3 Top Home Goods Stocks to Buy in 2017

Home goods retailers serve a huge, growing industry in the United States that last year accounted for $269 billion of revenue.

In a market that large, there's plenty of room for several big stock-market winners. Below, we'll look at why Big Lots (NYSE: BIG), Wayfair (NYSE: W), and Target (NYSE: TGT) stocks could each make attractive buy candidates for long-term investors, depending on your particular investing goals.

Image source: Getty Images.

Steady growth -- Big Lots

Big Lots operates in the massive, but highly competitive, discount end of the industry. Its closeout business model takes advantage of inefficiencies like bloated inventory and retail store closings to offer unbeatable prices, in exchange for a product offering that frequently changes.

Furniture is the company's single biggest product segment and Big Lots' prime market positioning in this niche helps generate solid profitability and sales growth. Comparable-store sales have been positive for 12 straight quarters, and Big Lots last year posted an uptick in profitability as it succeeded in passing on higher prices to customers even as comps improved by 1%.

Among the biggest risks to watch over the next few years is the growing threat from online shopping. Big Lots' focus on bulky furniture items has mostly protected it from this challenge so far, but eventually the company will need to establish a strong presence online to offset declining shopper traffic.

Disruption potential -- Wayfair

Online retailing specialist Wayfair represents a bold, yet risky, bet on e-commerce disrupting the home goods market. After all, the U.S. digital channel is forecast to grow at a 15% annual rate between now and 2025, compared to less than 3% for the traditional retailing segment. Wayfair, with its online catalog of over 8 million home products, stands to benefit significantly from that shift.

Its business model relies on a vast network of partners -- over 10,000 at last count -- that hold its inventory and help it fulfill orders. That asset-light setup allows Wayfair to focus its investments on optimizing around the e-commerce shopping experience while boosting its branding.

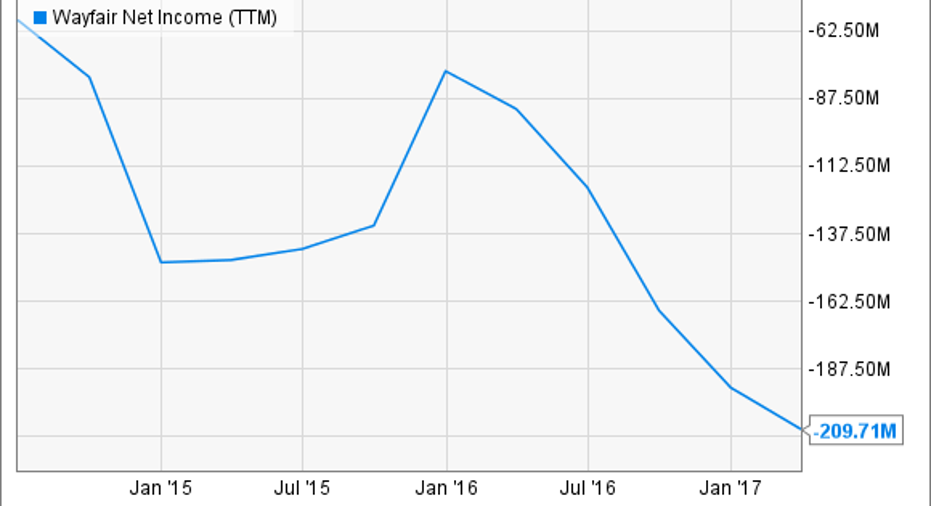

So far, the operations haven't delivered solid profitability. Expenses have far outstripped profits over the last three years, leading to consistently large net losses.

W Net Income (TTM) data by YCharts.

But that could change once the company shifts its focus away from attracting more customers toward maximizing profits. Wayfair aims to eventually reach adjusted profit margins of between 8% and 10%, compared to losses of between 3% and 5% since fiscal 2014.

A juicy dividend -- Target

More conservative investors might prefer Target. One of the leading retailers in the country, its business is groaning under the weight of spiking online competition and market-share gains by its biggest rival, Wal-Mart. Customer traffic fell 1% in the most recent fiscal year to reverse the prior year's 1% uptick. The physical retailing slump also bled into Target's 2017 fiscal year, so, despite a 22% jump in online orders, overall comps fell 1.3% last quarter.

This business has plenty going for it, though, including a dividend that's been growing for more than 25 consecutive years, yields over 4%, and is well covered by healthy operating cash flow.

As for the struggling operations, CEO Brian Cornell and his executive team are aiming to rely on Target's signature categories like home furnishings and apparel to help the company return to steady sales and profit growth.

However, investors buying shares today should understand that they're signing up for a bumpy ride -- at best. Customer traffic trends aren't likely to improve quickly, and profits are set to decline at least through the next year as Target cuts prices in a bid to better compete against its value-focused rivals both online and in physical stores.

10 stocks we like better than TargetWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Target wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017

Demitrios Kalogeropoulos has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Wayfair. The Motley Fool recommends Big Lots. The Motley Fool has a disclosure policy.