7 Top Stocks to Buy in October

Image source: Getty Images.

Great stocks come in many shapes and sizes, and finding the best ones to buy now can be tricky. To help investors home in on the top stocks on the market today, we asked some of our top contributors for their best ideas. Their picks span healthcare, consumer goods, basic materials, services, and technology, but all of their ideas have one thing in common: upcoming catalysts that could send their shares higher.

A growing healthcare powerhouse

Todd Campbell: Pfizer, Inc.'s(NYSE: PFE) recent decision to remain a single company, rather than split in two, has caused its share price to drop, but I think selling Pfizer on this news is shortsighted -- and creating a bargain-bin buy opportunity.

Pfizer isn't the struggling company it was a few years ago, when it was reeling from lost sales tied to the expiration of patents protecting its mega-blockbuster cholesterol drug Lipitor.

A restructuring has made Pfizer leaner, new drug launches are reinvigorating growth, and a best-in-class balance sheet is allowing management to go on a spending spree that's positioning the company as a leader in cancer treatment andthe emerging market for biosimilars.

The company has jettisoned non-core businesses, including its pet business, and its R&D team has delivered big wins with multibillion-dollar anticoagulant Eliquis and fast-growing breast cancer drug Ibrance. A $17 billion acquisition of Hospira has given it an enviable stable of biosimilars, including Inflectra, which is expected to launch soon in the U.S. as an alternative to multibillion-dollar autoimmune disease drug Remicade. Meanwhile, a $14 billion acquisition of Medivation has given Pfizer the $2 billion-and-growing prostate cancer drug Xtandi, as well as two cancer drugs in late-stage trials.

Pfizer's change in fortune has already allowed it to deliver six consecutive quarters of operational growth, and management is guiding for $51 billion in sales this year, up from $49 billion last year. If Pfizer hits that target, it will represent the company's first year-over-year top-line growth in years. Management also targets EPS of $2.38, which is a nice jump from the $2.20 reported in 2015. Industry watchers think EPS will climb to $2.64 next year, which gives Pfizer an attractive forward P/E ratio of roughly 13.

Overall, Pfizer is returning to growth, and its decision to remain a single company doesn't change that. Because of that, buying shares on sale and pocketing a healthy 3.5% dividend yield in the process could be very profit-friendly.

Image source: PepsiCo.

Dinged by a strong dollar

Jamal Carnette:If you're in the market for a high-yielding large-cap stock with growth potential, thenPepsiCo(NYSE: PEP) is an appealing choice. In recent years, the company has been dogged by the perception that its sugary drinks and salty snack foods are contributing to a global obesity epidemic. PepsiCo's recently announced third-quarter results show that it's serious about addressing these concerns while still growing its business.

PepsiCo noted that nearly half of the company's revenue came from what it refers to as "guilt-free" products -- i.e., drinks with fewer than 70 calories per 12 ounces and lower-fat, lower-sodium snacks. Financially, PepsiCo reported that core earnings per share grew 3.7% to $1.40 in the third quarter versus $1.35 in Q3 of last year. It also raised its forecast for full-year core earnings to $4.78 per share, ahead of Wall Street analysts' predictions. When it comes to top-line results, PepsiCo reported a year-over-year net revenue decrease of 1.9%.

However, PepsiCo's quarter was even better than it appears on first sight. The strengthening U.S. dollar hurts U.S.-based exporters like PepsiCo. On a constant-currency basis, which excludes the effects of currency fluctuations, the company grew core earnings per share 7% and increased organic revenue by 4.2%.

In the end, PepsiCo appears to growing revenue and earnings per share at a healthy clip once currency effects are stripped out. Eventually, those currency effects will ameliorate, but the company's strategy of improving execution and selling healthier snacks should continue to drive the stock higher.

Merger, margins, or dividends: This stock offers all

Neha Chamaria: Down about 5% this month, Dow Chemical (NYSE: DOW) is the kind of stock you could consider buying on a dip, given the chemical giant's strong growth prospects and low valuation.

At 8 times trailing earnings, Dow is trading at less than half its five-year average and industry P/E. To top that, the stock is offering a dividend yield of 3.5% -- much higher than the 2.2% offered byDuPont (NYSE: DD), a close competitor that Dow is preparing to merge with. While the proposed merger hasn't cleared regulatory hurdles yet, the combined entity would be the world's largest agricultural chemicals company and the second-largest materials company. Those prospects demand a much higher premium.

