Better Buy: Skyworks Solutions, Inc. vs. Qualcomm

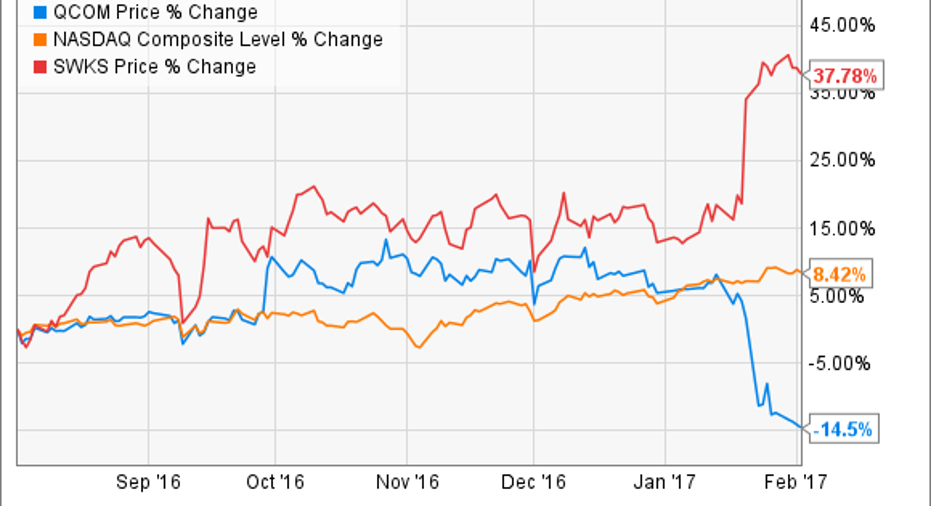

Though investing is filled with uncertainty, occasionally, the answer to a certain question is as clear as day. Today, that seems to be the case in comparing semiconductor companies Skyworks Solutions (NASDAQ: SWKS) and Qualcomm (NASDAQ: QCOM), as the recent movements of their stock prices suggest.

Clearly, the market had voted in favor of Skyworks' stock over that of Qualcomm lately, but is that trend likely to continue? In this article, we'll run Skyworks Solutions and Qualcomm through a three-part analysis to better understand which company's stock is the better buy today.

Qualcomm vs. Skyworks: Financial fortitude

Comparing the solvency and liquidity metrics for Qualcomm and Skyworks, the two chip companies are both in fine financial shape, as you can see from the following chart.

|

Company |

Cash & Investments |

Debt |

Cash From Operations |

Current Ratio |

|---|---|---|---|---|

|

Qualcomm |

$29.7 billion |

$11.6 billion |

$6.0 billion |

2.0 |

|

Skyworks Solutions |

$1.1 billion |

$0 |

$1.2 billion |

7.2 |

Data sources: Qualcomm and Skyworks investor relations.

In terms of their near-term liquidity, Qualcomm and Skyworks each carry far more current assets than current liabilities, although Skyworks' deserves special praise for its particularly conservative quick ratio. Neither company appears to present much in the way of liquidity risk. Furthermore, Qualcomm and Skyworks Solutions both employ conservative capital structures. Qualcomm can easily service its outstanding obligations from either its current cash balance or its operating cash flows. Here too, though, Skyworks wins since it eschews borrowing altogether and still generates plenty of cash.

It also briefly deserves noting that Qualcomm's balance sheet composition will certainly change when its pending acquisition of Internet of Things (IoT) chipmaker NXP Semiconductor closes at some point this year. Qualcomm will finance the deal using its overseas cash reserves and by issuing bonds. Though Qualcomm management reiterated that the deal shouldn't interfere with its ability to meet its various obligations -- notably its dividend -- Skyworks' impressive financial footing and Qualcomm further leveraging its balance sheet, albeit for a productive propose, earn Skyworks a clear win in this category.

Winner: Skyworks Solutions

Image source: Getty Images.

