3 Energy Stocks to Buy with Dividend Yields Above 5%

Image source: Getty Images

If you are looking for companies that have dividend yields north of 5%, then you'll need to travel into the territory of companies that have questionable payouts or less-than-certain futures. Fortunately, some companies with such high yields are less vulnerable than others. Three that stand out today are Enterprise Products Partners (NYSE: EPD), Holly Energy Partners (NYSE: HEP), and Eni (NYSE: E). Here's a quick rundown as to why each of them should be able to keep its high yield payout going for some time.

Close to dividend aristocrat status

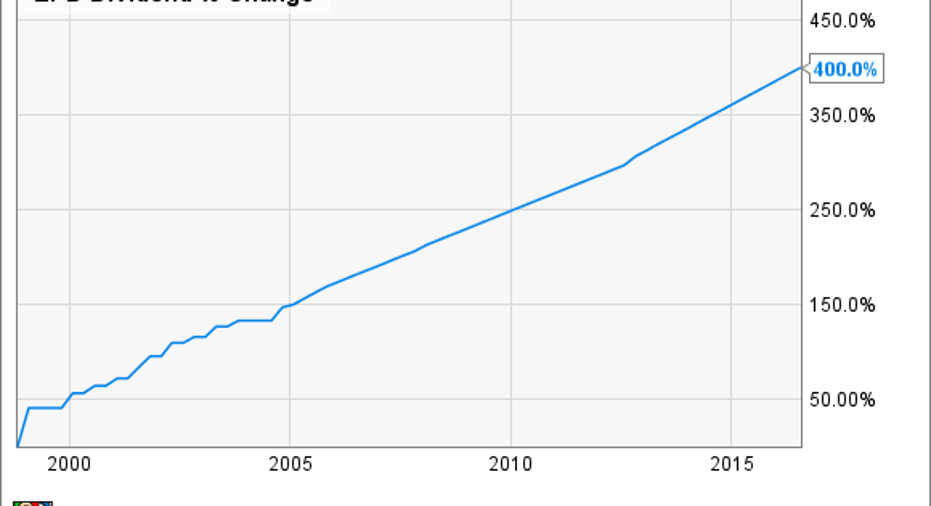

You will be hard pressed to find an investment that combines high yield with payout security as well as Enterprise Products Partners. The company's distribution yield now stands at 5.9%, but it's based on a payout that has risen every year since the company's IPO back in 1998. If it keeps that pattern going, it will become a dividend aristocrat in 2023.

EPD Dividend data by YCharts

Based on its business model,Enterprise should have no difficulty getting there. More than 85% of the company's gross profits come from fee-based services it provides involving its pipeline and infrastructure network, shielding it from much of the commodity price pain that has afflicted so many other energy companies. The company's strong balance sheet and payout policy have kept its finances much healthier than many of its peers.

For the company to actually grow, though, it will need to a produce suite of new projects that can deliver more cash to the coffers. Today, that doesn't appear to be a problem: Enterprise currently has $6.5 billion in new projects under construction, and expects $1.2 billion worth of them to come online by the end of 2016. This robust construction plan should be enough to see it through at least the end of the decade, and should put it on track to achieve that vaunted dividend aristocrat status.

Small company, big payout

Even though Holly Energy Partners is one-thirtieth the size of Enterprise, the two do share some attractive similarities. Holly Energy Partners' revenue stream comes from long-term, fixed-fee contracts that mostly insulate it from the ups and downs of commodity prices. In fact, 100% of its contracts and services are fee based, so the only exposure the company has to commodity prices is if a shift in values caused the volume of products moved to decline significantly.

The other thing that makes Holly Energy Partners similar to Enterprise is that its management has eschewed a common modus operandi of other master limited partnerships, which often try to increase payouts too quickly and end up paying out all their available cash. Instead, it has elected to grow its dividend at a rate that keeps some cash on the books each quarter to either support funding of other projects or as a safety net in case earnings unexpectedly turn south. This conservative approach has allowed the company to raise its dividend every quarter since it IPO'd back in 2004.

It also helps that Holly Energy Partners has support from its general partner HollyFroniter (NYSE: HFC). HollyFrontier's management has been one of the best in the oil refining business at allocating capital to high return projects, and it is using that approach with Holly Energy Partners as well. For the company's projected capital spending of $65 million to $85 million this year, the company expects 2017 EBITDA to increase by $51 million. Those high rates of return should be more than enough to keep its payout streak alive for a while longer.

Dividend already cut, big catalyst on horizon

One integrated oil and gas company that routinely gets overlooked -- despite a $50 billion market cap and a dividend yield of 5.8% -- is Eni. Based on some of the moves theItalian company has made to shore up its balance sheet as of late and the big production bump it will soon receive from a massive gas discovery last year, it may be time to start paying attention.

Yes, because of the steep decline in oil prices over the past couple of years, Eni was the first -- and so far the only -- integrated oil and gas company to cut its dividend, a move it made in March 2015. For those who held its shares at the time, that probably stung. However, that 28% dividend cut helped to free up $1.2 billion in cash that it can now use to close the gap between its spending and its income over the next couple of years -- which it is likely to need, given that oil companies are forecasting that oil prices will remain low for some time. This should mean that Eni's current dividend will be stable, and put it in a position to grow after the company starts production at some of its major new projects in the coming years.

The biggest of those start-ups will be in the Zohr discovery off the coast of Egypt, which is estimated to hold 30 trillion cubic feet of natural gas, making it one of the largest discoveries of the past century. Also, it will be a relatively lower cost source because there is already robust oil and gas infrastructure nearby. Eni is looking to sell a small equity stake -- about 20% -- to help pay for the development, but even after accounting for the sale, that one new field alone should boost Eni's production by 10%. With projects like these on the horizon, and a currently healthy financial situation, Eni's dividend looks pretty attractive.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Tyler Crowe owns shares of Enterprise Products Partners.You can follow him at Fool.comor on Twitter@TylerCroweFool.

The Motley Fool recommends Enterprise Products Partners. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.