Are Higher Interest Rates Good for Bank Stocks? Its Complicated, Says Analyst Dick Bove

Whether higher rates are good or bad for a particular bank depends on a balancing act. Image source: iStock/Thinkstock.

Much of the current excitement surrounding bank stocks stems from investors' belief that interest rates will continue to rise, sending bank profits higher as well. There's truth to this, writes longtime bank analyst Dick Bove in a recent research note, but there's more to the story than just this.

Looking back to the 1970s

In a report published Monday, Bove looked to the 1970s to get a sense for what's going on in the bank industry today. He did so because the 1970s were known for rapidly rising interest rates. By looking at what happened to bank stocks then, in turn, we can get a sense for what to expect now.

Bank profits did in fact go up during that decade. Earnings per share among money center banks -- those like JPMorgan Chase (NYSE: JPM), Bank of America (NYSE: BAC), and Citigroup (NYSE: C) -- nearly tripled from 1971 to 1981, Bove notes.

This makes sense when you consider that banks sell loans, the prices of which are dictated by interest rates. Higher rates mean higher loan prices. And higher loan prices mean higher interest income for banks.

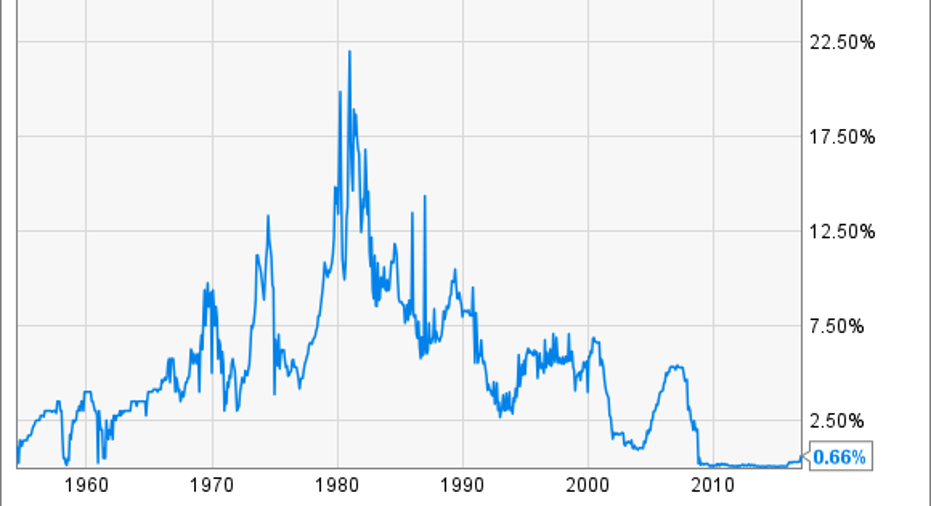

The 1970s paradox

Given that interest rates soared throughout the 1970s -- short-term rates got as a high as 18% -- you'd think that the 1970s must have been a great decade for bank stocks. After all, higher profits should translate into higher valuation multiples for bank stocks.

Effective Federal Funds Rate data by YCharts.

But this isn't what happened. In fact, the multiples on bank stocks went in the other direction. The average price to earnings multiple for banks like JPMorgan Chase, Bank of America, and Citigroup went from more than 13.0 in 1972 down to less than 5.0 eight years later.

What caused this paradoxical result? In short, because higher interest rates weigh on the price of fixed-income securities (which are a main component of any bank's asset portfolio). Bove says that higher interest rates are only good for banks so long as the benefit to profits outweighs the detriment to book value.

According to Bove,

Today vs. the 1970s

Bove is absolutely right to point out that "interest rate changes are often not what is thought in valuing bank stocks." However, there are a couple of things that are worth pointing out.

The first is that the 1970s and today, while similar because they were both periods of rising interest rates, are also very different. The 1970s was a particularly tumultuous decade for banks, and things got worse in the 1980s, as the savings and loan crisis gained momentum.

The problem at the time wasn't just that interest rates were volatile. The more important issue was that they rose incredibly rapidly, as the Federal Reserve sought to combat a wave of double-digit inflation ignited by soaring energy prices thanks to two OPEC-led oil embargos that decade. This isn't as big of a problem today as there's little reason right now to be worried about a rapid rise in rates since we're still in the shadow of the financial crisis.

Moreover, banks in the 1970s managed interest rate risk differently than they do today. After predecessor banks to JPMorgan Chase, Bank of America, and Citigroup nearly failed because their cost of money (short-term rates) rose beyond what they earned on their fixed-rate loan portfolios (long-term rates), they began underwriting variable-rate loans.

This is the model today -- indeed, one could go so far as to say that modern interest rate risk management was invented in the 1970s. The net result is that higher rates should translate into higher profits at a quicker rate today than they did four decades ago, and the downside shouldn't be as bad either.

This is why Bank of America is so asset sensitive and will earn $5.3 billion more in additional net interest income once rates reach merely a percent higher than they were at the end of September. JPMorgan Chase isn't far behind at just under $3 billion, while Citigroup is closer to $2 billion.

In sum, while Bove is right that higher rates will yield more income for banks, he's also right that they will weigh on book value. This is why the pace of rate hikes is so important. "Multiple increases in short periods are not positive for these stocks," says Bove. "Moderate increases over long periods are positive."

10 stocks we like better than Bank of America When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Bank of America wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

John Maxfield owns shares of Bank of America. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.