5 Reasons Investors Are Shorting Main Street Capital

Since the end of 2015, business development company (BDC) Main Street Capital has emerged as one of the most heavily shorted stocks in its industry. Short interest has risen to 3.6 million shares, roughly equivalent to 15 days of average volume. Some brokers are charging as much as 12% to borrow shares to short for one year.

Why are investors so eager to short Main Street Capital? Here are a few reasons:

1. High valuationDespite a market rout that affected many peers in its industry, Main Street Capital has maintained a valuation at a healthy premium to book value. Shares trade at about 1.49 times book value compared to a valuation of 0.78 times book value for publicly traded BDCs. A more closely comparable mix of BDCs trades at about 0.88 times book value.

2. Declining portfolio metricsRecently, I noted that Main Street's controlled companies weren't carrying the weight they once were. Businesses in which Main Street owns a 25% or greater equity stake saw their dividend growth slow in 2015. Four of these companies appear distressed, paying out significantly less to the company than they did in 2014.

3. Oil and gas exposureAbout 9.4% of Main Street Capital's investments were directly tied to oil and gas and services at the end of 2015. Because the company is leveraged, losses in its portfolio have an outsize impact on book value.

If these investments were written off completely, Main Street Capital's net asset value would decline from $21.24 per share at the end of 2015 to $17.88. That's a nearly 16% decline in book value from the loss of less than 10% at the asset level. Leverage, unfortunately, swings both ways.

4. Indirect oil exposureJust because a company isn't an oil producer doesn't mean that it won't be affected by low oil prices.

In fact, if you look at the companies that paid smaller dividends back to Main Street Capital in 2015, you'll find that all but one has a tangential relationship to oil and gas. Being a Houston-based financier, the company has exposure to a substantial, but difficult to quantify, number of companies that will see their business ebb and flow with oil prices despite being classified in other industries.

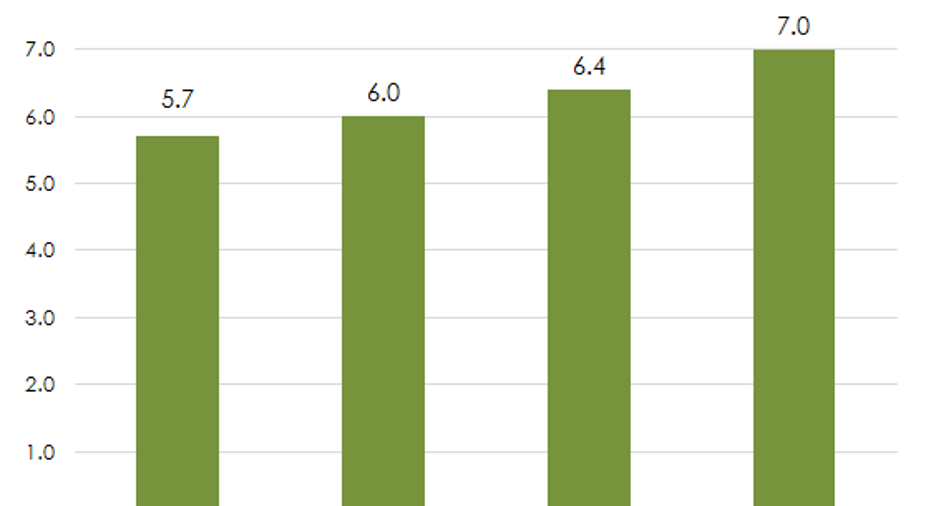

5. Higher multiplesMain Street Capital must report the value of its investment portfolio every quarter. It does this by ascribing a valuation to each of its investments, adding them up, subtracting its debt, and dividing the value between all its shares outstanding.

From its own filings, one should note that the multiple that Main Street Capital uses to value its weighted average equity investment has risen from 5.7 times in 2012 to 7.0 times in 2015.

This can happen for two reasons: Either its portfolio companies' EBITDA generation is declining and their valuations are holding flat with the help of a higher multiple, or it is using a higher multiple on its portfolio companies and writing up their valuations on its balance sheet.

For its part, Main Street executives have discussed how some of its portfolio companies are getting sold to buyers at higher and higher prices. Whether or not this trend is sustainable is questionable, and it's possible that its portfolio companies may be carried at a price they wouldn't sell for today.

In short, Main Street Capital is trading at a significantly higher valuation than its peers, despite the fact that its underlying portfolio of investments may not be performing as well as they once were. Given that Main Street trades at nearly twice the book value multiple of its peers, it's more than priced for perfection.

The article 5 Reasons Investors Are Shorting Main Street Capital originally appeared on Fool.com.

Jordan Wathen has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.