5 Top Stock Picks You Can Buy Now

Hunting for new stocks to tuck into your portfolio? Then it might be worth your time to consider these five stocks.

Domino's Pizza Inc. (NYSE: DPZ), the iShares Silver Trust (NYSEMKT: SLV), Pioneer Natural Resources (NYSE: PXD), The Priceline Group, Inc. (NASDAQ: PCLN), and Big Lots, Inc. (NYSE: BIG) all offer intriguing reasons why they could be top performers. Read on to learn if they're right for you.

IMAGE SOURCE: GETTY IMAGES.

1. Delivering top- and bottom-line growth

Domino's Pizza is usually a hit with consumers during the football season, and operational improvements, fresh marketing, and an easy-to-use app make this company incredibly intriguing.

While you shouldn't base future decisions on the past, the first quarter has usually been a boon for Domino's investors. Shares have climbed in the first quarter in 10 out of the past 10 years, returning a mean and median of 20.6% and 15.8%, respectively. As you can see in the following chart, this time of year has certainly been kind to the company in terms of revenue, so those gains aren't entirely surprising:

DPZ Revenue (Quarterly) data by YCharts.

Undeniably, heady growth could be a bit more difficult this year because comparisons are tougher following strong sales last year. Nevertheless, I think there's reason for optimism.

As fellow Fool Daniel Kline recently reminded us, Domino's has posted 22 consecutive quarters of year-over-year domestic same-store sales growth, and 13% growth in the third quarter was far from mediocre. Similarly, same-store sales grew a healthy 6.6% year over year in the quarter internationally, showing that it's not just the U.S. that's supporting results. Furthermore, that demand is producing enviable earnings, as third-quarter earnings per share of $0.96 outpaced industry forecasts by 6.7%, and reflect 43.3% upside from a year ago.

Clearly, demand for Domino's pizza remains strong, and operational improvements are allowing more of its sales to flow through to the bottom line. I think that trend will continue, and analysts seem to agree. Currently, they're targeting for Domino's to produce EPS of $5.14 in 2017, up from $4.25 in 2016. Assuming management can hit that forecast, investors should be rewarded.

2. Setting sights on silver

Owning some shares in the iShares Silver Trust is an intriguing hedge, given that precious metals have been on the decline and equity prices have been flirting with all-time highs.

Silver benefits from being an investment fairly uncorrelated to equities. It can also trade based on industrial demand, which can account for over 50% of total silver demand.

Therefore, if markets take a breather, silver could provide portfolios with some insulation against a decline. And if industrial production improves because of optimism over infrastructure spending or tax reform, then silver could still head higher, regardless of the direction of equities.

In either case, picking up silver at a 22% discount to its July peak could prove to be savvy:

3. Betting on an oil recovery

Oil and gas commodity prices began stabilizing in 2016, and with the natural gas heating season upon us, it wouldn't surprise me if shares in Pioneer Natural Resources Co. march higher.

Fool contributor Matt DiLallo wrote in October that Pioneer's dominance as a leader in shale production in the Permian basin positions it to profit from $50-plus oil, and I can't help but agree. The company has a solid balance sheet (relative to peers, it's pretty debt-free), and in December, management said its estimated production growth in 2016 was 14%.

Management also predicted in December that the company will grow production by between 13% to 17% in 2017, courtesy of five additional rigs. They also think Pioneer can grow production by a compounded 15% annually through 2020, assuming $50 oil, and that cash flow can grow by a compounded 25% annually over that same period. If management keeps a lid on drilling costs, and OPEC production cuts and U.S. demand growth prop up oil and gas prices, then this company's shares could be a winner.

4. Targeting more travel

As we saw with holiday spending, consumers are feeling a bit more flush than they have in the past, and with wages climbing, it may not be a stretch to bet that a bit more will be spent on travel this year.

If so, then Priceline is perfectly positioned. The company is a proven market-share leader, and its Bookings.com is a Goliath, with over 24 million bookable rooms listed. In Q3, Priceline continued to overdeliver on estimates, reporting that properties listed on Booking.com increased 29%, and that overall sales and gross profit grew 18.9% and 21.8%, respectively. Importantly, management said that Q4 total gross bookings could grow between 16% and 21%.

That optimism appears to be flowing over into industry-watchers' forecasts for EPS growth. This year, Priceline is expected to deliver EPS of $75.87, up from an estimated $64.63 for the full year 2016. Since shares can be bought for an arguably fair forward price-to-earnings ratio of 19.4, and Priceline continues to grow by double digits, there are good reasons to go long on this company's shares.

IMAGE SOURCE: BIG LOTS.

5. High hopes for the holidays

Big Lots' story is less about buying because its top line is growing (it isn't), and more about buying because it's becoming exceedingly profitable.

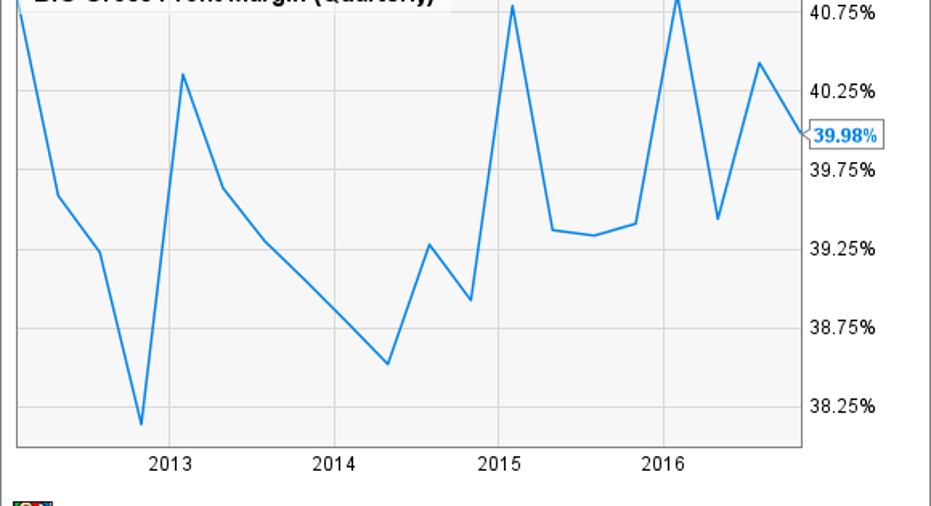

In Q3, sales slipped slightly as comparable-store growth flatlined, but gross margin inched up to 40% from 39.4% midyear, and over the past three years, trailing 12-month operating margins have increased from a low of around 4% to 4.96%. That profit growth is great news heading into the much more favorable fourth-quarter holiday shopping season:

BIG Gross Profit Margin (Quarterly) data by YCharts.

Furthermore, this is one company that has a lot of domestic exposure, and that means it could enjoy a lot of profit tailwinds if Donald Trump's corporate tax reform policies win support in Washington. Trump has proposed reducing the corporate tax rate to 15%; over the past 12 months, Big Lots' effective tax rate has been 37.44%. Looking at the potential tailwind differently, Big Lots' annual provision for income taxes is about $84 million, so we're not talking chump change.

10 stocks we like better than Big Lots When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Big Lots wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Todd Campbell has no position in any stocks mentioned.Todd owns E.B. Capital Markets, LLC. E.B. Capital's clients may have positions in the companies mentioned.Like this article? Follow him onTwitter where he goes by the handle@ebcapitalto see more articles like this.

The Motley Fool owns shares of and recommends Priceline Group. The Motley Fool is short Domino's Pizza. The Motley Fool recommends Big Lots. The Motley Fool has a disclosure policy.