3 Reasons Royal Dutch Shell's Stock Could Rise

Image Source: Royal Dutch Shell via flickr.com

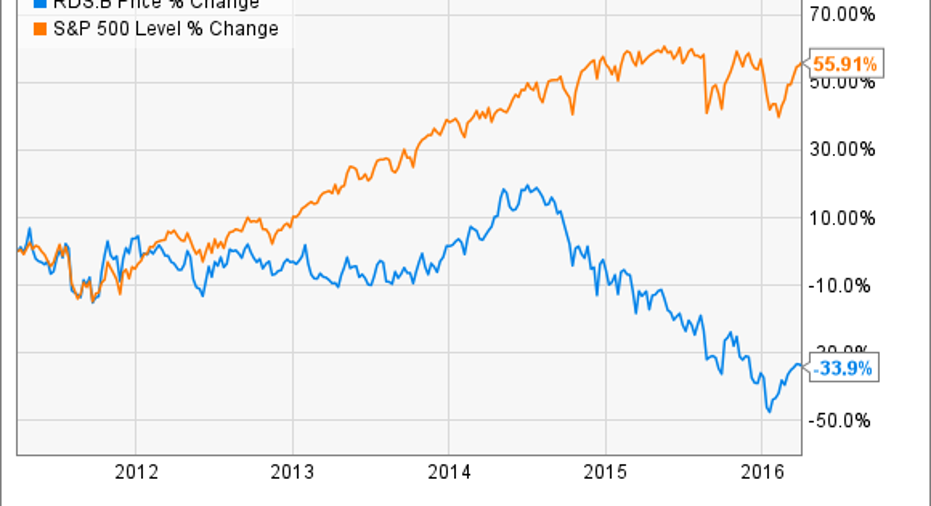

The past half decade has not been too kind to shares of Royal Dutch Shell . Even when oil was at $100 a barrel or more, troubles with overspending led to shares going pretty much nowhere. Once the oil price plunge hit a little less than two years ago, things got even worse.

Like so many other companies, the prospects of Shell's stock price is going to wax and wane with the price of oil. Beyond that, though, there are a few things that management is doing that could help boost its share price over the long term. Let's look at three catalysts that could help Shell put its shares back on track in the coming years.

Robust LNG demandFor the most part, integrated oil companies avoid being overly concentrated to a single aspect of the oil and gas industry. They all have similar percentages of upstream & downstream assets, and the same for a balance between oil and gas production. The theory is that by having a broad, balanced portfolio of assets, it helps to smooth out some of the volatility in the market.

That being said, Royal Dutch Shell is making a pretty outsized bet on the globalization of natural gas through LNG shipments. With BG Group into the fold now, Shell's LNG footprint is larger than the next two integrated oil companies combined

Image Source: Royal Dutch Shell investor presentation

We have started to see a bit of a decline in LNG prices, and that has led some companies to rethink some of their LNG investments a few years down the road. Ultimately, though, LNG is a strong business for integrated oil companies because it's mostly conducted with long term supply contracts that aren't influenced too much by the fluctuation of natural gas prices. If Shell can realize some strong demand across its LNG portfolio, it would likely provide a strong source of free cash flow that can be used to pay dividends and other shareholder friendly initiatives.

Strong cost savings from BG Group integrationRoyal Dutch Shell pretty has much no control of the price of the commodities which it sells, so the only real thing that the company can control is its costs and its capital allocation. This issue has come to the forefront for oil and gas producers as they try to handle the low price environment, but it's quite pertinent for Shell because it has just recently completed the $50 billion acquisition of BG Group.

According to Shell, it believes that it can realize pre-tax cost savings of $3.5 billion by 2018. To meet that sort of ambitious savings, it will involve lots of job cuts and consolidating operations in places were the company has large overlap like Brazil, Australia, Egypt, and North America.

Image Source: Royal Dutch Shell investor presentation

So there are plenty of opportunities to be more selective about capital spending and to reduce costs in overlapping regions. The real challenge now, though, is to actually execute on those cost cuts. Trying to reshape the corporate culture and operating procedures can be a daunting task, and the size of BG Group will make it that much more challenging in the first several months.

If management can indeed meet its stated goals for lower operational expenses and more targeted capital spending, then it should really help the company boost its returns on capital, something Shell has struggled with in recent years. A boost in returns could go a long way in earning Shell a higher valuation multiple and send its share price higher.

Making good on shareholder return programFor a long term shareholder, this is probably the most important catalyst for the company's stock in the coming years. In 2017, when management believes the BG integration will be mostly complete and oil prices were be in a better place, the company intends on buying back about $25 billion worth of the company's stock over a three year period. The company is waiting until 2017 to start the program because it can't cover today's capital spending and dividend payments with cash from operations. Management estimates that by 2017, all capital spending and dividend payments will be covered with cash, and some remaining from asset sales and excess cash flow can go into repurchases.

A large portion of that is to help recover the share dilution that took place following the BG acquisition, but if the combined companies were to lead to much higher overall earnings, then removing that many shares should go a long way in boosting per share profits.

So much of this shareholder return program is predicated on oil prices, though. The combined company and its estimated cost cutting is expected to bring the company's production break-even price from $70 per barrel to the low-to-mid $60 range. It's an improvement, but still quite a ways off from today's oil prices. If we don't see a decent rebound in oil prices between now and 2017, though, this major share repurchase program may need to be put on the back burner.

What a Fool believesI -- and no one, really -- can predict where Shell's stock will go in the next couple of months. With so many factors influencing oil prices, Shell's stock could go in any direction that oil prices go in the short term. Longer term, though, strong LNG demand, realizing the cost benefits from the BG merger, and making good on its shareholder return program would go a long way in boosting Shell's per share value. For investors, the thing to watch out for in the near term is any news or progress related to cost savings related to the Shell merger, if that goes off well, then it should help to set up that large buyback program.

The article 3 Reasons Royal Dutch Shell's Stock Could Rise originally appeared on Fool.com.

Tyler Crowe has no position in any stocks mentioned.You can follow him at Fool.comor on Twitter@TylerCroweFool.The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.