5 Must-See Slides From Procter & Gamble Co.'s Analyst Presentation

Procter & Gamble (NYSE: PG) this week held a meeting with Wall Street analysts during which the management team discussed its plan to return to healthy sales growth. The presentation spanned almost 200 slides and delved into topics like cost cuts, portfolio simplification strategies, and market share growth opportunities.

Below are a few of the slides from the chat that shareholders won't want to miss.

Making progress

Image source: Procter & Gamble.

Executives are encouraged by P&G's latest operating trends. Organic growth clocked in at 3% to start off fiscal 2017, compared to 1% over the final six months of the prior year. This growth has been broad based, management said, with its two largest markets, the U.S. and China, both showing a steady rebound.

The company's improving volume trends contrast with rivals like Kimberly-Clark (NYSE: KMB), which last quarter saw its growth pace decelerate. The two rivals compete most directly in the diaper category, where P&G has recently clawed back market share in its Pampers and Luvs brands.

Simplification

Image source: Procter & Gamble.

It is well known that P&G has been aggressively whittling down its portfolio to a more manageable size. It now owns just 65 brands, down from 170. Yet that simplification strategy is finding even more traction behind the scenes. P&G has slashed the number of manufacturing sites it employs, driven down its headcount lower by 35%, and cut its advertising agency relationships in half.

So far, these changes have produced just minor impacts on the top and bottom line. However, their real value should accrue over time as P&G better adjusts to changing consumer preferences under a less burdensome cost structure.

Productivity effects

Image source: Procter & Gamble.

P&G is boosting its cost cutting program with the aim of slicing $2 billion out of annual costs over each of the next five fiscal years. Most of the gains will come from its cost of goods sold expenses, where management has already found success in producing savings. The next $10 billion of savings will come from initiatives like adding digitalization and automation to the production lines, simplifying manufacturing platforms, and completely overhauling its distribution network. The company plans to plow the resulting cash into revenue-boosting projects like increased advertising and research & development.

Winning in the laundry room

Image source: Procter & Gamble.

The fabric care business, anchored by brands like Tide and Gain, is critical to P&G's long-term success. CEO David Taylor and his team see several ways that the company can spark faster sales growth in this division, including by promoting premium laundry options like Tide Pods while encouraging customers to toss in an extra pod or two for heavy loads.

Thanks to a mix of innovation wins and marketing muscle, P&G's fabric care segment is performing well. Sales growth is up in each of its top two markets, the U.S. and Japan, and executives see those successes easily translatable to other areas of the portfolio.

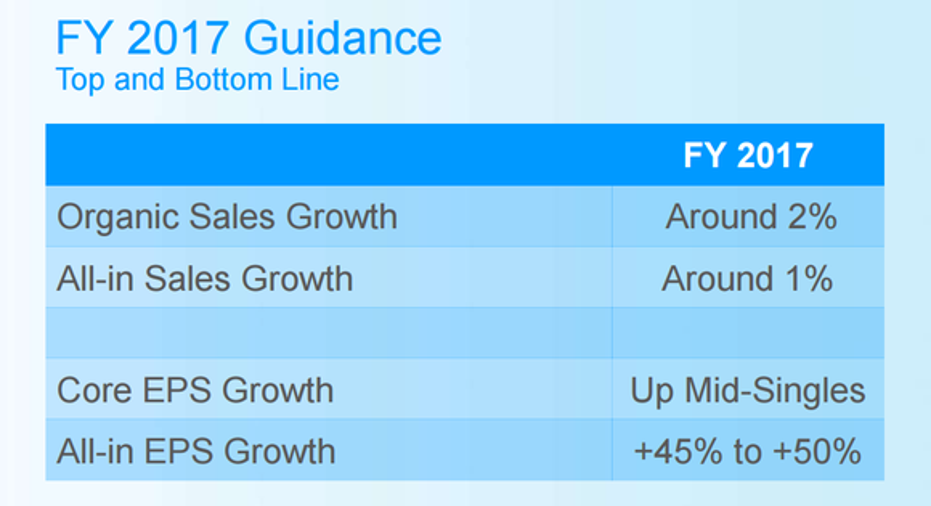

Cautiously optimistic

Image source: Procter & Gamble.

P&G believes it can achieve 2% organic sales growth this year for its first sequential improvement on that metric in years. Its core earnings per share, meanwhile, should increase by around 5%, which would mark a return to its long-run target after two straight years of underperformance. Efficient cash generation -- plus proceeds from brand divestments -- should help P&G multiply those gains into huge cash returns to shareholders (as much as $22 billion in fiscal 2017).

Management doesn't see big improvements coming on the economic front, and instead the team highlighted slowing market growth rates around the world and continued volatility in foreign currencies. Even if it hits its sales targets, meanwhile, that wouldn't mark the end of its stubborn streak of minor market share losses.

That's why it will be important for investors to watch P&G's organic growth rate over the next several years, particularly whether it is moving back toward a market-beating pace and whether it is composed of a healthy mix of pricing and volume gains.

Forget the 2016 Election: 10 stocks we like better than Procter and Gamble Donald Trump was just elected president, and volatility is up. But here's why you should ignore the election:

Investing geniuses Tom and David Gardner have spent a long time beating the market no matter who's in the White House. In fact, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the ten best stocks for investors to buy right now... and Procter and Gamble wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of November 7, 2016

Demitrios Kalogeropoulos has no position in any stocks mentioned. The Motley Fool recommends Kimberly-Clark. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.