5 Things Procter & Gamble Co. Management Wants You to Know

Image source: Getty Images.

Last week, Procter & Gamble (NYSE: PG) posted fiscal second-quarter earnings results that beat management's expectations. For the second straight quarter, sales growth was just ahead of projections even as profitability jumped higher.

On their conference call with Wall Street analysts, executives went into detail about the challenges and opportunities P&G experienced over the past few months. Here are a few of the key points that Chief Financial Officer Jon Moeller sought to get across to investors.

Growth

P&G posted 2% overall organic sales growth, which marked a decline from the prior quarter's 3% jump. However, that figure was impressive for a few reasons. First, it showed building momentum in a few key geographies. Organic sales have now improved for three straight quarters in the U.S. and in China, P&G's second largest market.

Second, the growth came despite economic challenges that the company did not anticipate, including currency disruptions in India and tough selling environments in Egypt, Turkey, and Argentina. Finally, the gains were volume driven, with volume rising a healthy 2% as pricing held steady.

Portfolio payoff

P&G finally has the portfolio that it has wanted for years, with the 66 brands it markets (down from 165) representing the fastest growing, most profitable franchises with the best long-term outlook for growth. CEO David Taylor and his team estimated last year that once the divestments are complete the new mix should produce one full percentage point higher organic growth. Shareholders should be encouraged by the early results showing that the brand-shedding process is finally starting to lift sales results.

Profitability

Procter & Gamble is making significant improvements to its already market-beating profitability. The company cut nearly $10 billion out of its cost structure over the last five fiscal years and aims to remove another $10 billion through 2021. These shifts added three full percentage points to profitability, which was just partially offset by increased promotions.

P&G operating margin is 21%, putting it ahead of nearly all its rivals, including Unileverand Kimberly-Clark.

Cash returns

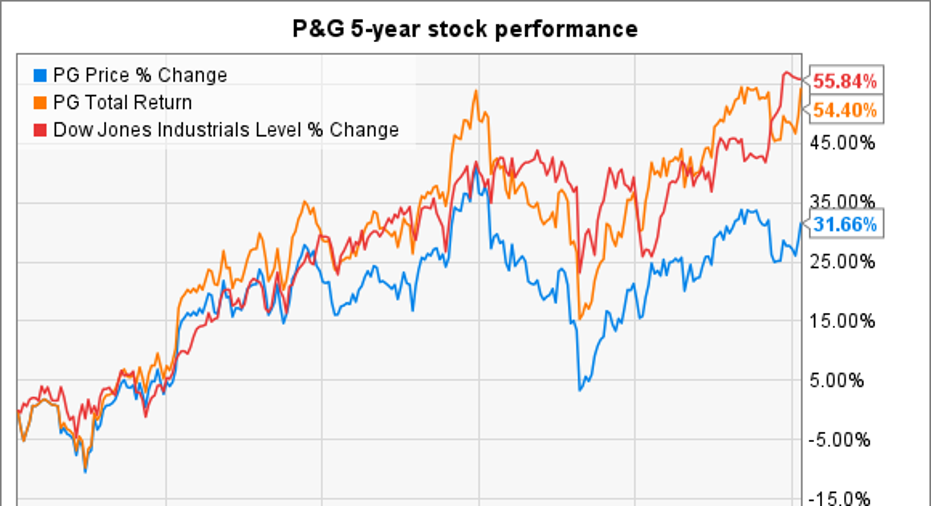

Investors were underwhelmed when P&G announced its smallest dividend raise in modern history last year, but the broader picture on cash returns tells a more positive story. Thanks to the funds it raised through selling off big brand franchises like Coty beauty products, the consumer goods giant is on pace to send $22 billion back to shareholders this year through a mix of stock repurchases and dividend payments. Investors should keep that in mind when judging the stock's performance. Sure, it has trailed the market by a wide margin over the last five years. But that gap disappears when you include dividends in the mix.

Raising guidance

Two quarters through the new fiscal year, P&G is optimistic about the business. In fact, executives raised their sales growth target to 2.5% from 2%, compared to the 1% uptick in 2016 and the flat result in the prior year. In part because of the economic challenges mentioned above, they left their earnings forecast unchanged. Still, the projected 5% profit uptick would be the first time in three fiscal years that P&G has hit its long-run earnings growth target.

10 stocks we like better than Procter and Gamble When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Procter and Gamble wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Demitrios Kalogeropoulos has no position in any stocks mentioned. The Motley Fool recommends Kimberly-Clark and Unilever. The Motley Fool has a disclosure policy.