3 Things Investors Should Know About Genomic Health Stock

Investors who are intrigued by the promise of new healthcare technology to fight cancer will probably want to look at Genomic Health (NASDAQ: GHDX) stock. The provider of genomic-based diagnostic tests has set itself apart from other genomic companies with its Oncotype product line.

Is Genomic Health the kind of stock that could generate huge returns over the long run? Possibly. However, here are three things investors should know before buying Genomic Health.

Image source: Getty Images.

1. High volatility

If you only looked at Genomic Health's beta value of 0.68, you might think the stock wasn't too volatile. In theory, that beta value means that Genomic Health stock is considerably less volatile than the overall market. But is that really the case?

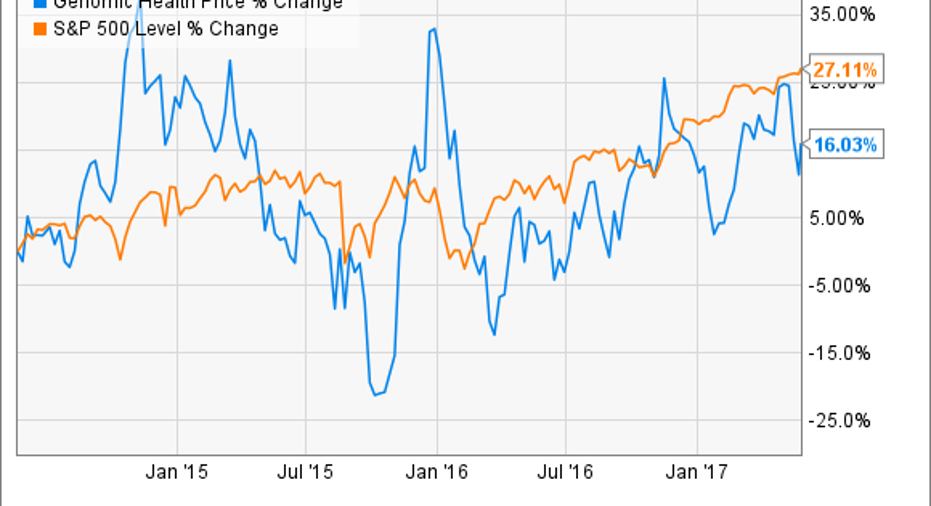

Beta values are typically calculated by comparing monthly prices of a stock against monthly prices of the S&P 500 Index. Different time periods can be used, but 36 months is common. Here's how Genomic Health stock's chart looks versus that of the S&P 500 Index.

Genomic Health stock had multiple wild swings during the period. The chart appears to show that it was a lot more volatile than the S&P 500 was. So why would Genomic Health have such a low beta value?

Perhaps the best explanation is that the monthly prices for the stock didn't have nearly as many gyrations as the above chart of daily prices reflects. Regardless, investors should be aware that Genomic Health stock is pretty volatile and be prepared for a potentially bumpy ride.

2. High valuation

Genomic Health's shares trade at nearly 93 times expected earnings. That's a sky-high forward earnings multiple. In February, I listed Genomic Health as one of the three most wildly overvalued stocks in healthcare. Here's the kicker: the company's forward earnings multiple is higher now than it was then.

The primary issue for Genomic Health is that it is spending a ton of money on sales and marketing. Its stock trades at only 3.18 times sales. That's actually a pretty good level. However, the company has been spending more on operations than it makes in revenue. The single biggest expense is sales and marketing.

While spending in other areas has gone down, sales and marketing costs are going up. This trend doesn't appear to be likely to change anytime soon. Genomic Health says that it expects sales and marketing expenses to increase because of itsefforts to spur adoption of and reimbursement for its products, expand its global commercial infrastructure, and grow its sales force.

3.Wide range of growth projections

High valuations can be acceptable to investors when a stock has tremendous growth prospects. Is that the case for Genomic Health? It depends on who you ask and how they define growth.

The company maintains that it will be able to grow adjusted EBITDA from around $10 million last year to over $100 million by 2020. If that impressive growth is achieved, Genomic Health's current valuation could be justified.However, the consensus among Wall Street analysts calls for average annual earnings growth of less than 6%.

One reason behind the big discrepancy in projections is the difference between adjusted EBITDA and earnings. The former is inflated by the addition of depreciation and stock-based compensation expenses. Genomic Health spent over $18 million last year on stock-based compensation and nearly $9 million on depreciation and amortization. That's a lot of money to leave out of the equation.

Why the stock could still be a buy

Despite all of this, Genomic Health could still be a stock for long-term investors. A sizable potential market exists for the company's products. For example, Genomic Health's Oncotype DX for breast cancer has a 55% U.S. market share and has penetrated only 10% of the potential international market. Its Oncotype DX for prostate cancer has penetrated 10% of the U.S. market.

The company should be able to secure reimbursement for its products in more European countries in the next year or so. In addition, Genomic Health's Oncotype SEQ liquid biopsy is especially promising.

I expect the financial results for Genomic Health will improve significantly in the coming years. Will the company grow enough to justify its current valuation? It remains to be seen. But for investors who aren't too risk-averse and are willing to hang on through ups and downs, Genomic Health stock could be one to consider.

10 stocks we like better than Genomic HealthWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Genomic Health wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017

Keith Speights has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Genomic Health. The Motley Fool has a disclosure policy.