4 Biotech Stocks to Buy in January

When an entire sector goes on sale it tends to create bargains. There's no doubt that the biotech sector has the blue-light special flashing right now, as it has massively underperformed the S&P 500 year to date. Knowing that, we asked a team of healthcare contributors to highlight a biotech stock that they think is a smart buy as we head into 2017. Read on to see why they pickedTrevena (NASDAQ: TRVN),Ligand Pharmaceuticals (NASDAQ: LGND),ACADIA Pharmaceuticals (NASDAQ: ACAD), and Geron (NASDAQ: GERN).

Image source: Getty Images.

This clinical-stage biotech could shine in the new year

George Budwell(Trevena): The clinical-stage biotech Trevenais set to release top-line results from two phase 3 studies (APOLLO-1 and APOLLO-2)for its lead drug candidate, oliceridine, in the first quarter of 2017. The short story is that oliceridine is an injected drug indicated for the treatment of moderate to severe pain in a post-surgical setting.

This experimental drug is worth a deeper dive right now because the acute pain market is massive (more than $11 billion in just the U.S.), and there's a desperate need for viable alternatives to highly addictive drugs like morphine. In other words, this particular drug market has all the factors in place to potentially produce a highly lucrative product.

Now, the first thing to understand about oliceridine's ongoing studiesis that the primary endpoint for both trials is the drug's ability to outperform placebo as a pain reliever -- a feat it has performed in spades in its mid-stage trials that even led to a breakthrough therapy designation from the FDA last February. So I'm willing to go out on a limb here and say thatoliceridine will most likely hit the mark in each trial in terms of its primary endpoint. Pain relievers, after all, either work or they don't, and all the evidence so far clearly suggests thatoliceridine is indeed an effective pain reliever.

Butoliceridine's value proposition actually depends on how well it stacks up against morphine from both a safety and efficacy standpoint, which is the secondary endpoint in each trial.If oliceridine produces a favorable clinical profile relative to the gold standard, morphine, it could end up generating hundreds of millions in sales. That's an enormous potential haul for a company with a market cap of around $300 million.

So while it's probably unwise to back up the truck with this speculative biotech stock, I do think it's worth owning a small position in caseoliceridine hits pay dirt next year.

Having said that, there is a compelling bear case surroundingoliceridine's ultimate commercial potential that shouldn't be taken lightly. In short, bears have suggested that oliceridine's target market is only a small fraction of the broader acute-pain space, and Trevena may be unable to convince payers to provide coverage for what will almost certainly be a far more expensive drug than morphine.

Those are definitely fair arguments that could play a huge role if oliceridinedoesn't clearly differentiate itself from morphine in both of these trials -- and underscore why investors may want to keep any position on the small side for the time being.

The only game in town

Brian Feroldi(ACADIAPharmaceuticals): Introducing a new drug to the market can be challenging, but the odds of success go up when there isn't any competition to worry about. That's the situation that ACADIA Pharmaceuticals is in right now as its drug Nuplazid is the first and only FDA-approved treatment for Parkinson's disease psychosis (PDP).

Nuplazid launched for sale only a few months ago, but the early results are encouraging. Total sales in the third quarter came in at $5.3 million, which was more than double what analysts were expecting. That's nowhere near close enough to offset the company's massive spending, but it is a good start.

