3D Printing: 2 Reasons to Buy, 1 Reason to Sell

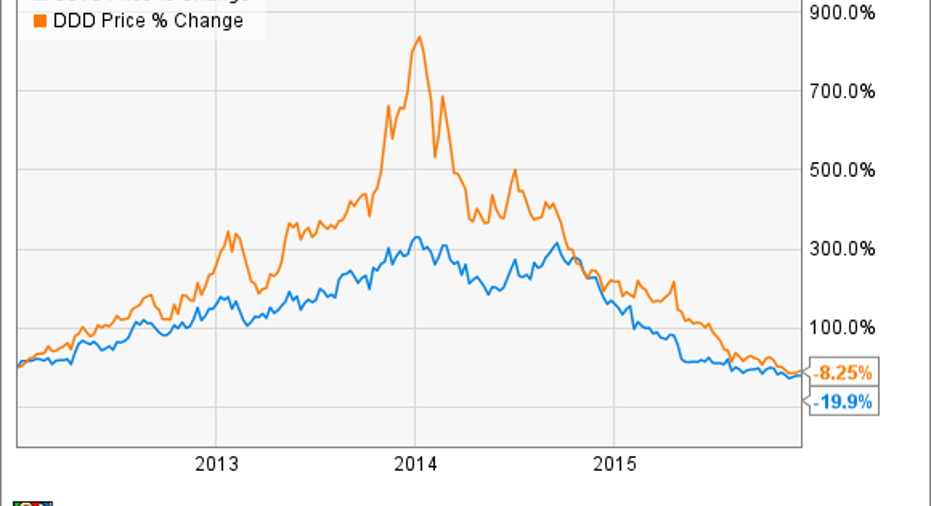

Investors in 3D printing have gone from elation to heartbreak in only a few years:

While much of the peak was a product of exuberance from an investing world that pushed 3D printing stocks to what in hindsight looks like crazy premiums, there's likely to be an eventual recovery in the slowed pace of demand that's hitting the industry right now. And while it's hard to say ifStratasys,3D Systems, or any of the smaller players out there will ever see their stocks return to previous highs, there's still huge expectations for the industry itself.

We asked three of our contributors with strong knowledge of the industry to chime in with some insight. Two of our contributors still see opportunity out there, while one of our experts thinks it's best to stay away -- at least for now. Here's what they had to say.

Rich Smith: It's been a long time since I was optimistic about 3D printing as an investment -- and it was the nosebleed valuations at Stratasys, 3D Systems, and ExOnethat jaded me. That said, Iamoptimistic about 3D printing as a technology, and I've long thought that the way to play it was to focus not on the razors, but on the blades.

I'll explain.

Long ago, way back when Gillette was still an independent company, it was legendary for having perfected the business model of selling a razor cheaply and making its real profits selling consumable "blades" for shaving. In the 3D printing paradigm, the printer-makers Stratasys, 3D, and so on are all trying to sell you "razors," but the real money is still in "blades" -- the raw-material "ink" that will be used to 3D-print physical objects.

Even more than a quarter century after Stratasys and 3D first set up shop, it's still early innings for the 3-D printing industry. From simple prototyping of products, 3-D printers are rapidly moving into new uses for their products -- batch production of special orders, specialized production of engine parts, and even food production. As these uses grow, I see big things ahead for the companies that manufacture the raw materials that make up 3-D-printed products.

I'm not the only one. Recently,The Wall Street Journalran a story on how minersRio Tintoand others are hoping to capitalize on the 3D printing craze by persuading big 3D manufacturers to use their titanium dioxide (TiO2) product to 3D-print objects. Industry experts interviewed for theJournalstory called 3D demand for TiO2 a potential "turbocharger" for their profits and said demand for the product should grow at as much as 24% annually over the next five years.

And titanium dioxide is just one of many raw materials that can be used to 3-D-print products. As time goes on, I'm sure we'll be hearing about -- and investing in -- many, many more. Stay tuned.

Steve Heller: Although shares of Stratasys and 3D Systems appear "cheap" on a relative basis after losing between 80% and 90% of their respective value from their all-time highs, there's no law in investing that says big sell-offs often result in huge turnarounds. To be clear, investors could face tremendous losses initiating positions in Stratasys and 3D Systems today -- especially if the underlying fundamentals continued to deteriorate, which isn't out of the question.

After all, the 3D printing industry is currently experiencing a period of falling demand from its largest adopters, and competition is expected to intensify next year with several well-funded new entrants -- all while 3D Systems and Stratasys face ongoing operational challenges. These circumstances aren't exactly ideal conditions for a turnaround.

For starters, 3D Systems' third-quarter 3D printing hardware revenue fell 22% year over year, while Stratasys' fell 37% -- not an encouraging sign for the "razor" aspect of their razor-and-blade models, which fuels the repeated sale of high-margin consumables over the long haul.

Secondly, Hewlett-Packard, Cabon3D, and Canon are expected to release proprietary 3D printing technologies in the next year or two that address many of the shortcomings believed to be holding back adoption. If successful, these new entrants could loosen 3D Systems' and Stratasys' stronghold on the industry and weaken their business prospects.

Finally, 3D Systems and Stratasys both have struggled with execution in recent years, prompting action from their respective management teams to completely reevaluate their businesses, streamline their operations, and improve performance. In reality, any restructuring efforts taken by management would probably weigh on their results in the near term and possibly longer.

Ultimately, it's one thing to buy a stock when the underlying fundamentals haven't deteriorated as severely as the fall in the stock would suggest. But it's an entirely different thing when the underlying fundamentals have changed since the stock's highs, which I think is the case with 3D Systems and Stratasys. I'd stay away.

Jason Hall: One of my worst investing moves of 2015 was buying 3D stocks. In February, I bought shares of Stratasys, 3D Systems, and ExOne, nearly doubling my holdings in all of these companies. Things have been awful since, with sales declining across the board, companies taking writedowns on asset values, and the general outlook going from exuberant to terrified in what felt like overnight.

But the 3D printing story is far from over, and the expectations remain high for huge industry growth over the next decade. This growth will be driven by technological advancements, as well as more companies that use 3D printing within their businesses.

As Steve pointed out, the former highfliers in the industry will be dealing with a lot more competition in the coming years, but I'm far from convinced that it signals a death knell for the current players. After all, companies such as HP and Canon have background in ink and laser printing, which has very little in common with 3D printing, which is as much a marketing term as a descriptor of what these machines actually do.

Furthermore, the new entrants are large companies fighting a slow death in their core printing businesses, as technology moves business and society away from paper. Frankly, I'm far from convinced that these companies will be able to solve the challenge of 3D printing simply by throwing money at it.

In summary, it's apparent that most of the problems at 3D Systems and Stratasys -- and to a lesser extent the smaller players -- is confined to the walls of those companies. They both went on spending, merging, and acquiring binges and are now paying the piper as they're forced to step back, rationalize their businesses, and focus on profitable, organic growth.

I think over the next year, investors will have opportunities to invest in these companies again, with solid upside for long-term gains. It's very painful right now -- I know firsthand -- but this downturn is forcing the industry's biggest companies to reevaluate their businesses and make some hard decisions. It could turn out to be the best thing that ever happened to them.

The article 3D Printing: 2 Reasons to Buy, 1 Reason to Sell originally appeared on Fool.com.

Jason Hall owns shares of 3D Systems, ExOne, and Stratasys. Rich Smith has no position in any stocks mentioned. Steve Heller owns shares of 3D Systems and ExOne. The Motley Fool recommends 3D Systems and Stratasys. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.