5 Reasons to Buy American Water Works Now

It's impossible to know for sure what the future holds, but many investors feel that the market will soon encounter volatility. And when uncertainty arises, attention often turns to more conservative stocks -- like water utility American Water Works (NYSE: AWK), an industry leader. Whether or not that attention is due to fears of volatility, however, plenty of reasons suggest that now is a swimmingly good time to buy shares.

Image source: Getty Images.

1. Below the high-water mark

Trading at approximately 27.5 times trailing earnings, American Water Works may seem expensive in light of the fact that its five-year average price-to-earnings ratio is 22 (according to Morningstar), while the industry average is 20.9. But relying solely on one metric and ignoring the company's peers can be misleading:

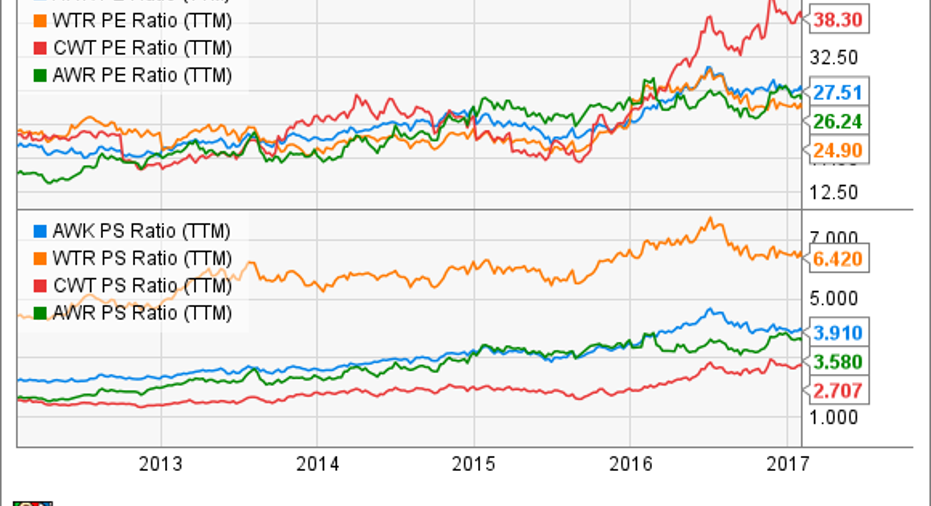

AWK PE Ratio (TTM) data by YCharts.

Stacking the company up against its peers, we find that it is not unreasonably valued. California Water Service Group (NYSE: CWT), has a five-year average P/E of 22.9, only slightly higher than American Water Works' five-year average; however, it currently trades at a much richer 38.3 times trailing earnings. Aqua America (NYSE: WTR), on the other hand, appears to trade at the most attractive valuation in terms of trailing earnings, but in those terms, investors must pay considerably more than they would for other companies in the space.

Perhaps the stock's valuation -- in terms of earnings and sales -- seems unconvincing. Let's look at one more metric:

AWK Price to CFO Per Share (TTM) data by YCharts.

Turning to the stock's price in terms of cash from operations per share, we find that American Water Works is a bargain -- especially compared to the 18.2 multiple at which American States Water Company (NYSE: AWR) trades. Although the figures above may not suggest that the company is a screaming buy, they certainly indicate that the stock is reasonably valued.

2. Increasing drops in the dividend bucket

Although some investors turn to utility stocks as a hedge against volatility, others turn to them because of the dividends. From fiscal 2011, when American Water Works paid dividends of $0.90 per share, to fiscal 2016, when it paid $1.47 per share, the company achieved a compound annual growth rate (CAGR) of 10.2%. Intending to keep future dividend increases aligned with earnings-per-share (EPS) growth, management has targeted a payout ratio of between 50% and 60% of earnings. Over the past five years, the company has maintained a payout ratio within this range, suggesting that investors can trust management's ability to achieve this goal.

3. This advantage blows peers out of the water

Providing water services to about 15 million customers in 47 states, plus Washington, D.C., and Ontario, American Water Works retains a competitive advantage over competitors that operate in fewer areas. Aqua America, for example -- American Water Works' closest competitor -- provides services to 3 million people in only seven states. The geographical diversity of the company's operations mitigates the risk associated with adverse regional weather conditions; competitors American States Water Company and California Water Service Group are both concentrated in California, which is currently suffering from a historic drought.

Besides reducing risk, geographic diversity affords American Water Works a significant opportunity to make acquisitions, a key component of its growth strategy, for it seeks businesses in proximity to areas where it already has operations. When the company releases its fiscal 2016 earnings, management expects to report that it has added about 42,000 customers during the year due to acquisitions -- about 76% more than the approximately 24,000 customers it added through acquisitions in fiscal 2015.

4. This head is well above water

Dealing primarily in regulated businesses -- representing 87% of operating revenue in fiscal 2015 -- American Water Works has the ability to forecast with a fair degree of certainty. For example, the company foresees continued improvement in its O&M efficiency ratio; this ratio of O&M (operations and maintenance expenses) compared to operating revenue is a non-GAAP (generally accepted accounting principles) metric similar to "operating margin."

American Water Works has consistently reported improvement in its O&M efficiency ratio. Image source: American Water Works corporate presentation.http://ir.amwater.com/Cache/1500094194.PDF?Y=&O=PDF&D=&FID=1500094194&T=&IID=4004387

In a corporate presentation from last December, management reported that for the 12 months ended Sept. 30, 2016, the company achieved an O&M efficiency ratio of 34.9% -- an improvement of 930 basis points since 2010. Management recognizes the opportunity to achieve even greater efficiency in the years ahead, identifying a stretch target of 32.5% by 2021.

How does this efficiency translate to earnings growth? Management has identified an EPS-growth CAGR target of between 7% and 10%, from the $2.64 it reported in fiscal 2015 through 2021.

5. Keeping an eye on Keystone

Proving that the company is not averse to growing its market-based business segment, American Water Works acquired Keystone Water Solutions, a provider of water-management solution services to the natural gas exploration and production companies in the Appalachian Basin, for $133 million in 2015. On the company's third-quarter conference call, Susan Story, American Water Works' president and CEO, suggested that Keystone will be EPS-neutral in fiscal 2016 due to "the timing of ramp-ups and work completion schedules." But that's not to say the subsidiary wasn't successful. Story reported on the call that Keystone has grown its market share from about 20% when it was acquired in July 2015 to about 35% at the end of Q3.

As with the advantages afforded by the geographical diversity of its operations, the company's exposure to the natural gas market provides it a path to profitability that complements the regulated-businesses segment.

The takeaway

Although they're not the most exhilarating of investment opportunities, water utility stocks certainly represent worthy considerations for investment. And of these, the industry leader warrants considerable attention, since numerous reasons suggest that an investment in American Water Works will hold water.

10 stocks we like better than American Water Works When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and American Water Works wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of January 4, 2017

Scott Levine has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.