3 Great Reasons to Buy American Water Works Stock

Image source: Getty Images.

American Water Works(NYSE: AWK)stock has quenched investors' desire for market-beating returns over the long term.

Since going public in April 2008, the largest investor-owned water and wastewater utility in the U.S. has returned 363% through Sept. 29, leaving high and dry the broader market's 87.5% return. American States Water (NYSE: AWR), the industry's second-best performer over this period, has returned 172%, while the industry's second-largest player operating in the U.S. by market cap, Aqua America (NYSE: WTR), has returned 170%.

American Water, like most water utility stocks, has had a big run-up in price since mid-2015, driving its valuation to a high level. So investors should be aware that it could pull back over the median term. However, here are three top reasons American Water makes an attractive long-term investment.

1. It's in the right business

Fresh water is the most essential product that we humans need to live that isn't free. Moreover, the supply demand equation favors water stocks:

- Fresh water supply is limited and could shrink because the Earth has been in a long-term warming trend.

- Demand should grow because the world population is increasing and more people in emerging markets are moving into the middle class.

While there are various ways to invest in water, water utilities are the surest bets because their regulated businesses are monopolies. Additionally, most of them pay a decent dividend. (American Water's dividend is currently yielding 2%.)

2. Its size and geographic diversification provide its regulated business with a competitive advantage

American Water sports a considerable competitive advantage over its peers in its core regulated business -- which accounts for more than 90% of its total net income -- stemming from its larger size and greater geographic diversification.

The company has a market cap of $13.1 billion -- more than twice the $5.3 billion market cap of Aqua America, the second-largest industry player in the U.S. It generated $3.25 billion in revenue over the trailing 12 months, which is four times as much as Aqua America pulled in. American Water provides services to approximately 15 million people in 47 U.S. states and one Canadian province, and operates as a regulated utility in 16 of these states. The second most geographically diversified company, Aqua America, has regulated operations in just eight states.

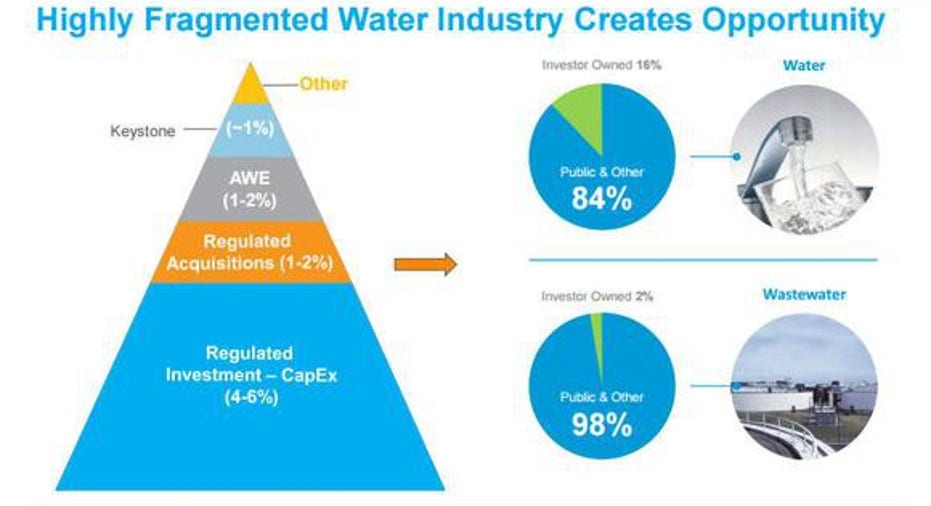

American Water's industry-leading size provides it with more resources to grow through acquisitions -- and there's much acquisition potential because the industry is very fragmented in the U.S. (as the chart below shows). Its geographic diversification means it can often expand near its existing operations without adding full new workforces. Moreover, this diversification makes it less vulnerable to regional-specific challenges, such as droughts. American States Water has been struggling recently because its entire regulated business is in California, much of which is in the fifth year of a severe drought.

The highly fragmented industry is one factor that should help American Water achieve its goal of a 7% to 10% earnings per share compounded annual growth rate from 2016 to 2020 (anchored by adjusted 2014 EPS). Image source: American Water.

3. Its market-based segment and Keystone subsidiary provide it with additional growth potential

American Water's market-based business, whichaccounted for 8.4% of its segment earnings per share in the second quarter of 2016, primarily builds, operates, and maintains water systems for military bases in the U.S. While the company must bid to win these long-term contracts, it still gets to set its own rates, which provides it the potential for higher profit margins.

Keystone Clearwater Solutions is also a market-based business, but operates as a subsidiary. American Waterentered the "fracking" water business in mid-2015 when it acquired Keystone, which supplies water and related services to natural gas exploration and production companies in the Marcellus and Utica shale regions of the Appalachian Basin. This acquisition was feasible because American Water has regulated operations in Pennsylvania and West Virginia.

It seems likely that American Water was able to pick up Keystone at a good price given the timing of the buy -- about a year after the huge downturn in the energy markets started. While the market for fracking water is still depressed, natural gas companies are picking up their drilling activities due to the rebounding price of natural gas. American Water's CEO Susan Story said on the last earnings call that the company is optimistic about Keystone's prospects once the recovery in the natural gas market makes further progress. Keystone is expected to have a neutral effect on earnings in 2016.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Beth McKenna has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.