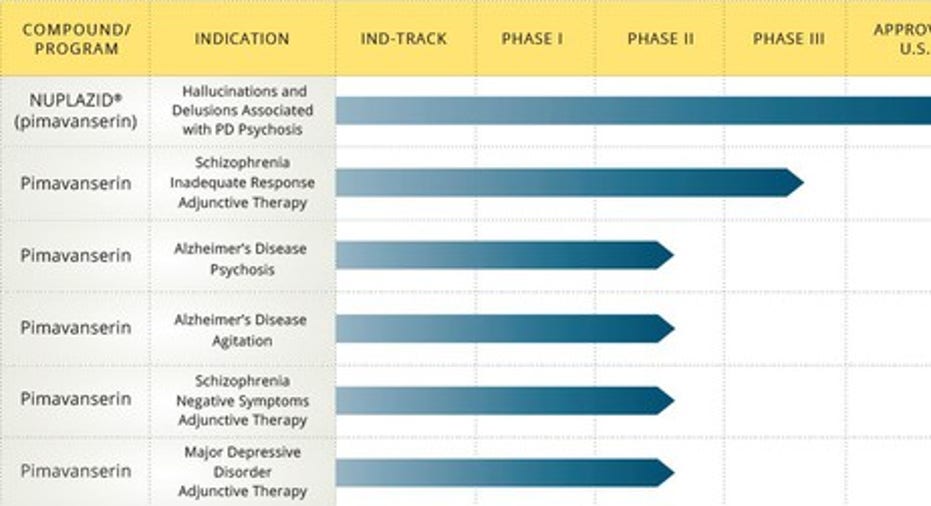

While Nuplazid has just barely started to scratch the surface of the PDP market, management is also pushing for expanding the drug's labeling.

Here's a look at the drug's other potential uses.

Image source: ACADIA Pharmaceuticals.

While finding success in other indications is never guaranteed, Nuplazid has already made it through the regulatory approval process once, so I'd argue it has a better-than-average chance of doing so again.

In total, ACADIA offers investors plenty of reasons to believe that it will show incredibly fast growth in the years ahead. With shares currently trading at a discount, I think it is a fine time to consider getting in.

Look out, Jakafi

Cory Renauer(Geron): My biotech stock pick to begin the new year suffered a market beat-down in 2016, and is now one of its industry's most intriguing long-term value plays. The company doesn't have a product to sell yet, but its lead candidate, imetelstat, has produced compelling trial results that suggest it could eventually dominate a somewhat underserved niche.

Geron's partner Johnson & Johnson is expecting more data from ongoing studies with imetelstat in 2017. If myelofibrosis trial results are consistent with previous observations, the healthcare behemoth will help fund larger trials in order to support New Drug Applications.

Currently, the only treatment for myelofibrosis is Incyte's Jakafi, which generated sales and royalty revenue at an annualized run rate of $1.01 billion based on third-quarter results. It earned FDA approval in 2011 based on its ability to reduce spleen size, a symptom of the disease. Geron's imetelstat, though, is the first to show clear signs of reduced disease activity and even drive the rare blood cancer into complete remission.

At recent prices, Geron's enterprise value is a mere $340 million. With a deep-pocketed partner ready to usher imetelstat through the regulatory pathway and into the commercial setting, there's a solid chance Geron could provide market-thumping returns to patient investors.

A small biotech with a big biotech's pipeline

Keith Speights(Ligand Pharmaceuticals):Try to find a biotech with a market cap less than $3 billion that has a deeper pipeline than Ligand. I don't think one exists. Ligand has eight programs in late-stage clinical studies and a whopping 18 in mid-stage studies. That count rivals much larger biotechs.

Ligand's key to success is its partnerships. The company has over 90 partners and licensees for its drug development platforms. If you threw a dart at a dartboard with the names of the biggest drugmakers in the world, there's a good chance that you'd hit one of Ligand's partners.

The big draw for Ligand's products is that they help biopharmaceutical companies develop new drugs more effectively. Ligand's leading technology, Captisol, has a chemical structure that improvessolubility, stability, bioavailability, and dosing of active pharmaceutical ingredients.

During the first nine months of 2016, Ligand's revenue soared nearly 40% compared to the prior-year period. With climbing sales of current products Kyprolis and Promacta and its robust pipeline likely to crank out more winners, I expect Ligand to keep up this pace of growth for the next several years.

10 stocks we like better than Geron When investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Geron wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of Nov. 7, 2016

Brian Feroldi has no position in any stocks mentioned. Cory Renauer owns shares of Johnson and Johnson. George Budwell has no position in any stocks mentioned. Keith Speights has no position in any stocks mentioned. The Motley Fool recommends Johnson and Johnson. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.