5 Things Chevron's Management Wants You to Know

Image source: Chevron investor presentation.

Chevron has been a little slow to respond to the decline in oil and gas prices. In some ways, it hasn't been able to, because it had so much capital spending tied up in large projects not yet producing. As more and more of those facilities come online, though, the company is gaining some more flexibility on what to do from here. Cutting costs is a large part of Chevron's current strategy, but it isn't the only thing that management is looking at.

To get a better idea of where Chevron goes from here, let's take a look at several management quotes from its most recent conference call. The five below give a pretty good picture as to what Chevron's management is thinking.

The short shift

A big lesson oil and gas producers have -- hopefully -- learned from this big disruption of the energy market is that there is an immense value in being flexible. The larger oil and gas companies like Chevron were too focused on megaprojects that can take decades to develop. This downturn left them with their pants down as cash flows from operations dried up and bills for projects were still coming due. Here's how Chevron is dealing with this, according to CFO Patricia Yarrington:

The way Chevron plans to do this is by shifting to shale oil and gas production. It takes much lower upfront capital before a well comes online, and the short development cycle means capital spending can fluctuate rather quickly. Chevron expects to increase its capital spending on its current production base and short-cycle investments like shale from 40% in 2015 to 65% by 2018.

Aggressive asset sales

Despite this strategy shift, there is a bit of a hangover from the company's megaproject spending and the downturn in oil prices. To get back to profitability and fill the funding gaps, Chevron has been rather aggressive about asset sales. It appears that this trend isn't stopping any time soon. Yarrington went into a little more detail into the company's planned asset sales over the next couple of years:

The one thing that is slightly concerning about these announced deals is that so much of them are concentrated on the downstream side -- refineries, pipelines, retail, etc. Even before these proposed sales, Chevron was the most production-oriented of the large integrated oil and gas companies. Shedding these assets will only make it more exposed to the ups and downs of the oil market.

Can it raise the dividend?

Chevron and ExxonMobil are the only two integrated oil and gas companies that qualify as dividend aristocrats. With cash flows looking tighter than ever, though, Chevron's ability to raise its dividend is looking a little precarious. In response to a question about a potential dividend raise, this is what Yarrington had to say:

That's a pretty complex way of saying "we're going to try our damnedest to keep the dividend streak alive." With so many investors basing their investment on the idea that Chevron will keep raising its dividend, it would be hard for the company to not continue to do so. Chances are, Chevron's management and board will decide on a token raise to keep its dividend streak alive, but don't expect a big raise that would further compromise its cash flows.

Shale is the solution for now

Continuing with the statements that Yarrington made about the need for shorter-cycle investments like shale, Joseph Geagea, the executive vice president of technology, projects, and services, highlighted Chevron's potential as a shale producer. Notably, he focused on the advantages the company has over many other companies in the Permian Basin.

Unlike many newer independent oil and gas producers that had to sign lease agreements with landowners to pay royalties, Chevron was already sitting on large tracts of land from legacy production that can be developed for its shale rock. This is how the company is able to generate decent rates of return at a lower cost of oil. Whether this kind of performance can be replicated in other basins is questionable since the Permian position enjoys the benefits of infrastructure and no royalty rights, but Permian will be a good place to get production while oil prices are extremely low.

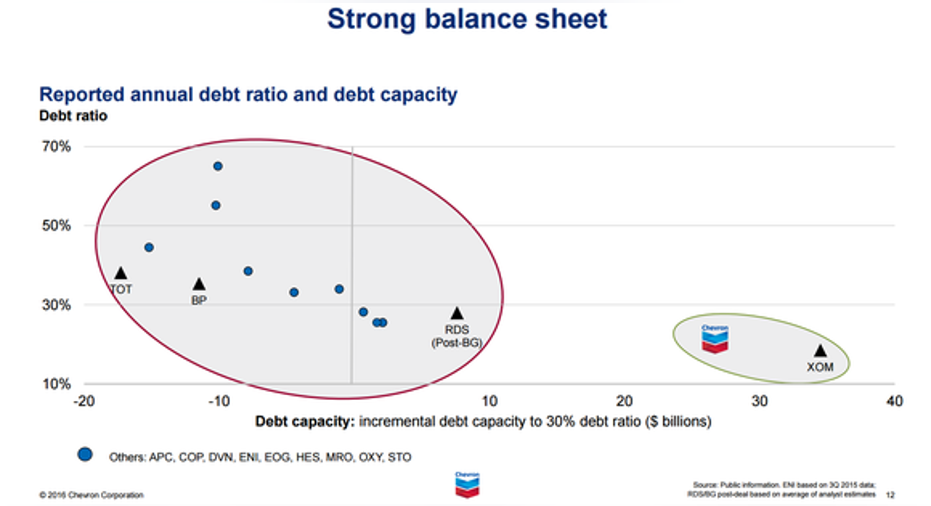

Any more appetite for debt?

Debt has been one of the saving graces for Chevron and many others during this downturn, and as Chevron has highlighted in some of its recent investor presentations, both it and ExxonMobil hold a huge advantage over many of its peers in terms of balance sheet strength.

Image source: Chevron investor presentation.

At the same time, though, the company's asset sales and capital spending cuts probably won't be enough to cover its cash needs until 2017, by managements estimates. That means Chevron will probably need to tap the debt market some more in the interim to meet its cash needs. While some analysts were curious if management was getting a little nervous about this, Yarrington pointed out that the company still has a little more appetite if necessary:

As much as debt can be a burden, the way that Yarrington has explained it here is a pretty good read on the situation. The problem with it, though, is knowing when a company is at the top of the cycle. A long period of high prices could be all it takes for companies to act a little cavalier with debt.

What a Fool believes

There was a lot to digest from Chevron's recent conference call, but the overarching theme is that the company is making a large push into short-development-cycle investments like shale drilling and is using any means possible to plug the funding gaps in the next couple of years.

Probably the most important thing for investors to watch in the long term is that debt situation. Sure, the company probably does have the strength to take on a bit more debt in the interim to cover cash needs, but once oil prices are in a better place, we will want to see that debt level get reduced significantly so the company can get ready for the next downturn, whenever it happens.

The article 5 Things Chevron's Management Wants You to Know originally appeared on Fool.com.

Tyler Crowe owns shares of ExxonMobil.You can follow him at Fool.comor on Twitter@TylerCroweFool.The Motley Fool owns shares of ExxonMobil. The Motley Fool recommends Chevron. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.