Alliance Resource Partners: Has This High-Yielder Finally Hit the Wall?

For a long time high yielding Alliance Resource Partners had been the standout performer in the hard-hit coal industry. The business environment is only getting worse, though, and despite this limited partnership's ability to buck the industry-wide downtrend for so long, things have started to change. The third quarter may have been a key turning point.

Up up and awayAlliance Resource Partners' top line has headed higher in each of the past 10 years. Dividends have been on the rise as well, advancing annually over the span. Dividend growth was a compelling 15% or so on an annualized basis. Compare that to a company like Peabody Energy , one of the world's largest independent coal miners.

Peabody's top line peaked in 2012 and has fallen each year since. The dividend was stuck at $0.085 a quarter between late 2010 and year-end 2014. It's now a meager $0.01 a year. And Peabody is one of the luckier industry players; once-giant Alpha Natural Resources is in bankruptcy. To be fair, there are other coal companies that have fared better than Peabody and Alpha, but Alliance was the clear stand-out performer in the industry.

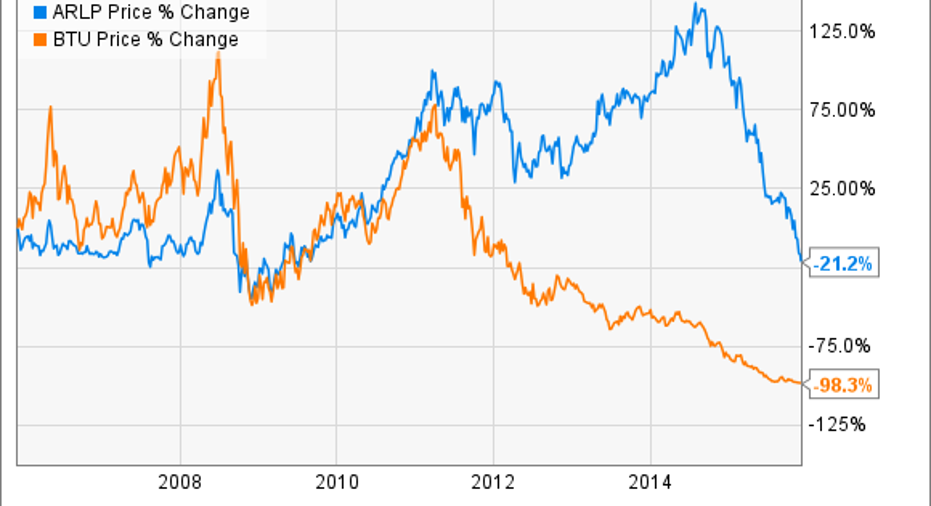

No wonder the partnership's units advanced over 300% in the decade leading up to March 2014 (during which Peabody only rose 40% or so). The big change, however, took place in early 2011 when Alliance's units continued to head higher and competitors started to feel the heat of falling coal demand and prices.

The big difference? Alliance managed to remain profitable while competitors like Peabody Energy and Arch Coal started to hemorrhage red ink. And, perhaps even more important, Alliance kept hiking its dividend. Not surprisingly competitors shares turned lower, but Alliance kept moving higher... until March of last year, that is. That's when Alliance's units started to crumble, too.

What's changed?The big change at that point was the realization that even Alliance, which had been able to use increasing production to make up for low coal prices, couldn't outrun falling coal prices forever. Alliance is down over 60% since March of last year (Peabody, for reference, is down 95%). But for investors watching company fundamentals, the drop may not have made sense.

That's why the third quarter was such a rough one; the company's sales fell year over year. You could forgive one quarter of weakness at a partnership that's done so well for so long, except for the comments by management. In the third-quarter earnings release, CEO Joseph Craft noted that, "Overall for the U.S. domestic thermal coal outlook, we expect future demand to be stable; however, the market continues to be oversupplied causing weak commodity prices. We see no near-term catalyst to improve pricing except a supply response by the industry."

Looking at the numbers, the company's coal sales increased nearly 5% year over year in the quarter but that wasn't enough to make up for still-falling coal prices. And Case went on to say, "As we evaluate our own supply response to an uncertain coal market, ARLP is electing to maintain quarterly cash distributions per unit at current levels." In other words, Alliance is thinking about reducing its coal production, which will, without a rise in coal prices, lead the top line even lower. And since Case doesn't seem to think coal prices are heading higher in the near term, Alliance's results could start to look more like its competitors' results. This is a problem.

Alliance is conservative, compared to peers. Image source: Alliance Resource Partners.

Wiggle roomThat said, Alliance's covered its distribution by 1.66 times in the third quarter. While falling production and weak coal markets will likely shrink that number, the miner has plenty of wiggle room to maintain its distribution for now. And if the industry standout is starting to cut back, it might be the sign that the industry is about to turn the corner.

The changed outlook suggests that Alliance isn't appropriate for conservative investors. At this point, no coal company is. However, more aggressive types, and particularly contrarians, might want to take a deep dive. Alliance is still the cleanest shirt in a dirty laundry pile. With a conservative management team, room to support the distribution, and a more than 20% yield, it may be worth the risk. However, you'll want to keep a close eye on production, sales, and distribution coverage.

The article Alliance Resource Partners: Has This High-Yielder Finally Hit the Wall? originally appeared on Fool.com.

Reuben Brewer has no position in any stocks mentioned. The Motley Fool recommends Alliance Resource Partners. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.