3 Ways Procter & Gamble Co. Is Beating the Competition

Procter & Gamble (NYSE: PG) is on stronger footing these days. Its fourth-quarter expansion pace recently edged past Kimberly-Clark's (NYSE: KMB) for the first time in over two years. Sales volumes were nearly as high as Unilever's (NYSE: UL), too.

Yet P&G is still on track to lose a slice of market share this year even as it closes that critical gap with rivals. Still, there are some important areas that P&G comes out well ahead of its peers.

Image source: Getty Images.

Profitability

The company is one of the most profitable in its peer group, for one. Gross profit margin improved by nearly a full percentage point last quarter as its efficiency gains far outweighed the impact of higher commodity costs.

Currency exchange rates significantly understate that profitability gain. Strip out the currency shifts and the company's gross margin actually rose by 1.2 percentage points, thanks to over 2 percentage points of gains from its $10 billion cost-cutting program.

PG Operating Margin (TTM) data by YCharts.

Operating margin improved to 22% last quarter, putting it well ahead of Unilever's 15% and Kimberly-Clark's 18%. In fact, only Colgate (NYSE: CL) has P&G beat in this core metric.

Marketing

Few companies in the world can claim anything approaching Procter & Gamble's marketing strength. It invests nearly $5 billion in advertising each year, making it the single biggest spender on the market.

Image source: P&G investor presentation.

Its marketing program is about much more than just ads. P&G also has the biggest sampling program around. Through partnerships with hospitals around the country, it delivers test packs of Pampers diapers to a whopping 70% of new moms each year. That program has helped expand the franchise's market share lead over Kimberly-Clark's Huggies recently.

The same goes for Gillette's premium razors, which P&G sends to millions of young men in hopes of creating lifelong customers. Unilever can try to challenge that brand's dominant hold on the market, and it has found some success with approaches like the Dollar Shave Club subscription offering. It's hard to make big gains against a franchise that's backed up by such a relentless stream of marketing support, though.

Cash returns

P&G's dividend yield is just below most of its rivals, and its recent growth pace trails peers, too. The company's 1% raise last year was its smallest in over a decade, and was trounced by the 5% increase Kimberly-Clark just announced.

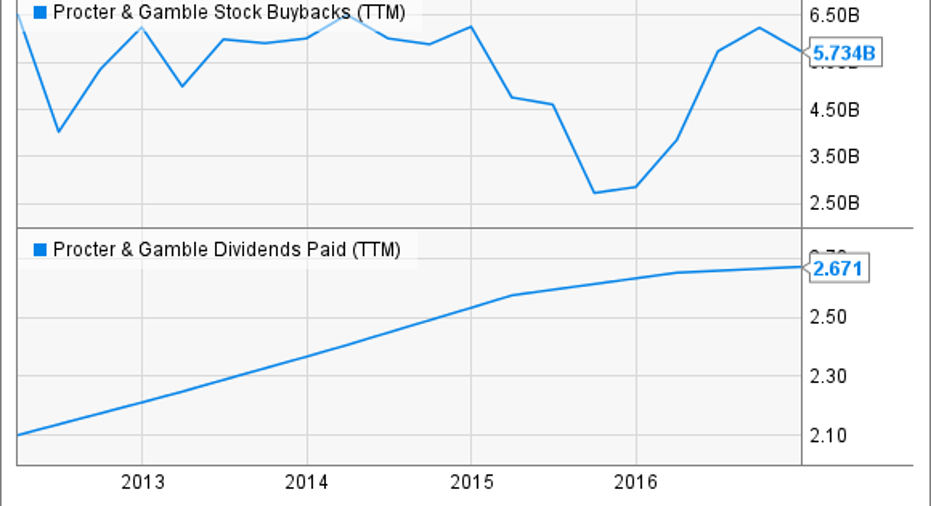

Zoom out and consider its broader capital return program, though, and you'll find that P&G can't be matched in this area. Kimberly-Clark sent $2 billion to shareholders over the last 12 months while Procter & Gamble, with help from its aggressive brand divestment program, is on track to deliver $22 billion to its owners. That equates to almost 10% of its market capitalization, or double Kimberly-Clark's commitment.

PG Stock Buybacks (TTM) data by YCharts.

P&G isn't planning another multibillion dollar brand sale on par with 2015's Duracell exchange or last year's beauty product divestment. Yet the company still plans to send about $18 billion back to shareholders, mainly through stock repurchases, over each of the next two fiscal years.

Management's hope is that by that time P&G will be growing at a fast-enough pace, and with strong-enough profitability, to push overall shareholder returns back to market-thumping levels. The company isn't enjoying balanced sales and earnings gains yet, but it is at least moving in that direction. Its core earnings are set to grow for the first time in three years in 2017 as sales gains finally accelerate after a brutal stretch of declining or flat organic revenue.

10 stocks we like better than Procter and GambleWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Procter and Gamble wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of February 6, 2017

Demitrios Kalogeropoulos has no position in any stocks mentioned. The Motley Fool recommends Kimberly-Clark and Unilever. The Motley Fool has a disclosure policy.