3 Intriguing Growth Stocks Long-Term Investors Can Buy

Image source: Getty Images.

Growth stocks offer plenty of reasons for investors to buy them, but figuring out which growth stocks are best to add to portfolios can be tricky: Focus too much on stocks that are growing their top line because they're sacrificing profitability, and you might expose yourself to too much risk.

With that in mind, I hunted for companies that are rewarding investors with both top- and bottom-line growth, and discovered these three, each of which I think has catalysts that could reward long-term investors: Adidas (NASDAQOTH: ADDYY), Visa Inc. (NYSE: V), and Align Technology, Inc. (NASDAQ: ALGN).

Read on to see if they might be right for your portfolio.

Back on the right foot

Adidasis one of the most intriguing consumer goods stories of 2016. It was once the globe's biggest athletic-apparel company, but over the past decades it's fallen behind global Goliath Nike and upstart Under Armour.

Lately, however, it's been regaining some of its former glory. Thanks to new sponsors, sales of the company's footwear have taken off. Last quarter,Adidas' sales improved21% year over year on a constant currency basis to 4.4 billion euros ($4.9 billion). Sales growth was widespread with China, Western Europe, and North America growing 30%, 26%, and 31% versus a year ago, respectively.

That performance has Adidas' management pegging high-teens sales growth for the full year, up from 10% growth in 2015:

ADDYY Revenue (TTM) data by YCharts.

The company's bottom-line growth is also noteworthy. Last quarter, operating margin improved 3.4% to 9.4% and operating profit surged 77% to 414 million euros ($455 million). Diluted earnings per share are up 65% in the first six months of the year to 3.13 euros ($3.44).

Undeniably, the athletic apparel market is cutthroat, but catalysts are coming that could allow the company to drop even more money to its bottom line. A CEO with a penchant for divesting slow-growing, low-margin businesses took over the reins last month, and since Adidas' costs as a percentage of sales are lower than competitors, there appears to be room for profit-boosting changes.

Overall, Adidas' high-profile sponsorship wins, including the cementing of a long-term deal with Kanye West and the launch of a Kanye West product line, demonstrates Adidas is ready to compete again. And that could make this company's stock a savvy addition to growth portfolios.

Capitalizing on credit

Visa Inc.profits from credit transaction volumes, and a steady and continuing shift from cash to credit purchases offers plenty of tailwinds that aren't showing any signs of easing.

Over the past 10 years, Visa's trailing 12-month sales have increased from around $3 billion to about $15 billion, and last quarter, Visa's payment volume increased 10%to $1.3 trillion and its revenue improved 19% to $4.3 billion, including its acquisition of VisaEurope. The performance brought the company's fiscal full-year revenue to$15.1 billion, an increase of 9% from last fiscal year. Visa's profit also increased: In fiscal Q4, adjusted net income was$1.9 billion or $0.78 per share, and adjusted full-year 2016 net income was $6.9 billion or $2.84 per share, up 8% from last year.

Management believes that this coming fiscal year will be similarly successful for Visa. The company is guiding investors fornet revenue growth of between 16% and 18%, including a 1% to 1.5% drag from foreign currency conversion, and they think adjusted EPS will grow by mid-teens percentages too. Those predictions suggest that investor enthusiasm for Visa could continue.

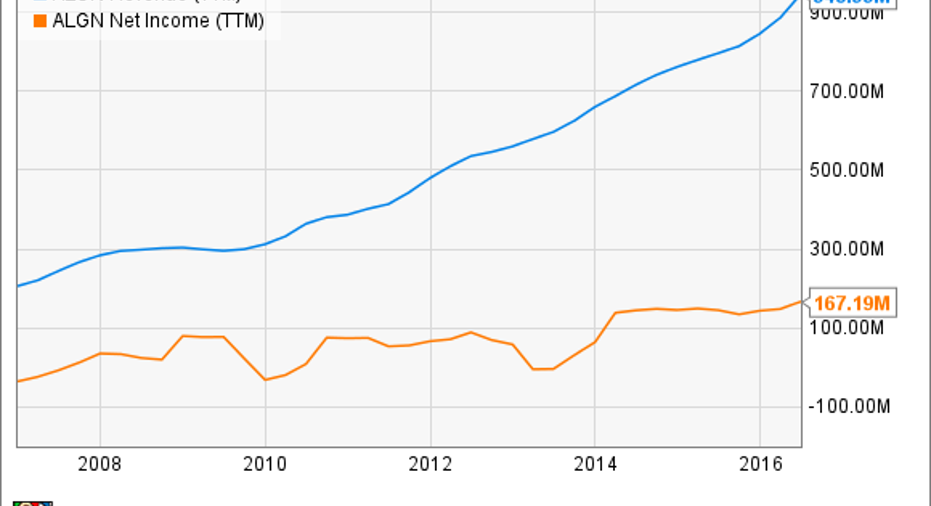

Profit from "pearly whites"

Align Technology'sInvisalign teeth aligners are already reshaping how orthodontists and dentists straighten patients' teeth, but with market share of only 7% and new products that could expand its addressable market to as many as 10 million people, the upside could be tremendous.

Rising demand for Invisalign resulted in second-quarter sales and profit jumping 29% to $269 million and 59% to $0.62 per share, respectively, and over the past 10 years, Align Technology's trailing 12-month sales have more than tripled:

ALGN Revenue (TTM) data by YCharts

Management believes Invisalign's current addressable market totals 5 million patients. However, advances that are improving Invisalign are making it an option for more patients, and that has management thinking that its addressable market could grow to 10 million over time.

Image source: Align Technology.

BecauseInvisalign isn't as noticeable as metal braces, it can be less expensive than metal braces, and it can be used in increasingly complex situations, there's reason to think that this company is in the early innings of changing a big global market.In Q2, North American andinternational sales were up 6% and 20% quarter over quarter, respectively.

If Align Technology makes inroads with general dentists, and next-generation Invisalign lives up to its billing, then I think double-digit top- and bottom-line growth can continue. If I'm right, then owning this growth stock could pay off handsomely.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Todd Campbell owns shares of, and The Motley Fool owns shares of and recommends,Under Armour (A Shares).Todd owns E.B. Capital Markets, LLC. E.B. Capital's clients may have positions in the companies mentioned.Like this article? Follow him onTwitter where he goes by the handle@ebcapitalto see more articles like this.

The Motley Fool also owns shares of and recommends Nike and Visa. The Motley Fool recommends Align Technology.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.