3 Reasons to Love Caterpillar

Caterpillar shareholders received some good news when the company reported a better-than-expected fourth quarter. Although the heavy-equipment maker'ssales missed analyst predictions by $420 million, Caterpillar'sbottom line beat estimates by $0.04 per share. Management expects 2016 revenue to be $40 billion to $44 billion, and profit to be $4 per share when excluding restructuring costs, ahead of analyst estimates of$43.3 billion and $3.48 per share.

Caterpillar's strong guidance is welcome news for shareholders, who have seen the stock fall by almost 40% over the past six quarters as weak commodity prices and soft Chinese and Brazilian economies weigh on the company's results. Despite the stock's poor performance, there are several compelling reasons to believe that Caterpillar is a good buy-and-hold stock.

1.Caterpillar's dividend is secureCaterpillar pays a $0.77 dividend each quarter, which at current prices translates to a near 4.5% dividend yield. That's better than what Caterpillar's competitors, Joy Global and Deere & Company, offer, as Joy Global yields 0.3% and Deere & Company yields 2.96%. Moreover, unlike Joy Global, which cut its dividend to$0.01 from $0.20 in December due to deteriorating mining equipment demandgiven the low commodity prices, there isn't much chance of Caterpillar cutting its dividend unless economic conditions deteriorate further. Caterpillar expects to make $4 in earnings per share for 2016 and $3.50 in EPS when factoring in restructuring costs. The expected 2016 earnings more than cover Caterpillar's annual dividend of $3.08 per share.

Caterpillar's management is also committed to the dividend. They have said that maintaining the dividend is a high priority, and have shown that they are willing to do what it takes to support it. Caterpillar has laid off thousands of its workers over the past year in order to be competitive and cash flow positive in the weaker demand environment. Management has also cut back on stock buybacks to conserve more cash for the dividend. The company repurchased $2 billion of its shares in the first three quarters of 2015, but almost none in the fourth quarter.

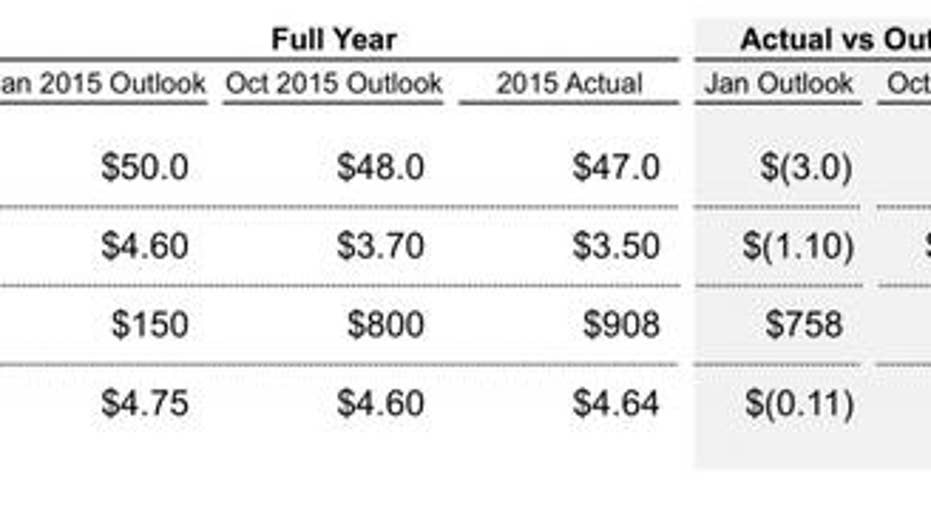

2. Management is controlling costs

IMAGE SOURCE: CATERPILLAR INVESTOR PRESENTATION.

Although its 2015 revenue was $3 billion lower than what management expected at the beginning of the year, Caterpillar'sprofit per share was just $0.11 per share short when excluding restructuring costs. The company's resilient bottom line was due to management cutting costs mercilessly. As a result, Caterpillar's expenses are expected to be $900 million lower than they were in 2015.

Management's focus on expenses is very important. Keeping costs competitive is necessary to prevent unneededdilution in bad times and keeps the dividend safe.

3. It's a qualitycompany that's gaining market shareDespite cutting costs, Caterpillar is still a resilient market leader with solid growth prospects. Having been around for 90 years, Caterpillar has survived previous sector busts, and has gained market share because of them. For 2015, Caterpillar gained market share for the fifth straight year in the machines sector and continued to make substantial investments in research and development and in digital capabilities to connect fleets and job sites. Caterpillar's investments will ensure that the company's profits will rebound quickly when commodity prices or emerging market conditions improve.

If global demand worsens,Caterpillar has adequate time to adjust because it has $6.5 billion in enterprise cash, and an "A" credit rating.The same can't be said for other competitors such as Joy Global, which doesn't have as much liquidity or credit.

Caterpillar is a great buy-and-holdCaterpillar is profitable, has good dividend coverage, and is making the necessary investments to do well when the global economy recovers. The company's management is also doing what it takes to preserve the balance sheet and dividend. Although global economic conditions could worsen before they get better, Caterpillar seems like a good buy-and-hold stock.

The article 3 Reasons to Love Caterpillar originally appeared on Fool.com.

Jay Yaohas no position in any stocks mentioned. The Motley Fool is short Deere & Company. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.