Of course, I'm not asking you to bet on a merger that hasn't been finalized. Regardless, Dow has an enviable track record of high margins and shareholder returns. Its current operating margin of about 12% is up sharply from its sub-5% margins in 2013, and Dow's EPS more than doubled year over year to $2.61 during the last quarter.

Dow's two-pronged strategy of pursuing aggressive growth opportunities while restructuring existing businesses should push its earnings and cash flows even higher in coming years. Its growth catalysts include huge ongoing projects like Sadara, the world's largest petrochemicalfacility, which Dow is setting up in alliance with Saudi Aramco. That's just one of the many growth avenues Dow is pursuing right now.

In short, Dow looks compelling at today's price, merger or not.

A "must-own" stock

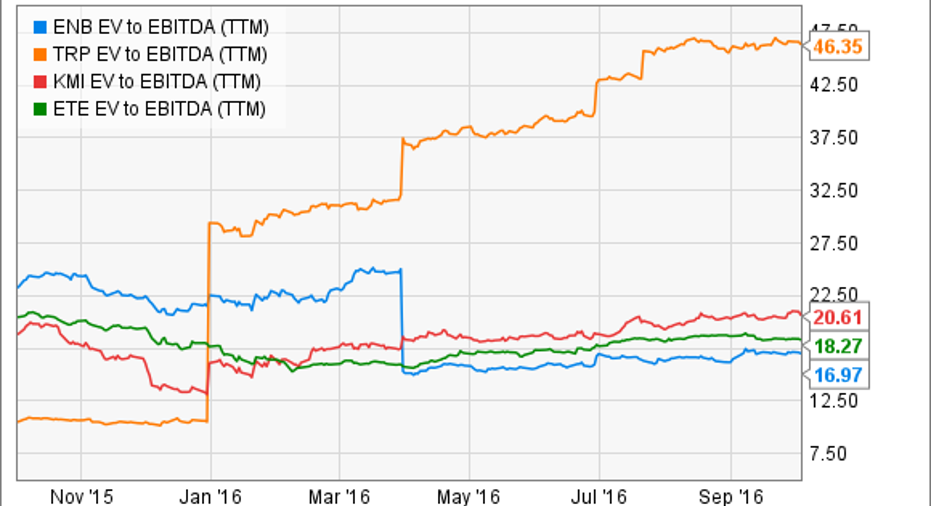

Matt DiLallo: Canadian energy infrastructure giant Enbridge (NYSE: ENB) has everything an investor could want in an investment. With a current yield of 3.75%, it provides plenty of income for dividend seekers. Meanwhile, growth investors will like the company's enormous project backlog, which should drive 12% to 14% annual growth in available cash flow from operations through 2019. Finally, value investors will love the fact that despite the lucrative income stream and visible growth, Enbridge's stock trades at a discount to its peers:

ENB EV to EBITDA (TTM) data by YCharts.

Not only does Enbridge offer ample growth and income at a reasonable value, but the company's financials are rock solid. Fee-based assets such as pipelines, renewable power plants, and utilities underpin 96% of the company's cash flow, providing stability. Further, the company only pays out about half of its cash flow via dividends, leaving plenty of excess to fund a significant portion of its growth projects, reducing its reliance on the fickle capital markets. Combine these factors with the company's investment-grade credit rating, and Enbridge should prove resilient in all market conditions.

This combination of stability and growth is why the company's management team believes Enbridge has become a "must-own" investment for long-term-minded investors.

Image source: IMAX Corporation.

Focus on the big picture

Brian Feroldi: Wall Street hasn't been showing shares of IMAX (NYSE: IMAX) any love recently, and it's not hard to understand why. Last quarter, the company's revenue declined by 14%, and EPS plunged by 68%. Those are hardly the kind of numbers that might cause a stock to rally.

However, the reason IMAX's quarterly numbers don't look so hot is that in the same quarter last year, the company recorded its highest-grossing box office ever. At the time, IMAX was showing a handful of mega-blockbuster hits like Jurassic World, Avengers: Age of Ultron, and Furious 7, so topping those results was going to be tough.

