3 Growth Stocks for May

As a growth investor at heart, I would argue that there's no bad time to look into high-growth investment opportunities. The top tickers on the table do keep changing, though, so we asked three Motley Fool contributors to share some of their best growth stock ideas for this moment in time.

Read on to see why they pickedAllstate(NYSE: ALL),EPAM Systems(NYSE: EPAM), andUniversal Display(NASDAQ: OLED).

Image source: Getty Images.

You're in good hands withthis potential investment

Chuck Saletta (Allstate): It may be surprising to consider a more than 80-year-old insurance titana growth story, but Allstate just might be able to convince you it's possible. Despite a market capitalization of around $30 billion and over $2.2 billion in trailing-12-month earnings, Allstate is expected to grow its earnings at a very solid clip, near 15.5% annualized over the next five years.

With a backwards-looking price-to-earnings ratio below 15 and a forward-looking one of around 12 times its expected earnings,Allstate is trading at a reasonable price for that anticipated growth. Add to that a dividend of $1.36 per share per year -- for a modest yield of around 1.6%-- and Allstate's shares pay better than a typical 3-year Treasury Bondwhile providing that potential growth for investors.

Of course, just because Allstate looks like it's trading at a reasonable price for its potential growth doesn't necessarily mean the future will turn out in line with those expectations. Allstate was forced to cut its dividend by more than half during last decade's financial crisis, illustrating the risks associated with a competitive insurance marketplace. Growth and profits may appear real and strong -- until companies find themselves overextended when an insured or financial risk exceeds their expectations.

For instance, Allstate's combined ratio has exceeded 100% in the not-too-distant past, meaning it has previously lost money on its insurance operations. Unfortunately, the nature of insurance means that type of loss might very well happen again. Still, what matters is whether the company's balance sheet is strong enough to withstand those periods of insurance losses. With over $3 billion in cash and a debt-to-equity ratio of around 0.3,Allstate looks capable of handling a strong financial storm.

Despite the risks driven by its industry, Allstate looks like it has the rare combination of decent growth prospects and reasonable value to make it worth consideration as an investment.

Universal Display's growth story has only just begun

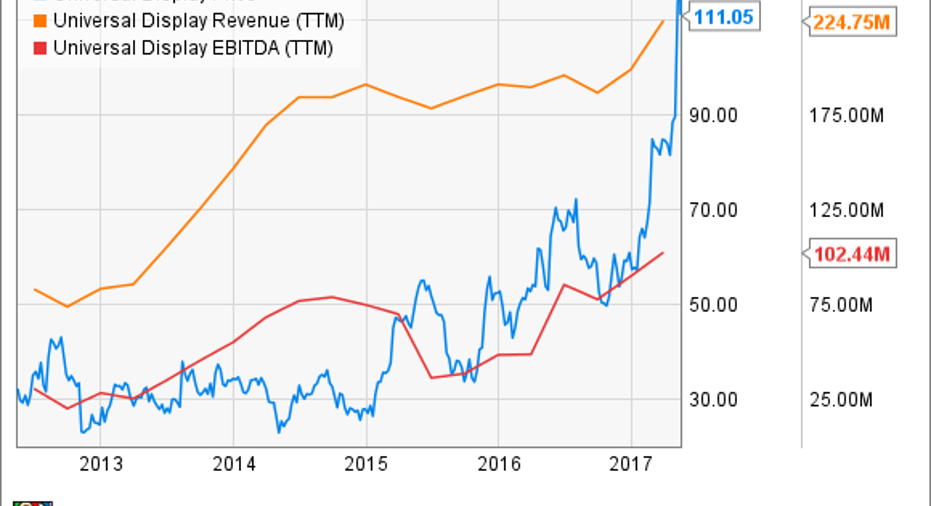

Anders Bylund (Universal Display): After a few years of relatively stagnant revenue and profit growth, Universal Display has kicked its growth engines into high gear again. Share prices already followed suit, but the stock still has a long way to go before running out of long-term rocket fuel.

The OLED lighting and display technology researcher has seen its share price double in 2017, punctuated by spikes after two fantastic earnings reports. The first-quarter update in early May was particularly poignant, since it included firm and positive revenue guidance for the rest of 2017. Major customers are investing billions in their OLED manufacturing lines, driving the technology deeper into the mainstream of smartphone, tablet, television, and lighting panel products.

According to comments by Universal Display CEO Steve Abramson, Samsung (NASDAQOTH: SSNLF) is pouring $9 billion into building OLED production facilities this year. LG Display (NYSE: LPL) expects more than half of its 2020 revenues to come from OLED panels. The OLED TV market is expected to grow sixfold in the next four years, and the lighting panel market is only just getting started.

Samsung and LG Display expect to reap returns on their OLED production investments, and Universal Display receives a combination of royalty payments and direct OLED material orders for every device that leaves their factories. This stock has skyrocketed in 2017, but there are acres of high-growth runway straight ahead.

A nice play on the IT outsourcing trend

Brian Feroldi(EPAM Systems): No two companies are exactly alike, which is why it is common for businesses to create their own custom software to run their day-to-day operations. The only problem is that creating that software in-house can be difficult, which is why many companies choose to outsource the work.

EPAM Systems is a company that more and more companies are turning to when they need help. The reason is that EPAM employs a vast worldwide network of designers, architects, software engineers, and consultants that it can quickly call on to get a project off the ground.

One great attribute of the IT outsourcing business is that clients are in constant need of help, and their needs are always changing. Those factors help to keep EPAM busy with new work once it lands a client. In fact, EPAM's business is so predictable that the company has about 80% to 90% of its revenue booked before any given year begins.

The company's recent results continue to show that its services remain in demand. Revenue grew 23% to $325 million, while non-GAAP net income jumped 15%. Meanwhile, the company's small army of "delivery professionals" grew 15% to nearly 20,000. The hiring boost positions the company well to take on more work, which is why management expects revenue to jump "at least" 21% for all of 2017.

Despite the company's strong growth projects, the company's stock is trading for less than 20 times next year's earnings estimates. I'd argue that's a fair price for a high-quality growth business, which is why I think EPAM Systems is a great stock for growth investors to buy right now.

10 stocks we like better than Universal DisplayWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Universal Display wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017.

Anders Bylund owns shares of Universal Display. Brian Feroldialso owns shares of Universal Display. Chuck Saletta has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Universal Display. The Motley Fool recommends EPAM Systems. The Motley Fool has a disclosure policy.