Better Buy: Caterpillar Inc. vs. United Technologies

It's always interesting to compare stocks like Caterpillar Inc.(NYSE: CAT) and United Technologies Corporation(NYSE: UTX). They both have exposure to the global economic cycle, and in particular construction markets, but their other specific end markets differ so muchas to make them significantly different investment propositions. Moreover, Caterpillar's upside prospects come from cyclical strength in areas like mining, energy, and transportation, while United Technologies' largely come from management's successful execution of its plans to transition the company toward long-term growth.

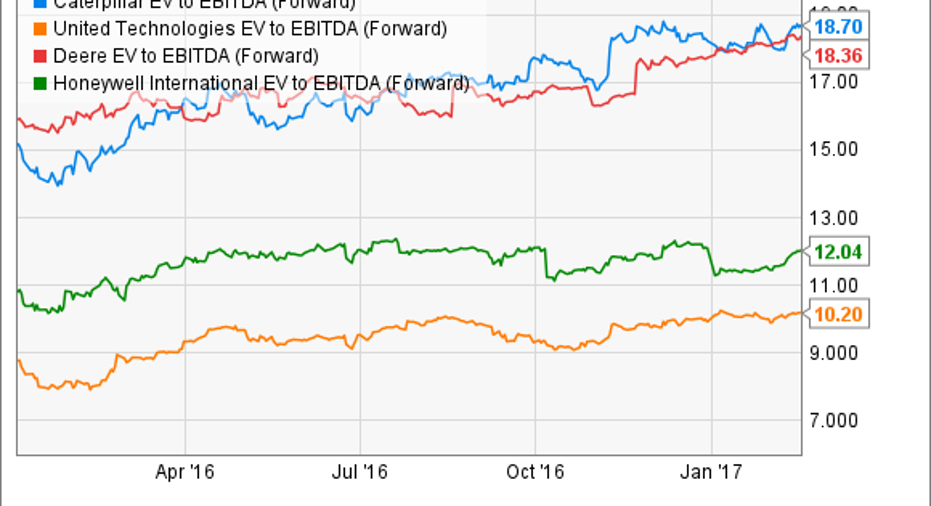

Valuation

It might seem unusual to start with valuation, but it helps to distinguish the investment case for each stock. The following chart shows analyst consensus for forward enterprise value (market cap plus net debt) divided by earnings before interest, tax, depreciation, and amortization (EBITDA). It's a useful valuation because it includes a debt consideration and an appreciation for future earnings -- an important point for a highly cyclical company like Caterpillar.

CAT EV to EBITDA (Forward) data by YCharts.

There are two points to note. First, Caterpillar is significantly more expensive than United Technologies -- but don't jump to any conclusions just yet. Caterpillar's valuation reflects its greater growth prospects in the next few years. For example, going by current analyst estimates -- see table below -- Caterpillar is set to grow strongly in 2018 as end markets, hopefully, turn more positive in 2017 and customers buy up existing machineinventory.

On the other hand, United Technologies' low valuation reflects its weak earnings prospects in the next few years, largely due to actions taken to ensure long-term profitability -- more on that later.

| Metric | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|

|

Caterpillar EPS (estimate) |

$3.42 | $3.06 | $4.21 | $5.38 |

| Caterpillar growth(estimate) | -- | (10.5%) | 37.6% | 27.8% |

| United Technologies EPS(estimate) | $6.61 | $6.55 | $7.02 | $7.68 |

| United Technologies growth(estimate) | -- | (0.9%) | 7.2% | 9.4% |

Data source: Nasdaq.com. Author's analysis.

Second, Caterpillar's valuation is slightly more expensive than that of its peer Deere, while United Technologies' is cheaper than that of its peers Honeywell International and Eaton Corp. On balance, and based on near-term earnings, United Technologies is a cheaper stock on an absolute and relative basis.

Earnings trends

Which stock has better earnings momentum in 2017? The answer is unfortunatelyfar from clear.

At the Credit Suisse conference in December, Caterpillar's management described analyst consensus for $3.25 in EPS in 2017 to be "too optimistic."The commentary helped walk down analyst consensus toward the $3.06 mark, and in the fourth-quarter earnings presentation in late January, management guided toward $2.90 for 2017. But here's the thing: A broad spectrum of companies made positive remarks on Caterpillar's main end markets (construction, energy, resources, transportation) in the last few months, including General Electricon energy and United Technologies itself on construction.

Image source: Caterpillar Inc.

United Technologies' key focus in 2017 is successfully executing on its plans to transform three of its four segments. Otis elevators needs to regain market share with equipment sales so it can generate long-term service revenue, and Pratt & Whitney needs to ramp up production of its new geared turbofan engine.Meanwhile,aerospace systems needs to go through a period of margin compression while it replaces sales of higher-margin legacy products with newer, initially lower-margin products on new aircraft programs. For these reasons, United Technologies' profit growth will be limited in 2017 and in the next few years.

Image source: Getty Images.

Which stock to buy?

In short, United Technologies. While it's true that Caterpillar has more near-term earnings potential from a cyclical pickup in growth, it looks like the market has baked much of this in already, and there's always the risk that oil and resources markets could turn down again.

United Technologies also carries economic risk, and there is no guarantee that Pratt & Whitney will fully resolve issues with geared turbofan engine production, or that it will not have more problems. That said, I believe that when companies are in transition, and suffering near-term earnings headwinds, they should actually trade at a premium to the market. This is because the market should be pricing in an assumption of stronger earnings in a few years' time.

However, as you can see above, United Technologiestrades at a discount. Markets aren't always right, and the current valuation discount should be enough to attract investors with a long-term perspectivewho believe its stock ison theright track.

10 stocks we like better than CaterpillarWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Caterpillar wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Lee Samaha owns shares of United Technologies. The Motley Fool owns shares of General Electric. The Motley Fool has a disclosure policy.