3 Growth Stocks to Buy in October

Image source: Getty images.

With the markets trading near all-time highs, it's getting harder and harder to find growth stocks that are tradingat an attractive price. However, our Foolish contributors are always up for a challenge, so we asked three of them to scour the markets and highlight a growth stock that they think is a great buy right now. Read on to see which companies they selected and why.

Clearly visible growth on the horizon

Matt DiLallo: Most growth stocks only offers investors the promise of future growth based on projections. Midstream MLP Phillips 66 Partners (NYSE: PSXP), on the other hand, is all but guaranteed to grow due to its pipeline of projects and drop-down acquisitions from parent company Phillips 66 (NYSE: PSX). Those initiatives are expected to fuel 30% compound annual growth in Phillips 66 Partners' distribution, which should drive similarly robust growth in its unit price.

Driving this growth is Phillips 66's forecast that its namesake MLP will grow its underlying earnings from a run rate of $400 million up to $1.1 billion by 2018. One factor driving that growth is the MLP's $300 million organic growth backlog, which consists of three pipelines that are expected to be in service by the end of next year.

In addition to that, Phillips 66 owns several midstream assets that currently generate $600 million in earnings and that it can drop down to its MLP over the next few years. Further, Phillips 66 is investing in several organic midstream growth projects on its own dime, which it could eventually sell to its MLP.

These drop-down transactions are needle-moving for Phillips 66 Partners. For example, the partnership recently paid $775 million to acquire from Phillips 66 three assets that are expected to generate $90 million in earnings going forward. As a result of that deal, CEO Greg Garland said the company "remain[s] on track to deliver our stated five-year compound annual distribution growth target of 30% through the end of 2018."

Bottom line: Investors who are looking for rapid growth but want more than just promises should consider the certain growth that Phillips 66 Partners has coming.

Left out of the rally

Brian Feroldi:Alexion Pharmaceuticals (NASDAQ: ALXN), which focuses on rare diseases, is a high-growth stock that continues to fall, even as the market roars higher, which makes right now a great time to consider joining me as a shareholder.Alexion has been putting up double-digit revenue and profit growth for years thanks to its blockbuster drug Soliris, a treatment for two ultra-rare diseases called PNH and aHUS.More recently, Alexion has diversified its product portfolio with the launch of two new enzyme-replacement therapies called Strensiq and Kanuma.

Sales of these drugs are growing rapidly and should eclipse $200 million this year. Add in the $2.8 billion that Soliris is expected to pull in, and Alexion is projecting companywide sales to grow by an impressive 18% this year.

Yet despite the strong growth forecast, shares of Alexion have actually declined by more than 35% since the start of the year. What gives?

Image source: Getty images.

The answer can be traced to disappointing clinical results from the company's late-stage REGAIN study, released in June. The trial was testing Soliris as a potential treatment for refractory generalized myasthenia gravis (gMC). Positive results could have opened up a whole new group of patients for the drug.Unfortunately, the REGAIN study failed to show that using Soliris led to a statistically significant change in clinical outcomes. That caused traders to bail.

While the news wasn't good, I think the markets have overreacted. In the REGAIN trial, Soliris barely missed proving statistical significance on its primary endpoint, and it demonstrated statistical significance on three of its secondary endpoints. That has ledFiercePharmato report that some physicians may still opt to use Soliris off-label for this disease because there are no real alternatives. Thus Soliris could still see growth from this indication, even if it fails to win regulatory approval.

Market watchers are still projecting that Alexion will grow its bottom line by more than 18% annually over the next five years. With shares now trading for about 26 times forward earnings, I think right now is a great time to consider getting in.

Acquisitions created a monster!

Daniel Miller: XPO Logistics, Inc. (NYSE: XPO), a global transportation and logistics company, has been a wild growth story over the past half-decade. It put typical acquisition strategies to shame as it gobbled up companies in multiple spaces. It now ranks as the second-largest global provider of contract logistics, the second-largest less-than-truckload (LTL) provider in North America, the second-largest global freight brokerage firm, the third-largest intermodal provider in North America, and the No. 1 last-mile logistics provider for heavy goods in North America.

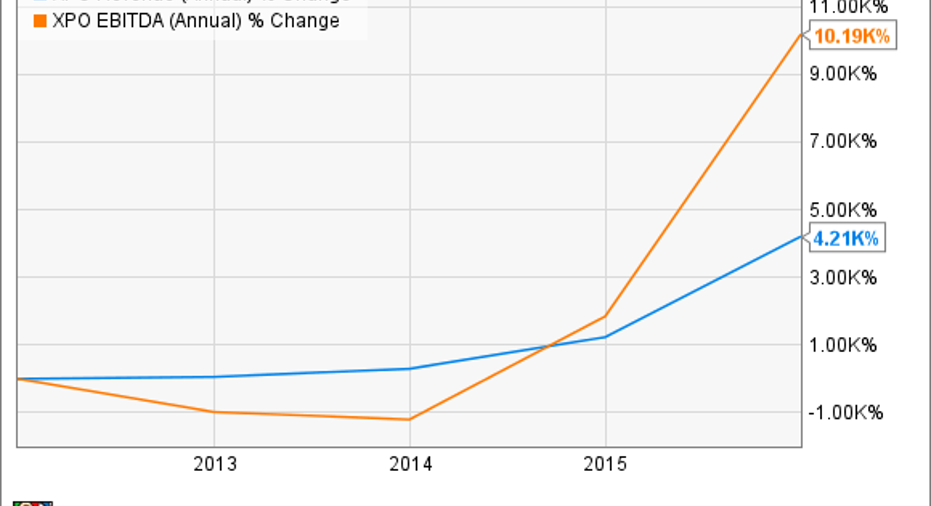

Just look at what its ambitious acquisition strategy has done for its top and bottom lines:

XPO Revenue (Annual) data by YCharts.

One metric that mirrors its top-line growth is its long-term debt, as XPO leveraged its balance sheet to acquire these companies. That's why, at least for now, management is hitting the pause button on its acquisition spree and focusing on generating strong synergies across the board -- something that should beef up the bottom line for investors.

As XPO Logistics operates in multiple sectors ranging from contract logistics and truck brokerage to North American truckloads, 77 of XPO's top 100 customers use two or more service lines. This, in my opinion, suggests that while XPO is taking a break from acquisitions, it can do a huge amount of cross-selling to its customers. That, in combination with cost synergies from recent acquisitions, should spell strong bottom-line growth over the next few years.

Speaking of cost synergies, XPO's chief transformation officer, Ramon Genemaras, has a great track record: He led $1 billion in cost cuts at General Electric, Tyco, and Johnson Controls. XPO management believes the company can achieve two full percentage points of margin improvement in the next 30 months.

XPO Logistics' acquisitions have made it a phenomenal growth story. While they're being put on hold temporarily to generate some juicy cost synergies, reduce debt, and take advantage of cross-selling opportunities, XPO's growth story is far from over.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Brian Feroldi owns shares of Alexion Pharmaceuticals.Like this article? Follow him onTwitter where he goes by the handle@Longtermmindsetor connect with him on LinkedIn to see more articles like this.Daniel Miller has no position in any stocks mentioned. Matt DiLallo owns shares of Phillips 66. The Motley Fool owns shares of General Electric and Johnson Controls. The Motley Fool is short Johnson Controls. The Motley Fool recommends XPO Logistics. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.