3 Turnaround Stocks to Watch in Retail

The retail industry has struggled recently amid slowing in-store traffic, weak earnings, and inflated inventories. The hardest hit bricks-and-mortar retailers include Macy's , Men's Wearhouse , and Fossil Group , all of which are down double digits year to date. However, these retail stocks could also be the most rewarding picks for patient investors down the road. Three Motley Fool contributors explain below.

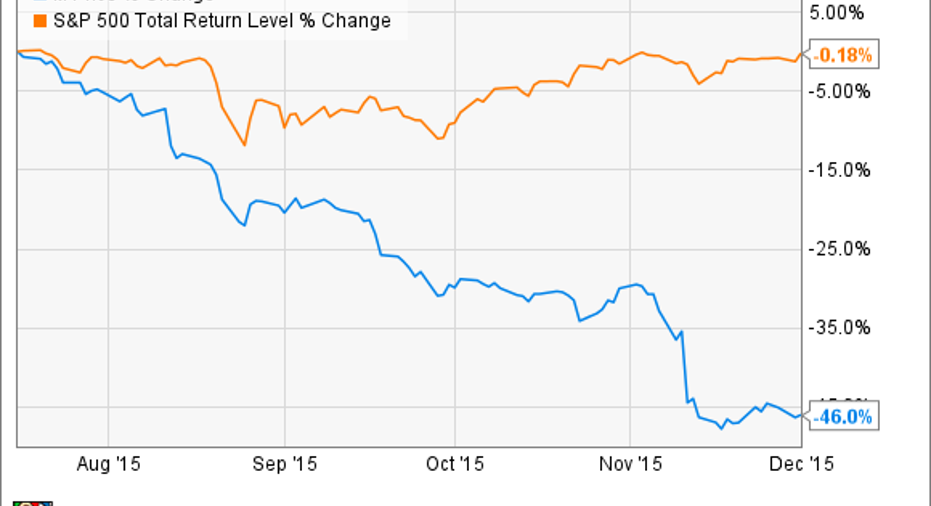

(Macy's):Macy'sstock has been crushed since this summer:

After achieving relatively strong business results since the end of the recession, the company has struggled with stagnating sales in 2015.

Macy's reported a sharp 4% decline in same-store sales in the third quarter, an acceleration from the 2% comps decline the first half of the year. Falling comps is a big concern in retail, especially when fashion is a big part of your brand, as it is for Macy's.

Earnings per share were down by nearly half, though when adjusting for one-time impairment charges related to planned store closings, earnings fell only about 9%.

But the market seems to be expecting Macy's short-term struggles to turn into a downward spiral.

Here's my take: Macy's is profitable and produces strong cash flows, and management is taking steps to make the business stronger, closing underperforming stores and focusing on growth in e-commerce and its "Backstage" outlet store concept, while expanding in China. It will take time for these initiatives to bear fruit, but the company is in a strong financial position and management can take the time to execute on its strategy deliberately.

With a price-to-earnings multiple of barely over 10 today, Mr. Market's expectations are very low. And while the bottom-line results could get worse before they turn around, Macy's is becoming a very intriguing turnaround play. I'll certainly be paying close attention.

Sean Williams (Men's Wearhouse): I believe if long-term shareholders are patient withMen's Wearhouse, they're going to like the way their portfolio looks.

Shareholders are currently in a world of hurt: Men's Wearhouse stock tumbled roughly 50% in November after the company announced disappointing preliminary third-quarter estimates and weaker-than-estimated fourth-quarter and full-year results. (Full results are scheduled to be reported this evening.) The weakness stems from its integration of Jos. A. Bank, a purchase it announced last year. Jos. A. Bank is known for its "buy one, get X free" type of sale events, and Men's Wearhouse no longer wanted to cheapen the brand, or its margins, with these sales. Men's Wearhouse first de-emphasized these sales, then wound up removing them altogether this year, crushing Jos. A. Bank's traffic and resulting in a colossally bad second-half of 2015.

Things may not look great here, but hope for a turnaround is far from lost. For now, Men's Wearhouse appears steadfast in its approach to refresh the Jos. A. Bank brand and offer a different sort of promotional strategy. This method didn't work too well forJ.C. Penney, and the initial results suggest it's not working well for Men's Wearhouse, either. But Men's Wearhouse is also healthfully profitable, and has the time to tinker with the Jos. A. Bank brand, which wasn't the case with Penney's.

Also, we should keep in mind that consumers think very short-term. If Men's Wearhouse does bring back Jos. A. Bank's signature promotions, its previous core customers would likely return. The apparel consumer generally gives a company multiple chances to right the ship, and has a short-term memory when things don't go their way.

Another way of looking at this is fundamentally. The last time Men's Wearhouse traded below $20 per share was in mid-2010. Men's Wearhouse's sales have practically doubled since then, its margins are nearly identical, its dividend is much higher, and its share count has been reduced via buybacks. I'd opine that It's an attractively beaten-down stock that has all the making of a rebound over the long term.

Tamara Walsh (Fossil): You may be crying yourself to sleep at night if you're a loyal shareholder of watch and accessories maker Fossil. Wall Street has pushed the stock down more than 65% so far this year. Shares currently trade around $38 apiece, or near the bottom of the stock's 52-week range. The retailer's stock lost more than a third of its value recently after reporting weaker-than-expected third-quarter results. Fossil also predicted sluggish sales for the 2015 holiday shopping season.

However, the growing popularity of smartwatches and wearable tech is perhaps investors' biggest concern for the traditional watch seller. Fossil's watch sales, for example, fell more than 17% during the third quarter. Yet while this certainly poses some challenges for Fossil, it also creates an opportunity for the retailer to capitalize on an increasingly lucrative new market.

Fossil is already making important strides to grab a piece of the $80 billion (and growing) wearables market. Last month, the company said it would acquire connected device company Misfit for $260 million. "With the acquisition of Misfit, Fossil Group will be positioned to win with the connected consumer," said Greg McKelvey, chief strategy and digital officer of Fossil Group. This will enable Fossil to add connected technology to its portfolio of brands, thereby expanding its addressable market beyond traditional watch buyers.

This proactive move on the part of Fossil's management could create revenue growth for the company in the years ahead. For this reason, I believe the double-digit sell-off in the stock is overblown, and that patient investors will be rewarded down the road.

The article 3 Turnaround Stocks to Watch in Retail originally appeared on Fool.com.

Jason Hall has no position in any stocks mentioned. Sean Williams has no position in any stocks mentioned. Tamara Rutter has no position in any stocks mentioned. The Motley Fool recommends Fossil. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2015 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.