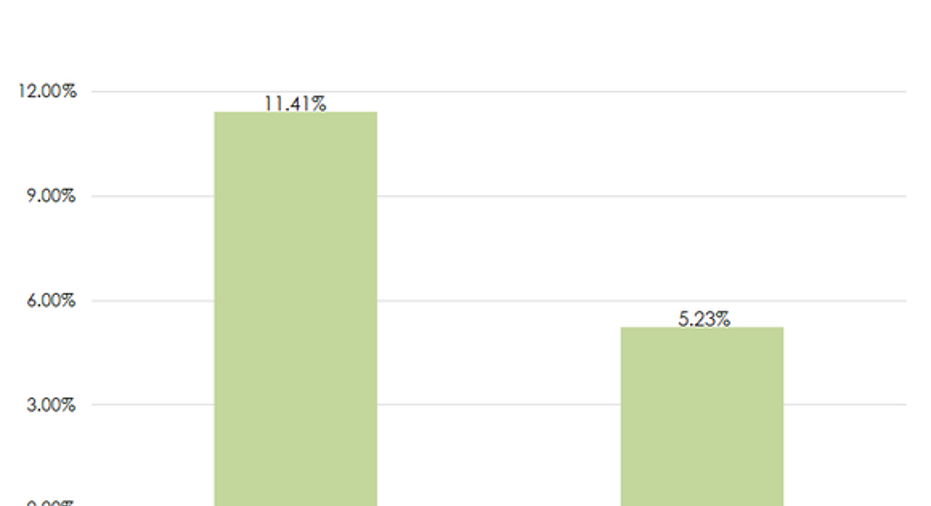

Bond ETF yields can be deceivingly high, as losses tend to occur in spurts. The chart below shows that credit cycles generally follow business and market cycles. In good years, riskier bond funds will provide high yields with very low losses. In bad years, however, defaults can erase more than a year's income. Note that losses on investment-grade and junk bonds run in cycles, but defaults and losses are much more severe for junk bonds than investment-grade bonds.

Image source: Vanguard research on junk bonds.

2. Interest rate risk

Bond prices have an inverse relationship with interest rates. When interest rates rise, bonds fall in value. When interest rates fall, bonds rise in value. How much bonds rise or fall due to interest rates varies based on the duration of any given bond, or the average amount of time it will take for the bond to pay all of its expected cash flows.

Duration can be used to estimate the impact of rising and falling interest rates, and you'll find this metric for any bond ETF in its prospectus, annual report, or on the fund sponsor's website. If a bond ETF has a duration of four years, this tells us that a 1% increase in interest rates would result in a 4% decrease in the ETF's value. Likewise, a 1% decrease in interest rates should result in a 4% increase in the ETF's value.

Consider two bond ETFs as an example. Vanguard's Short-Term Bond ETF (NYSEMKT: BSV) has an average duration of 2.8 years. Vanguard's Long-Term Bond ETF (NYSEMKT: BLV) has an average duration of 15.7 years.

Since the start of 2016, interest rates have broadly decreased, and long-term interest rates have decreased the most, relatively speaking. Not surprisingly, the short-term bond ETF has increased very little, while the long-term bond ETF has performed spectacularly. The fund's average duration explains this difference in performance in 2016, a year in which interest rates have gone down.

3. The underlying index

Almost all exchange-traded funds are index funds. That is to say, the bond ETFs do not employ credit analysts or portfolio managers to pick bonds. Instead, they seek to track an index of bonds, and generate good returns by lowering their own costs, which results in lower fees for investors. You should always take a look at the index a bond ETF seeks to track.

Many investors simply buy an ETF that broadly invests in investment-grade rated bonds of all types. Two popular ETFs that do this are the iShares Core US Aggregate Bond ETF (NYSEMKT: AGG) and the Vanguard Total Bond Market ETF (NYSEMKT: BND). These ETFs hold thousands of investment-grade rated bonds, a majority of which are issued or backed by the U.S. government. These funds are relatively safe and provide for a low yield since most of their money is in super-safe U.S. government securities.

Other ETFs find slightly higher yields by investing in investment-grade corporate bonds, excluding only government bonds. The Vanguard Intermediate-Term Corporate Bond ETF (NYSEMKT: VCIT) is a good example of a bond fund that does just that.

These funds have different investment portfolios because they track different indexes. The total bond market funds track the Barclays U.S. Aggregate Bond Index. Vanguard's Intermediate-Term Corporate Bond ETF tracks the Barclays U.S. 5-10 Year Corporate Bond Index. A bond ETF will only be as good as its underlying index.

4. Fees

Bond fund fees can be deceivingly low. The average bond fund carries a lower expense ratio than the average stock fund, but fees still add up significantly.

Bonds have a lower expected return than stocks.If we assume the long-run return on bonds is perhaps 4% or 5%, then a fund that carries a 1% expense ratio would eat up 20%-25% of pre-fee returns. That's simply too much.

What's a good fee to pay? It's all relative, but data from the Investment Company Institute suggests that the average bond index fund carries an expense ratio of 0.10% per year.That would be a good target for a bond fund to fall under,since the lower returns of bonds necessitate that you pay less in fees.

All in all, you can avoid the biggest pitfalls of bond ETF investing if you keep the above four things in mind. Always weigh the yield of any bond ETF against the credit and interest rate risk of a bond fund, make sure you understand the index a bond ETF seeks to track, and perhaps most importantly, make sure you aren't paying too much to own a bond ETF. If you do those four things, you'll do just fine.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

Jordan Wathen has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.