3 Reasons FireEye Will Bounce Back in 2016

Investors have shut the door on 2015. FireEye (NASDAQ: FEYE) investors, on the other hand, slammed it. The past year was not kind to the cyber security company as the stock dropped 34% for the year. At just under $21, FireEye is now trading just a smidge above its original $20 IPO price.

However, a new year is a time for new beginnings and optimism. Here are three reasons investors can open the door back up for FireEye stock in 2016.

Cyber security is here to stay3D printing, hover boards, and the Internet of Things are three emerging technologies that didn't quite live up to the hype. In 2016, the hype seems to be centered around drones and virtual reality. It's too early to see if any of these technologies will be a long-term winner but there is one technological trend that is not going anywhere: cyber security.

According to Juniper Research, cyber crime will cost businesses over $2 trillion by 2019, almost 4 times the cost of breaches in 2015. Juniper also estimates the average cost of a data breach to exceed $150 million.

The cost of a data breach is significant. Retail giant Target (NYSE: TGT) has incurred $290 million in expenses since hackers made their way into Target's network in 2013. The costs may go higher as the company expects a class action suit from financial institutions and shareholders. It is also facing ongoing investigations by the State Attorney General and Federal Trade Commission.

Often the financial costs associated with a breach are just the beginning. Once a breach is made public, a company's brand may never recover from the reputational hit it incurs. Businesses are beginning to take notice. The Global State of Information Security Survey by PWC reveals that respondents increased their cyber security budgets by 24% in 2015. Furthermore, 54% of respondents have a Chief Security Officer and 53% of businesses have implemented an employee training program revolved around cyber security. Given the damage a data breach can have on a business, I expect these numbers to increase beyond 2016.

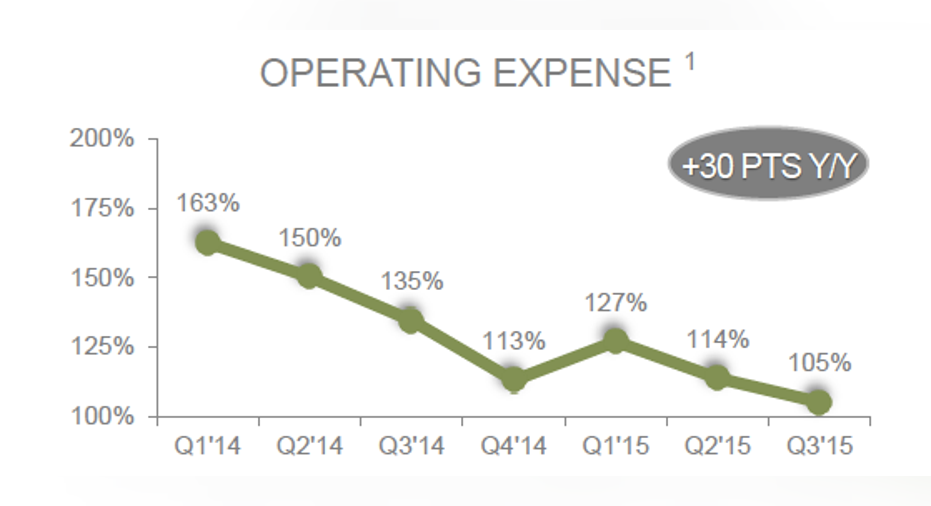

Profitability is on the horizonFireEye is currently not profitable-plain and simple. However, as the company continues to grow sales faster than costs, it's just a matter of time:

1. Non-GAAP. Source: FireEye.

Additionally, FireEye ended the third quarterwith $28 million in positive operating cash flow for the year. This is a significant milestone as Wall Street and FireEye management were not expecting the company to stop bleeding money for another two to four more years.

The price is rightThe past year has been a roller coaster ride for cyber security stocks. HACK (NYSEMKT: HACK), a cyber-security ETF, began the year trading just under $27 increased 31% in just 6 months. However, it ended 2015 essentially flat at $26. FireEye was even more volatile, increasing 74% from the beginning of the year to its all-time high. However, the stock ended the year down a total of 34%.

The clouds may be parting, however and the recent pessimism in FireEye stock may have created an opportunity for investors. Not only is FireEye trading well below its peers, it is trading below the entire software industry, which according to Capital IQ, boasts a P/S ratio of 6.7.

|

Company |

P/S Ratio |

|---|---|

|

FireEye |

5.6 |

|

Check Point |

9.5 |

|

Cyberark |

9.6 |

|

Palo Alto Networks |

14.4 |

|

Splunk |

12.5 |

Source: Capital IQ.

Although 2016 should be a bounce-back year, it is not going to be without difficulties. With the cyber security industry growing as rapidly as it is, competition is going to be fierce. However, the market is large enough that there is room for more than one winner. There will be growing pains, but in the new year, I expect FireEye to be one of those winners.

The article 3 Reasons FireEye Will Bounce Back in 2016 originally appeared on Fool.com.

Palbir Nijjar owns shares of FireEye. The Motley Fool owns shares of and recommends Check Point Software Technologies, FireEye, and Splunk. The Motley Fool recommends CyberArk Software and Palo Alto Networks. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.