Qualcomm vs. Skyworks: Competitive analysis

Skyworks and Qualcomm both enjoy powerful business models, though each has a few important risks that could derail their investment theses under the wrong circumstances.

Qualcomm is the leading provider of mobile application processors and baseband chips, which enable mobile devices to connect with 3G and 4G networks. Its Qualcomm CDMA Technologies (QCT) segment produces about two-thirds of the company's revenues and generates pre-tax margins that typically hover in the high teens. Qualcomm's true profit center, though, is its Qualcomm Technology Licensing (QTL) segment. Thanks to Qualcomm's pivotal role in developing 3G and 4G standards, the company has historically been able to generate royalty revenue from every device produced by mobile OEMs. Though small a percentage of its total sales, this QTL's royalty revenue is essentially pure profit, enjoying an 85% pre-tax margin.

Critically, Qualcomm's patent licensing practices have come under immense pressure from a host of lawsuits in recent years, which creates a genuine amount of doubt as to the durability of Qualcomm's profit center, adding a substantial amount of risk to a company with an otherwise attractive business model.

Looking to Skyworks, the company manufactures over 2,500 chips, including analog semiconductors, switches, and amplifiers, to a roster of over 2,000 customers. At a high level, Skyworks' competitive advantages lie in its unique ability to bundle an increasing number of complex connectivity functions into a single, space-saving chip. This unique ability made Skyworks an invaluable supplier to smartphone and tablet makers, and the company has been handsomely rewarded as mobile devices have proliferated in the past decade.

Looking to the future, Skyworks sees an opportunity to provide similar solutions to the booming Internet of Things market. By the year 2020, the company believes there will be 1 billion personal computers, 2 billion smartphones, and a whopping 43 billion Internet-of-Things-enabled devicesoperating globally, and it hopes to provide chips for as many of these as possible. Though the future indeed looks bright, it's important to note that Apple accounts for 40% of Skyworks' revenue today, so its performance is disproportionately influenced by Apple's component orders.

Winner: Skyworks

Qualcomm vs. Skyworks valuation analysis

Turning to the third section, here's a quick snapshot of three of the most commonly used valuation metrics for both Skyworks and Qualcomm.

|

Company |

P/E |

Forward P/E |

EV/EBITDA |

|---|---|---|---|

|

Qualcomm |

13.9 |

11.2 |

9.3 |

|

Skyworks Solutions |

19.3 |

24.8 |

18.4 |

Data source: Yahoo! Finance.

In reviewing the metrics, both Skyworks and Qualcomm largely seem appropriately valued. Qualcomm is expected to grow 1.2% this year and 2.8% next year. This kind of tepid top-line expansion combined with its current legal overhang justifies Qualcomm trading at a fairly compressed multiple. Analysts expect Skyworks to grow sales 8.6% this year and 10.3% next year. Though above average, this doesn't merit the same kind of aggressive premium we see right now at other semiconductor names like NVIDIA. Though not the sexy call, both companies look fairly valued today, in my eyes.

Winner: Tie

And the winner is...Skyworks

At the end of the day, Qualcomm's outsized legal risk loomed fairly large in this decision. Though Qualcomm maintains its innocence, an adverse ruling could materially impact the company's financial performance or, worse yet, its highly lucrative business model. Meanwhile, Skyworks' outlook remains largely favorable looking into the long term, though its over-reliance on key customers remains far from ideal. Both companies have positives and negatives, but Skyworks seems like the better buy today.

10 stocks we like better than Skyworks Solutions When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Skyworks Solutions wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017.

Andrew Tonner owns shares of Apple. The Motley Fool owns shares of and recommends Apple, Nvidia, Qualcomm, and Skyworks Solutions. The Motley Fool has the following options: long January 2018 $90 calls on Apple, short January 2018 $95 calls on Apple, short August 2017 $87 calls on Skyworks Solutions, and short August 2017 $85 puts on Skyworks Solutions. The Motley Fool recommends NXP Semiconductors. The Motley Fool has a disclosure policy.