Better Buy: Philip Morris International, Inc. vs. PepsiCo

The global market for consumer goods is good, and Philip Morris International (NYSE: PM) and PepsiCo (NYSE: PEP) have done great jobs of capitalizing on demand for their products around the world. Because international markets have greater growth prospects for consumer stocks than the U.S. market, many investors gravitate toward companies that give them exposure to areas that have a rapidly growing middle class of potential new customers. Yet investors need to know which of these two consumer giants looks more favorable.

To help you decide which of these two stocks is the better buy, we'll take a look at Philip Morris and PepsiCo through a number of analytical lenses to see which one comes out ahead.

Pepsi products go well beyond its namesake cola. Image source: PepsiCo.

Valuation and stock performance

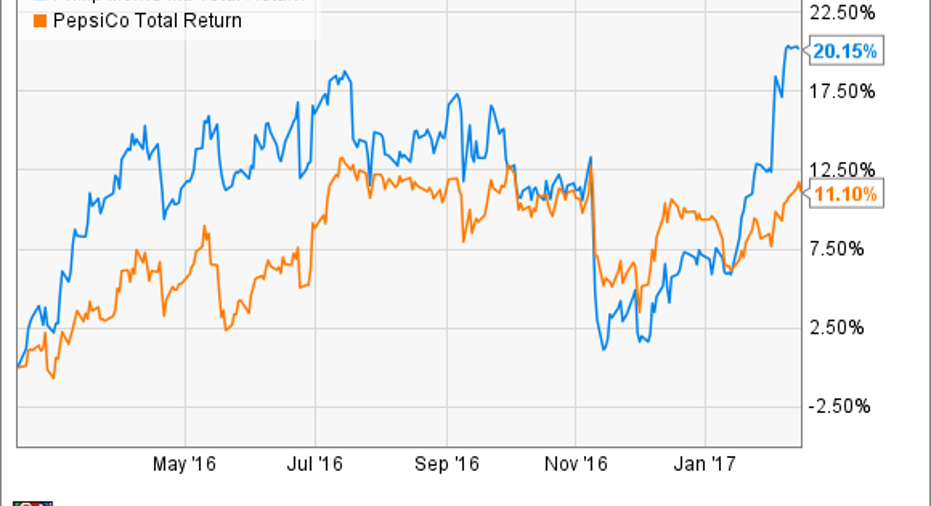

Both stocks have done well for investors lately, but when you look at the past 12 months, Philip Morris International has the edge over PepsiCo. The cigarette specialist has posted a total return of more than 20% since February 2016 compared to a respectable 11% gain for PepsiCo.

PM Total Return Price data by YCharts.

Often, a big rise in a stock brings heightened valuations, but Philip Morris and PepsiCo have relatively similar valuations. When you look at the income that they've brought in over the past 12 months, the two companies both have price-to-earnings ratios that are very close, at 23 times trailing earnings. Moreover, when you look at their respective opportunities for near-term profit growth, the gap opens up only minimally.

Philip Morris has a forward earnings multiple of roughly 20, while PepsiCo trades closer to 21 times forward earnings. Those differences are negligible, but Philip Morris has had more forward momentum recently in its stock price.

Dividends

For dividend investors seeking current income, Philip Morris has a clear edge over PepsiCo. The tobacco company boasts a 4% dividend yield compared to just 2.8% for the snack-food and soft-drink manufacturer. However, some investors prefer the fact that PepsiCo pays out only about two-thirds of its earnings in the form of dividends, which gives it more flexibility with respect to future increases. Philip Morris pays out nearly all of its current earnings in its dividends, and that has weighed on dividend growth lately.

PepsiCo has a much longer history of favorable dividend movement than Philip Morris. The drink maker just announced that it would boost its dividend by 7%, to $0.805 per share, on a quarterly basis. The move marks its 45th straight annual increase.

Philip Morris, on the other hand, was only able to make a 2% dividend boost last year, and some worry that future increases could also be small because of the company's challenges in growing its bottom line. PepsiCo's better growth prospects for its dividend largely offset the higher current yield that Philip Morris offers, making the comparison a wash.

Growth prospects and risks

The businesses that Philip Morris and PepsiCo operate in have both come under some pressure lately, both from fundamental aspects and from macroeconomic difficulties. Philip Morris has had to suffer the negative impacts of the strong dollar for a couple of years, and that's been a primary reason for its sluggish dividend growth. Yet in its most recent quarter, revenue and earnings both jumped considerably, and Philip Morris said that it expects to have a strong 2017.

The interesting long-term wildcard for Philip Morris is whether its corporate strategy to shift away from traditional cigarettes toward reduced-risk products will pan out. Early results from its iQOS heated tobacco system have been extraordinarily good in test markets in Japan, and Philip Morris is now looking to get approval from the U.S. Food and Drug Administration (FDA) for iQOS under the FDA's modified-risk product protocol. If that's successful, then the replacement cycle could bring huge growth opportunities for years to come.

PepsiCo has faced its own challenges, and it has worked hard to overcome them. In its most recent quarter, the drink and snack maker saw organic revenue rise 3.7%, lifting core earnings per share by 15% in constant-currency terms. Some of the health concerns about sugary soft drinks have affected PepsiCo's drink business, but the company was ahead of the curve in adapting to rising demand for healthier snack and beverage options, and it's reaping the rewards of those efforts in the current consumer environment.

PepsiCo said that it believes organic revenue will grow at least 3% in 2017, although a stronger U.S. dollar is likely to weigh on the top line again this year. Core earnings growth of 8% is also consistent with a mature company like PepsiCo.

At this point, Philip Morris International appears to be the better buy, with positive return momentum, a slight valuation advantage, a higher dividend yield, and a more exciting growth path ahead. That doesn't make PepsiCo a bad pick, though, and for conservative investors who aren't entirely comfortable with the transformative moves that Philip Morris is making, the soft-drink and snack giant could be the more comfortable choice going forward.

10 stocks we like better than PepsiCoWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and PepsiCo wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Dan Caplinger has no position in any stocks mentioned. The Motley Fool owns shares of and recommends PepsiCo. The Motley Fool has a disclosure policy.