Are You Still Investing Without a Margin of Safety?

In retrospect, Brexit turned out to be more meaningful than Grexit. And while the immediate reaction of global financial markets (NYSEARCA:VT) to the England’s decisive vote to leave the European Union (EU) was negative, it’s a stark reminder of why investing without a margin of safety is negligent.

With the exception of precious metals (NYSEARCA:GLTR), mining stocks (NYSEARCA:GDXJ), U.S. Treasuries (NYSEARCA:TLT), and a few defensive sectors like utilities (NYSEARCA:XLU) there were few places to hide.

(Audio) How Your Non-Core Portfolio Should Work

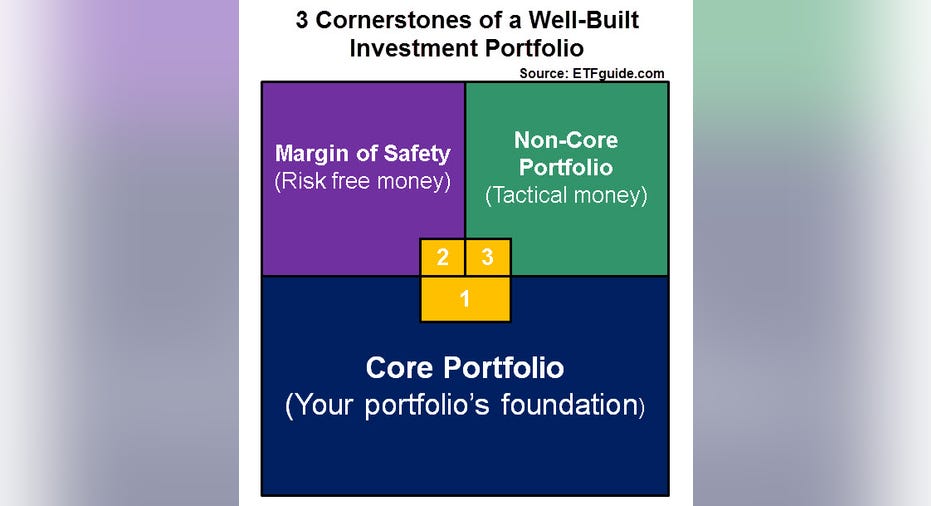

As I’ve relentlessly advocated on my weekly podcast and at ETFguide.com, the three cornerstones of an architecturally sound investment portfolio are 1) a core, 2) non-core, and 3) a margin of safety. Each of these three components plays a deliberately different role than the other part inside your investment portfolio. While the core and non-core part of your total investment portfolio will generally be oriented toward growth and income, your portfolio’s margin of safety is strictly reserved for capital preservation. And it serves no other role but to give you a cushion and permanent form of insurance.

The concept margin of safety is not new. It was originally introduced by investing legend Benjamin Graham. He applied margin of safety in the context of selecting individual stocks at prices below intrinsic value that would give the investor an adequate cushion or margin of safety.

For all investors, Graham’s groundbreaking idea about how to properly manage risk has broader applications beyond selecting individual stocks. In the spirit of Graham’s prudent advice, the concept margin of safety can be extended to how a portfolio of investments is assembled and managed. I also teach this in my online course “Build, Grow, and Protect Your Money: A Step-by-Step Guide.”

What type of assets should you use for your portfolio’s margin of safety?

The key characteristics for assets inside your portfolio’s margin are 1) they should not lose market value, 2) they should not have market volatility, and 3) principal and income should be guaranteed. These prerequisites automatically rule out assets like gold (NYSEARCA:GLD) and bonds (NYSEARCA:BND), which are often improperly used as margin of safety assets. Because bonds and gold are both susceptible to market losses, they are unsatisfactory components for a person’s margin of safety.

Installing an adequate margin of safety within your portfolio right now vs. later prevents you from doing it at a future time when market conditions may not necessarily be favorable. Put another way, acquiring insurance should always occur before the house burns down, not when it’s burning and most certainly not after it’s burned down.

To help you, I’ve created a margin of safety worksheet that will help you to accurately calculate how much of your portfolio should be dedicated to margin of safety. This worksheet is also available to premium members at ETFguide for no additional charge.

Here’s a few more things you should know about your portfolio’s margin of safety:

1) Your margin of safety is a permanent form of insurance within your total investment portfolio and is always on 2) The exact percentage of your portfolio earmarked for margin of safety is not guided or decided by present or future market conditions 3) Your age and investment time horizon along with your risk tolerance level are among the key factors that will determine how much of your portfolio is earmarked for margin of safety 4) Asset allocation and diversification are not satisfactory substitutions for investing without a margin of safety 5) Being a long-term investor does not make you prudent if you’re investing without an adequate margin of safety

Those who complain that margin of safety undermines long-term investment results are dead wrong.

As noted by my colleague Ron Surz in a recent post, William F. Sharpe won a Nobel in 1990 for his Capital Asset Pricing Model, which, among other things, proved that risk control is best achieved with a margin of safety or cash. And a portfolio that blends the “market” with cash, dominates the Efficient Frontier at low levels of risk thereby providing higher returns for the same level of risk.

It’s no coincidence legendary investors like Warren Buffett always have a margin of safety within their portfolio like cash equivalents and other assets with principal protection. This layer of portfolio protection takes Ben Graham’s margin of safety concept one-step further by applying it to how an entire portfolio of investments should be managed.

Does your investment portfolio have an adequate margin of safety? If not, then now is the time to do it.