7 Key Takeaways From Bank of America's Earnings Report

Bank of America (NYSE: BAC) reported first-quarter earnings that beat analyst estimates on the top and bottom lines, but that only tells part of the story. A deeper look at the bank's latest earnings report shows that the bank continues to improve in terms of efficiency and profitability, so here are seven key items that are important for investors to know.

1. The numbers beat expectations

First, the headline numbers. The bank's revenue of $22.2 billion handily beat estimates of $21.6 billion, and was up 7% from a year ago. Plus, the bank earned $0.41 per share, beating estimates by $0.06. This is certainly good news, as Bank of America's business continues to improve at a faster-than-expected pace. However, the headline numbers only tell a small part of the story, so let's take a closer look.

Bank of America's stock has performed well over the past year -- will it continue? Image source: Getty Images (Note: This is not a chart of BofA's performance.)

2. Profitability is steadily improving

Bank of America's stock has traded for one of the lowest price-to-book multiples in the banking sector for several years. One major reason for this is the bank's lack of profitability -- specifically, the failure to meet the industry benchmarks of a 10% return on equity and a 1% return on assets. And while the bank isn't quite there yet, it's getting much closer.

|

Quarter |

Return on Assets (ROA) |

Return on Equity (ROE) |

|---|---|---|

|

1Q 2016 |

0.64% |

5.1% |

|

4Q 2016 |

0.85% |

7% |

|

1Q 2017 |

0.88% |

7.3% |

Data source: Bank of America earnings report.

3. Revenue grew, but expenses did not

I mentioned earlier that Bank of America earned $0.41 per share for the first quarter. This was a 40% profit improvement over the first quarter of last year, much more of a jump than the bank's 7% revenue growth.

The main reason for this is that while the bank's revenue grew, its expenses did not. Overall, Bank of America's expenses were completely flat year over year. Particularly impressive was the consumer banking unit, which managed to reduce expenses by 3%, despite a 5% growth in revenue. In a nutshell, increased revenue without higher expenses translates to strong profit growth.

4. Buybacks are still the priority -- for now

I've written before about how Bank of America's capital priority over the past few years has been buying back its own shares, as opposed to aggressively increasing its dividend. And despite the much higher share price, that is still the case, as the bank returned $3.1 billion to shareholders during the quarter, and $2.3 billion of this was in the form of buybacks.

Bank of America shares have risen considerably in price over the past year or so, and now trade for just under their book value, and therefore are not as compelling of a bargain as they used to be. Buybacks may be the priority for the time being, but I wouldn't be surprised to see the emphasis shift slightly, in favor of a higher dividend, once the bank submits its capital plan to the Federal Reserve.

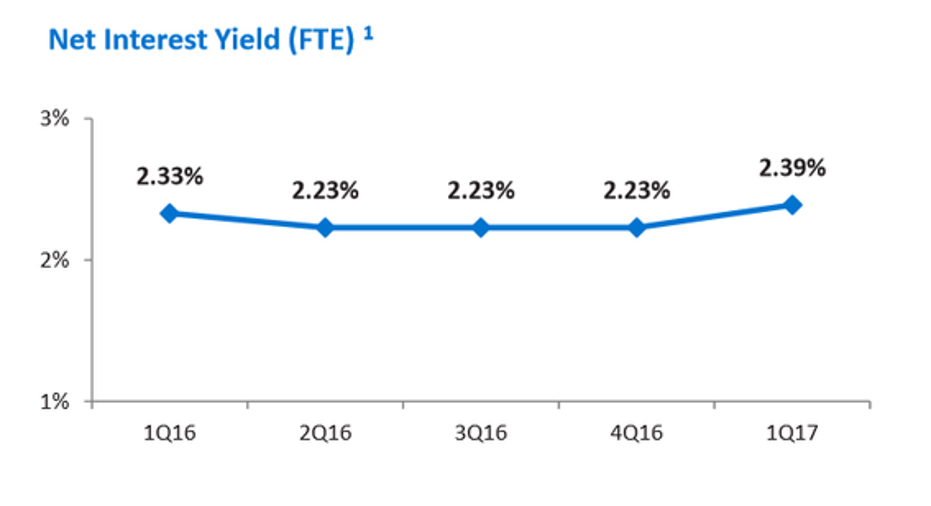

5. Interest ratespreads have gotten better

One factor that has kept Bank of America's profitability low over the past few years, as well as the rest of the banking industry, has been record low interest spreads. Banks earn a profit from borrowing money at a low rate, and lending it to customers at a higher rate -- known as the "spread," or the net interest yield.

During the first quarter, Bank of America's net interest yield finally started to improve after three straight quarters stuck at the lows. In the earnings report, Bank of America says it expects this to increase further in the second quarter, even without any additional interest rate hikes. Furthermore, the bank says that a 100 basis point (1%) improvement in the yield curve would translate to an additional $3.3 billion in net interest income over the next 12 months.

Image source: Getty Images.

6. The efficiency ratio is better than it appears

A bank's efficiency ratio is a measurement of how much the bank spends to generate its earnings, so lower is better. Bank of America's efficiency ratio has improved by 450 basis points over the past year, but 67% is still on the high end.

However, Bank of America pointed out in its earnings presentation that this looks artificially high due to seasonality. Specifically, if certain expenses, such as seasonally elevated payroll tax costs, had been spread evenly throughout the year, the efficiency ratio would have been a much more attractive 62%.

7. Bank of America is a mobile banking leader

Part of the reason for Bank of America's increasing efficiency is its strong growth in mobile and online banking. The more people who use these platforms, the greater the cost savings. For example, it costs the bank far less to process a paper check that's deposited than it costs to process a mobile check deposit.

During the first quarter, Bank of America reported 22.2 million active mobile banking users, a 13% year-over-year improvement. One-fifth of all deposit transactions are now completed through its mobile platform. Bank of America has received top rankings in mobile and online banking functionality, and also has improved its digital sales capability in recent quarters.

10 stocks we like better than Bank of AmericaWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Bank of America wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017

Matthew Frankel owns shares of Bank of America. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.