5 Things Phillips 66's Management Thinks You Should Know

Phillips 66 (NYSE: PSX) isn't just hoping that 2017 will be a better year for the refining giant, it is planning on it. While the environment for refining isn't doing the company any favors as of late, management sees the company making some big strides in its other business units that should lead to better days ahead.

On the company's most recent conference call, management discussed how it foresees 2017 shaping up as well as covering some of the topics du jour such as tax reform. Here's a few snippets from Phillips 66's most recent conference call that should give you an idea of what management is thinking for this year and beyond.

Image source: Getty Images

Guidance for 2017: Tough start, but...

2017 hasn't exactly started out on a great foot for refining companies. Gasoline and diesel inventories across the U.S. are high, and the winter season is always a bit weaker in terms of demand. Several other execs in the refining business are already anticipating a tough year for refiners, but CEO Greg Garland thinks that these tough market conditions will start to improve as the year goes on.

One of the big benefits of Phillips 66 versus other refining companies is its large presence in Chemical manufacturing through its CPChem joint venture with Chevron (NYSE: CVX). On multiple occasions, Garland and other members of the Phillips 66 management team talked about the start-up of its $6 billion ethane cracker plant in the U.S. Gulf Coast. Once this comes online, it will allow CPChem to significantly lower its capital spending and throw off more cash to both Phillips 66 and Chevron.

Glut of Natural Gas Liquids opening new markets

Natural gas liquids has been an interesting business over the past couple years. While oil and gas production have slowed down a bit from less drilling, production of NGLs has remained rather strong. As a result, there have been a lot of opportunities for processing and chemical companies to take advantage of the cheap feedstocks. Here's the thing, though, according to Garland, the uptick in production for natural gas and oil is going to present a unique challenge for NGLs in the near future.

Phillips 66 and a small handful of companies could take huge advantage of this situation. NGL prices overseas are much higher, and they are much less costly to export than liquefied natural gas.Longer term, though, this continues to bode well for petrochemical manufacturing. Phillips 66 is looking to make a final investment decision on a second fractionator unit at its Sweeny complex with plans to add a third as well.

Getting DCP Midstream back on track

For all the things that have gone right for Phillips 66 in recent years, one that has not performed as well is its natural gas gathering business through its joint venture with Spectra Energy to co-own the general partner of DCP Midstream (NYSE: DCP). Both Spectra and Phillips 66 had to essentially give assets and cash to the fledgling company in 2015, and neither company has seen much in terms of cash contributions from the business. Recently, though, DCP Midstream made some major corporate changes between the general partner and the limited partnership. According to, CFO Kevin Mitchell, these changes should pay off relatively quickly for the parent companies:

The tax question

Of course, no recent conference call can go by without questions about the potential tax changes proposed by the Trump administration and how it would impact Phillips 66. Most execs have simply said "we're encouraged" or something like that, but Garland's response was a little more nuanced:

The thing with major changes to the current tax code is that there are a lot of moving parts that will have both beneficial and adverse effects to a business, so investors shouldn't simply look at tax reform as a universal good.

Future capital allocation

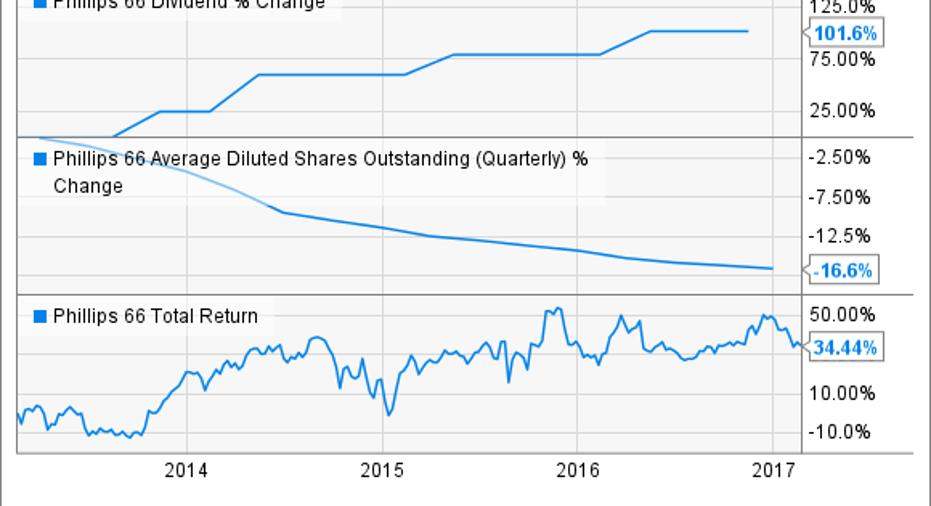

For most investors, Phillips 66 is a company with modest growth prospects, but one that generates lots of cash that can be returned to shareholders in the form of dividends and share repurchases. Ever since the company was spun off back in 2012, it has followed this plan and has generated decent returns for investors through good times and bad:

PSX Dividend data by YCharts.

For this formula to work, capital allocation -- and how capital allocation is prioritized -- is critical. According to Garland, there are pretty much two untouchable aspects of its capital spending, but the rest is up for debate:

With natural gas and naturalgas liquids remaining so cheap in the U.S. thanks to the shale boom, it would not be surprising if growth capital spending takes a little bit more priority in the coming years to build out even more petrochemical production and export capacity. Once those opportunitiesbecome fewer and further between, share repurchases will probably play a bigger role.

10 stocks we like better than Phillips 66When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Phillips 66 wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Tyler Crowe has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Spectra Energy. The Motley Fool recommends Chevron and DCP Midstream. The Motley Fool has a disclosure policy.