The hit-or-miss nature of the movie business means that IMAX's quarterly results will always be lumpy. That's why I prefer to keep my eyes trained on new theater installations and the company's backlog as a way to measure quarterly progress. Thankfully, IMAX is crushing it on both of those metrics.

Last quarter, the company installed 40 theaters, bringing its total network up to 1,102 systems. For the full year, management is calling for total new installations to reach 155, which is far higher than its original guidance of 115 to 120 theaters. What's more, the company has added 95 systems to its backlog, bringing the new total up to 442 total installs. That should ensure that new installations remain high for years to come.

The lineup of movies that will soon hit IMAX's theaters also looks strong. On that list are a handful of guaranteed hits likeGuardians of the Galaxy Vol.2,Rogue One: A Star Wars Story, Transformers: The Last Knight,andStar Wars: Episode VIII.

All told, IMAX's long-term growth story looks fully intact. With shares now trading for less than 23 times next year's earnings estimates, I think this is a great time to buy into this high-quality growth stock.

Ride on Wall Street's coattails

Dan Caplinger: The bull market in stocks has lasted for more than seven years now, and Wall Street's finest need the best research available in order to take maximum advantage of favorable industry conditions. FactSet Research Systems (NYSE: FDS) aims to provide just that to financial companies, and its success in that industry has led to a growing client base and increased adoption among its customers.

Investors now have a rare opportunity to buy into FactSet at a slightly reduced price, because the company recently announced quarterly results that led some investors to fear slowing growth. But solid gains in revenue, annual subscription value, and profits are still driving FactSet higher, and in particular, impressive results from its overseas highlight the diversification FactSet enjoys beyond the U.S. market.

It's true that if the financial industry suffers an ordinary cyclical downturn, then FactSet could see near-term pressure. Yet with one of the premier suites of information offerings available, FactSet should thrive in the long run. So long as financial companies seek to gain an investing advantage over their competitors, then FactSet should continue to grow its client base over time.

Image source: Whole Foods Market.

Earning a "healthy" profit

Steve Symington: Shares of Whole Foods Market(NASDAQ: WFM) trade near 52-week lows, and I'll admit the organic grocer has left a bad taste in many investors' mouths. But I think now is the perfect opportunity for long-term-oriented shareholders to open or add to a position in Whole Foods.

First, we're still in the early stages of Whole Foods' long-term growth story. Whole Foods ended last quarter with "just" 455 locations in the United States, Canada, and the United Kingdom. But management sees potential for operating 1,200 Whole Foods stores in the U.S. alone -- and thatdoesn'tinclude its new smaller-format, value-oriented 365 stores, the first of which opened last quarter and has enjoyed a largely positive reception so far.

What's more, last quarter Whole Foods demonstrated an encouraging sequential improvement in comparable-store sales trends, while co-CEO Walter Robb insisted the company has made "measurable progress on fundamentally evolving our business" under the nine-point turnaround plan it unveiled last November. That plan notably includes goals to improve Whole Foods' cost structure, increase technology and marketing investments, and help consumers better understand the company's value proposition the face of intensifying competition.

Finally, Whole Foods is a pioneer for the concept of "conscious capitalism,"recognizing that it shouldn't pursue profits above all else, but rather strive to "delight" its customers, employees, and suppliers, contribute to local communities, advocate for environmental sustainability, and sell only the highest-quality natural and organic products available.In short, you can feel good about owning shares of Whole Foods. And in my opinion, those shares just so happen to be trading at a particularly attractive price right now.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

John Mackey, co-CEO of Whole Foods Market, is a member of The Motley Fool's board of directors. Dan Caplinger owns shares of Whole Foods Market. Jamal Carnette has no position in any stocks mentioned. Matt DiLallo owns shares of FactSet Research Systems, IMAX, and Whole Foods Market. Matt DiLallo has the following options: short November 2016 $33 calls on Whole Foods Market. Neha Chamaria has no position in any stocks mentioned. Steve Symington owns shares of Whole Foods Market. Todd Campbell has no position in any stocks mentioned. The Motley Fool owns shares of and recommends FactSet Research Systems, IMAX, PepsiCo, and Whole Foods Market. Try any of our Foolish newsletter services free for 30 days.

We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.