Average Americans Aren't Doing Enough to Save for Retirement, Says Survey

IMAGE SOURCE: FLICKR USER SENIORLIVING.ORG.

A new survey byBlackrock finds that even among Americans who are saving for retirement, a frustratingly low 28% of people are confident that they're putting enough money away for their golden years. Are you doing more than the average American to prepare for retirement? Read on to learn what Blackrock's survey discovered and what you can do to give your retirement savings a boost.

Too little being doneThe Blackrock survey included over 1,000 people who participate in defined contribution plans, such as 401k plans, and who have saved at least $5,000 for retirement. These respondents included millennials, Gen Xers, and baby boomers and responses regarding retirement preparedness varied widely by age.

Millennials, for example, were the most confident that their retirement savings are on the right track. While only 43% of Gen Xers and 54% of baby boomers think that their retirement savings are on the right path, 59% of millennials reportthat their plans have them pointed in the right direction.

However, millennials are the least likely to be taking action to make the most of their retirement savings. Only 36% of millennials report increasing the amount they contribute to a retirement savings account when possible and only 38% pay attention to the performance of their holdings in their retirement plan.

Alternatively, 48% of Gen Xers and 53% of baby boomers are boosting their annual contribution rate when possible and 51% of Gen Xers and 56% of baby boomers are tracking their investment returns.

Given younger workers tend to be more optimistic about their future earnings potential and older workers tend to be more realistic about the potential shortfall of money in retirement, the findings related to being on the right track aren't totally surprising.

What is surprising, however, is how few millennials, Gen Xers and baby boomers are taking action to increase their retirement contributions and evaluate their investment choices.

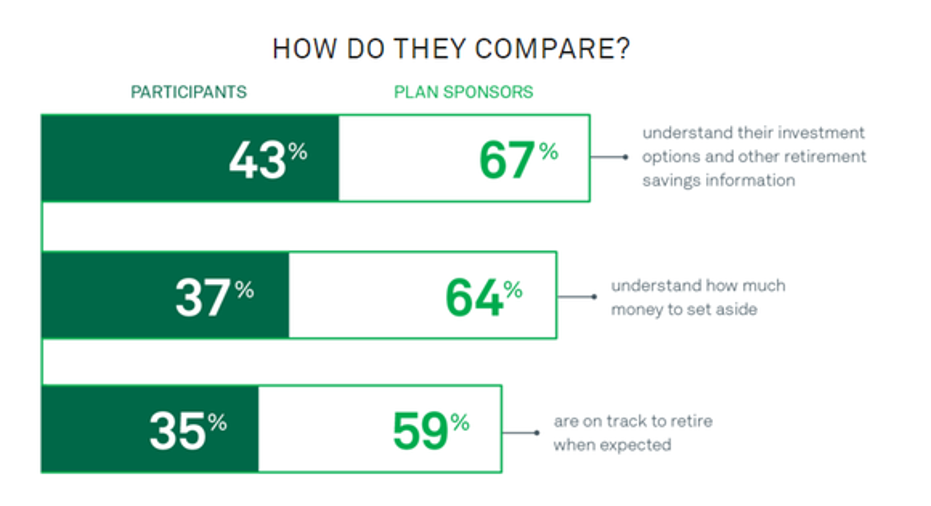

A knowledge gapA lack of investment knowledge could be to blame. The survey discovered that while 67% retirement plan sponsors think employees understand their investment options and retirement savings plans, only 43% of employees actually do understand them.

Additionally, 64% of plan sponsors think employees have a good understanding of how much they'll need to save for retirement, but only 37% of employees report understanding their retirement income needs.

DATA SOURCE: BLACKROCK.

Many Americans believe that Social Security income will provide a significant level of retirement income, when in reality Social Security is likely to replace only about 40% of preretirement wages. Workers may also have unrealistic expectations for how long retirement savings will last. Typically, its recommended that retirees only withdraw 4% of their savings annually in retirement, a small percentage that could result in savings proving to be a smaller-than-expected source of income.

Closing knowledge gaps like these could be the key to encouraging workers of all ages to more actively embrace portfolio-boosting behaviors.

Making changes nowAutomatically investing in IRAs and workplace retirement plans is great, but Americans can build even bigger nest eggs by enrolling in programs that automatically increase the percentage of their contribution every year.

An auto-escalating program increases the percentage rate of contribution by a specific percentage every year, such as 1%, until a set benchmark is reached, for example 10%. This feature is increasingly common and people participating in plans with auto-escalation tend to save far more for retirement than people in plans without them. Roughly one-third of plan participants save 10% or more per year in plans with auto-escalation, while only one-fifth of plan participants save a similar amount in plans without the feature.

Compounding interest means that the benefit of auto-escalating is biggest for young workers, but older workers can take advantage of catch-up contributions too. Usually, contributions to workplace retirement plans are capped at $18,000, but people over 50 years old can contribute an additional $6,000 in catch-up contributions. Although taking advantage of auto-escalation features and using catch-up contributions may not guarantee a lifestyle of the rich and famous, embracing these two strategies could help you achieve financial security in retirement.

The article Average Americans Aren't Doing Enough to Save for Retirement, Says Survey originally appeared on Fool.com.

Todd Campbell has no position in any stocks mentioned. Todd owns E.B. Capital Markets, LLC. E.B. Capital's clients may have positions in the companies mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.