3 Fast Facts That Can Help You Decide When to Claim Social Security

Image source: Flickr user Pug50.

Millions of Americans are approaching retirement, and one of the most important financial decisions retirees will make is when to begin receiving their Social Security benefits. Chose to receive benefits early, and you could leave tens of thousands of dollars on the table. Wait to claim Social Security until you're older, and you might end up with a bigger check that you'll be less able to enjoy because of failing health.

Although an individual's decision on when to begin receiving Social Security depends a great deal on their own personal situation, here are three Social Security facts that may help you make your choice.

Image source: Flickr user 401Kcalculator.

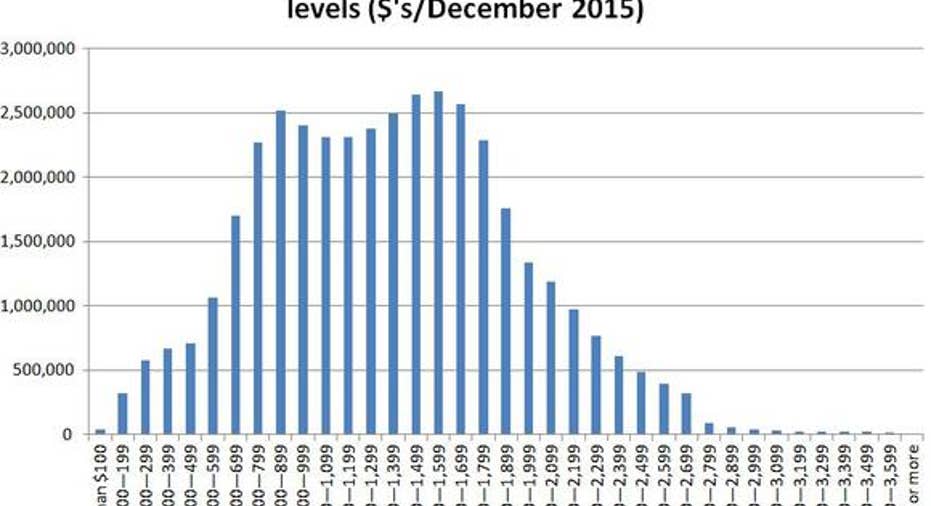

No. 1: Average Social Security CheckSocial Security is designed to supplement income in retirement, not replace all of your pre-retirement income. Therefore, retired workers typically collect about 40% of their pre-retirement income in Social Security benefits. However, as the following chart shows, the amount people receive can vary widely because Social Security benefits are based on a recipient's highest 35 years of income.

Despite the fact that your benefit could be vastly different than the averages, it may be helpful to know that the typical retired worker who collects Social Security received $1,345.49 in March. Add that to the average $695.02 paid out in spousal benefits, and you find that the average couple is collecting $2,040.54 in monthly benefits this year.

That's not a king's ransom, but depending on whether or not you've paid off your mortgage or have other sources of retirement income, it may be enough to support you in retirement. In order to estimate more precisely the benefit you can receive in retirement, you can use this handy calculator, or register and log into your account on the Social Security website.

Image source: Flickr user Garry Knight.

No. 2: Delayed retirement creditsThe majority of people receiving Social Security chose to do so earlier than their full retirement age, or the age at which they can collect 100% of their retirement benefits. Collecting early reduces your benefit by up to 30% if you were born after 1960 and opt into the program at age 62.

However, waiting to take Social Security until later than your full retirement age can pay off with a significantly bigger monthly check.

For example, a person born after 1943 will receive an 8% annual increase to their full benefit until age 70. Thus, a person born in 1960 with a full retirement age of 67 would receive a payment equal to 124% of their full retirement age benefit by waiting. That's a pretty big incentive to hold off on claiming Social Security, but depending on your financial situation, delaying may simply not be an option.

Image source: Flickr user Michael Dougherty.

No. 3: Life expectancy statisticsWhile it's true the Social Security Administration estimates that the average life expectancy of an American man and woman is 83 years and 86 years, respectively, many people pass away before or after those ages. For example, Vanguard calculates that the average man who is age 65 has a 41% chance of living to age 85, and the average woman age 65 has a 53% chance of reaching her mid-80s.

Although many people in their 60s have yet to suffer significant illness or injury, the median age at which a person is diagnosed with cancer is roughly 67.According to the National Institutes of Health, nearly 40% of men and women will be diagnosed with cancer in their lifetime. Similarly, the median age of a man or woman who suffers a heart attack is 66 and 70, respectively. Therefore, because it's considerably more common to face a life-changing diagnosis in your late 60s than it is in your early 60s, considerable thought needs to be put into evaluating your health before choosing to wait until 70 to take Social Security.

Tying it togetherThere's no magic number at which the typical American is best off claiming Social Security. The program is designed to pay out the same amount of money over an average person's lifetime regardless of when they file for benefits. Nevertheless, averages can be misleading, and therefore, decisions should be tied to both your budget and an honest assessment of life expectancy.

The article 3 Fast Facts That Can Help You Decide When to Claim Social Security originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.