3 Reasons This Red Hot High-Yield Dividend Stock Is Still a Good Buy Today

Source: Brookfield Infrastructure Partners.

Wall Street is indeed a fickle mistress. Just a few months ago, crashing oil prices and growth worries over China had the markets in a tailspin and long-term income investors could scoop up amazing quality dividend names at great prices.

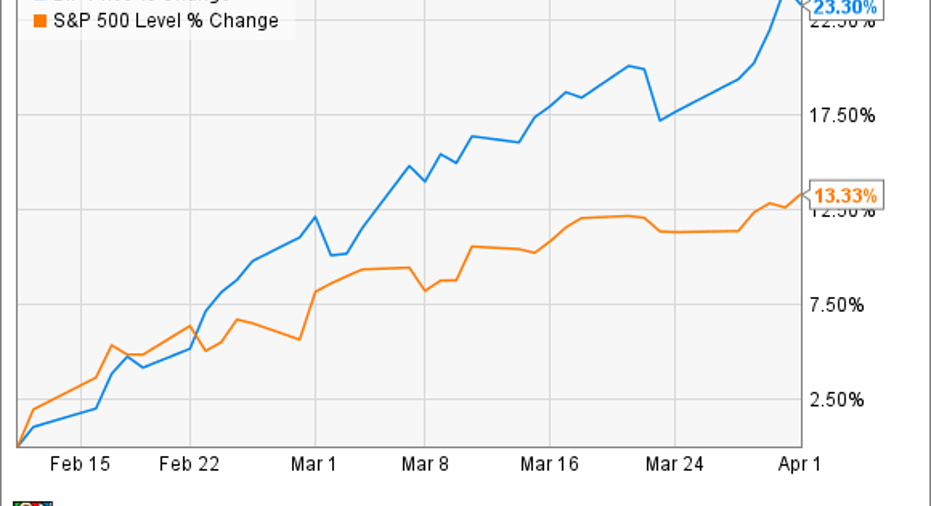

Yet today the market seems in full-time rally mode, and some high-yield stocks, such as Brookfield Infrastructure Partners (NYSE: BIP), have done even better in recent weeks, jumping almost 25% since the market's Feb. 11 low.

Yet as Warren Buffett famously said, "It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price." Brookfield Infrastructure Partners fits the bill of the great company selling at a fair price even after the recent rally, here's why.

Strong organic growth initiativesCFO Bahir Manios had this to say on the Q4 earnings call:

Whilethis diverse global utility is best known for fast growth through megadeals put together by its sponsor and general partner, Brookfield Asset Management ,its ability to also expand on most of its assets to continue growing cash flows is impressive.

More importantly to dividend investors, it can help Brookfield Infrastructure Partners hit its goal of annual distribution growth of 5%-9% in a more sustainable fashion.

By that I mean that in 2015 Brookfield generated $123 million in excess adjusted funds from operations, which is what funds the distribution.This 82% AFFO payout ratio means not just that the payout is secure but also that Brookfield Infrastructure can spend that excess cash on suchfurther growth initiatives.

Disciplined management never reaches for growthAccording to Manios, Brookfield Infrastructure has almost $3 billion in liquidity at the end of 2015, courtesy of raising $2 billion last year in debt and equity.

However, what I love about this LP is how management, which Brookfield Asset Management provides,is that it always focuses on maximizing its returns on investor capital. For example, its 2015 net ROIC (ROIC minus cost of capital)was 5.33%.

While that may not sound like much, in the utility industry that's quite impressive, especially compared with its much largerpeers.

- National Grid: 4.52%.

- Exelon: 4.34%.

- Dominion Resources: 2.75%.

More importantly, it means thatunitholderscan have confidence that Brookfield Infrastructure isn't lighting their cash on firevia "growth at any cost" deals that boost cash flow but destroy long-term investor wealth.

Case in point: Management recently dropped its effort to acquire a 25% stake in some Brazilian airport infrastructure and toll roads because it wasn't able to obtain an attractive enough price. With plenty of other "once-in-a-lifetime" opportunities available in the depressed Brazilian infrastructure market, Brookfield remains very careful with how it spends investor money.

Higher share price is better for long-term growthWhile Brookfield Infrastructure Partners may not be yielding 7.5% anymore as it was just a few months ago, its 5.5% distribution is still highly attractive.

More importantly for long-term investors is the that, given Brookfield'sbusiness model--it paysmost of itscash flow as distributions and funds highly profitabledeals with debt and equity -- Brookfield Infrastructure's much higher price is in the range for achieving total returns.

For example, at its yield of 4% to 6%, investors can earn rich current income while the LP can raise growth equity capital at low enough cost to make highly accretive acquisitions that will lead to better long-term payout growth. If the pricewas toolow, the LP may find it too expensive to tap the equity marketsjust when attractively pricedEuropean and Latin American infrastructure assets were available.

Risks to be aware ofWhile Brookfield Infrastructure's global assets mean its cash flows are highly diversified, it also exposes them to foreign commodity fluctuations. For example, in 2015 the strong U.S. dollar caused a $60 million, or 20%, decrease in earnings.

While Brookfield Infrastructure Partners has hedged 75% of its cash flows through 2017, investors need to realize that, should a strong U.S. economy trigger additional interest rate increases this year, the dollar could strengthen further. While currency fluctuations are normally short-term risks, given the low rate of global interest rates and the Federal Reserves' stated projections for longer-term US interest rates, it's possible that a stronger dollar could serve as a headwind to Brookfield Infrastructure's growth for several years to come.

Bottom lineEven though its unit price has soared to a 52-week high, Brookfield Infrastructure remains one of the best high-yield dividend growth stocks you can buy today.

With the backing and management team of Brookfield Asset Management behind it, as well as strong liquidity and a laser-like focus on disciplined spending of investor capital, income investors should consider it for a spot in their diversified dividend portfolios.

The article 3 Reasons This Red Hot High-Yield Dividend Stock Is Still a Good Buy Today originally appeared on Fool.com.

Adam Galas has no position in any stocks mentioned. The Motley Fool recommends Brookfield Infrastructure Partners, Dominion Resources, and National Grid. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.