Better Buy: United Technologies or Honeywell International?

United Technologies or Honeywell International ? Both companies have heavy exposure to aerospace and global construction markets and therefore face similar headline risks. In addition, both are going through transition periods in 2016. The changes will compromise revenue and earnings in 2016 but are designed to ensure long-term earnings and cash flow generation. So which stock will win out this year?

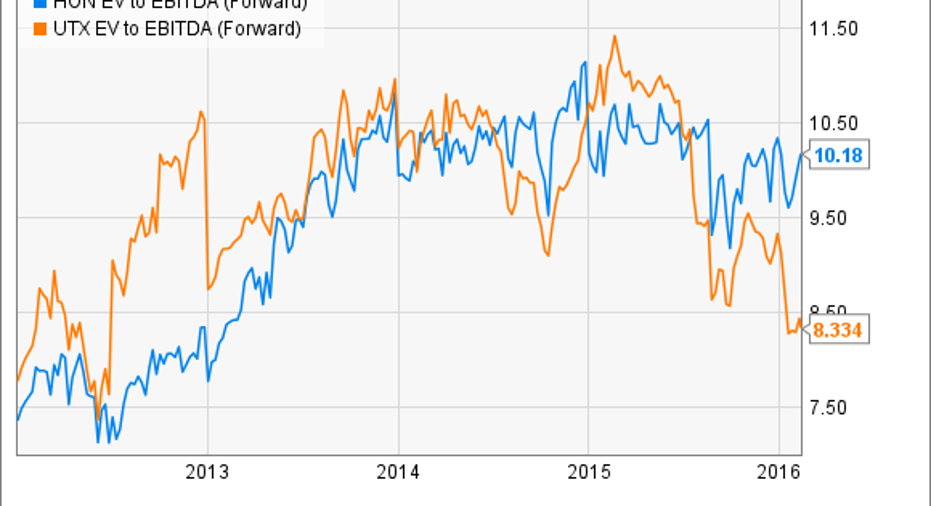

ValuationsA look at valuations shows a premium for Honeywell's stock. EV/EBITDA represents enterprise value (market cap plus net debt) over earnings before interest, tax, depreciation, and amortization -- a useful way to compare two companies with different debt loads.

HON EV to EBITDA (Forward) data by YCharts.

In a nutshell, United Technologies underperformed Honeywell last year because the company was forced to lower earnings estimates for two reasons:

- Lower than previously expected commercial aftermarket sales, principally from provisioning sales on Boeing Company's787 plane.

- Weak Otis elevator sales in Europe and particularly in China.

With those issues arguably in the past now, is United Technologies now the value pick?

Risks and opportunitiesBefore hitting the buy button, it's worth considering the risks and opportunities facing both companies in 2016. The second chart shows forward EV/EBITDA so it includes consensus estimates, which usually follow company guidance quite closely. The two key questions for 2016 are:

- What does the guidance mean in the long-term context of each company's value?

- What are the risks to both companies' hitting guidance?

I've discussed how United Technologiesand Honeywell are shaping up for 2016. The key points are as follows.

United Technologies

- Organic revenue growth of 1% to 3%.

- Adjusted EPS target of $6.30 to $6.60, implying 0% to 5% growth.

- Free cash flow conversion from net income of 90% to 100%.

It's not going to be a banner year for the company's headline numbers, and management is expecting significant operating profit declines in three of four segments.

However, some of the reasons for the declines are along-term positive:

- Management is trying to increase Otis' installed base togenerate more profitable long-term services demand.

- Pratt & Whitney is facing a year of negative engine margin from its geared turbofan engine, as it ramps up production of the new engine -- an act that will generate long-term services demand.

- Aerospace systems sales mix is shifting to newer products, which will have an initially lower margin than its more mature products.

The company undoubtedly faces headwinds with Otis in China (a key market), and ramping up production on aero engines is never an easy task. Meanwhile, the merger of Tyco and Johnson Controlscould put pressure on United Technologies' fire security and climate controls products, in which it competes, respectively, with Tyco and Johnson Controls.

However, you can still think of this as being a year in which the groundwork is laid for years of profitable growth ahead.

Honeywell InternationalThe company's outlook is best summarized in a graphic from its first-quarter earnings presentation. Its core organic sales growth is similar to United Technologies', but margin expansion is leveraging EPS and free cash flow growth -- all in line with its five-year (2014-2018) plan.

Moreover, underlying free cash flow is better than it looks. Honeywell is investing in growth as part of its plan. As such, free cash flow conversion from net income in 2015 was around 91%, but management expects to get back to a 100% conversion rate by 2017. In other words, a combination of margin expansion and relatively fewer capital expenditures in future years should see Honeywell's free cash flow expand in the future.

In common with United Technologies and General Electric , Honeywell faces some near-term headwinds in its aerospace operations -- Honeywell is giving incentives to position itself on new aerospace programs. Its performance, materials, and technologies segment also faces risks because of its oil and gas exposure, and automation and controls solutions has China exposure.

If you're worred about Boeing's recent production rescheduling, here's how Honeywell CEO David Cote answered a question on the subject on the recent earnings call:

The pickFor United Technologies, Otis' China exposure is a concern, but Honeywell will also be hit if China's growth dives. Similarly, bothhave exposure to aerospace and construction, while Honeywell is more exposed to oil and gas. Undoubtedly, Honeywell has an enviable recent history of execution, and Pratt & Whitney's geared turbofan production ramp will also create challenges.

However, General Electric is also ramping up production of its LEAP engine, and its management is confident of using the industrial Internet to help reduce unit cost production in the future -- a salutary reminder that United Technologies can also use new technologies to cut engine program costs.

All told, on a risk/reward basis, I think United Technologies can outperform Honeywell from here.

The article Better Buy: United Technologies or Honeywell International? originally appeared on Fool.com.

Lee Samaha has no position in any stocks mentioned. The Motley Fool owns shares of General Electric Company and Johnson Controls,. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.