3 Dividend Stocks for Successful Investors

Not every stock investorisexclusively interested in growth. Plenty of long-term investors who have managed to squirrel away a tidy fortune for themselves are far more interested in capital preservation as opposed to capital appreciation.

If you count yourself in that enviable situation, then you should be on the hunt for stable businesses that pay out a dividend. Our team of Fools thinks you should check outChurch & Dwight (NYSE: CHD),Las Vegas Sands (NYSE: LVS), and Sherwin-Williams (NYSE: SHW).

Image source: Getty Images.

A low-risk consumer giant

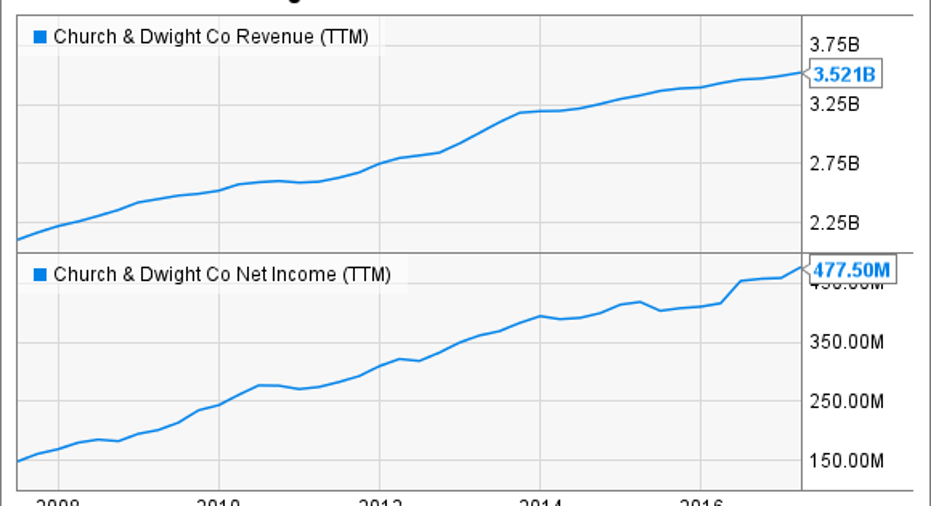

Brian Feroldi(Church & Dwight):Arm & Hammer. XTRA. Oxi Clean. Orajel. Trojan. Vitafusion. What do all of these beloved household products have in common? They are all owned by Church & Dwight, a consumer products company that has been in business since 1846!

One big benefit of selling personal care and household products is that consumer demand tends to be inelastic. That's a fancy way of saying that consumers don't stop buying baking powder or laundry detergent just because the economy slows down. When combined with the company's ability to consistently raise prices and introduce new products to the market, Church & Dwight's financials statements are about as reliable as they get.

CHD Revenue (TTM) data by YCharts.

This financial stability translates into a few big shareholder benefits. For one, the stock's beta is only 0.38, which means it's far less volatile than the S&P 500 in general. In addition, the company can use its dependable profits to reward shareholders with a steadily rising dividend (which currently yields 1.5%) and healthy amounts of stock buybacks.

The only knock against Church & Dwight is that the company regularly commands a premium valuation. That's certainly true today as shares are currently trading just south of 25 times forward earnings. While that might be a tad expensive for a mature business, I'm a firm believer that it is worthwhile to pay up for quality. If you agree, then I think it will be worth your while to give Church & Dwight a closer look.

A dividend stock to bet on

Travis Hoium (Las Vegas Sands): Investors wanting to successfully invest in dividend stocks need to look for companies that generate plenty of cash year after year to pay that dividend. And in 2017, a great place to look is the gaming industry, particularly Las Vegas Sands. The company has spent billions building out resorts in Las Vegas, Macau, and Singapore, and now it's time to cash in.

In the last 12 months, Las Vegas Sands has generated $4.36 billion in EBITDA, a proxy for cash flow from a resort. The current dividend yield of 5% requires $2.32 billion in cash to continue to be paid out. That means the company can continue growing the dividend, pay down debt, or fund growth projects like its proposal to build a resort in Japan.

The wonderful thing about Las Vegas Sands' business and its dividend is that it's protected from competition. Macau has only six concessionaires, and the government limits the number of casinos and gaming tables in the region. In Singapore, it's one of only two casino resorts, leading to a resort that generates around $1.5 billion in EBITDA annually.

Las Vegas Sands not only has a great dividend with room for growth, it also has cash flows that will be protected for years, even decades to come. And that's a stock successful investors should love.

Colorful dividend returns

Demitri Kalogeropoulos (Sherwin-Williams): For income investors, few metrics scream success as loudly as a good track record of market-thumping payout growth. Paint specialist Sherwin-Williams has this feature well covered. The dividend aristocrat's payout has tripled over the past decade, reaching $3.36 per share last year compared to $1 per share in 2006. That equates to an impressive compound annual growth rate of 13%.

Yet despite those gains, the company still pays out less than a third of its profits as dividends. And that's just one reason income investors can expect hefty payment growth in the future. For another, consider Sherwin Williams' profit margin, which recently climbed into the double-digits for the first time. The company is having no trouble passing along price increases in its paint stores even as sales volumes bounce higher. Those successes, combined with cost cuts, powered an 8% earnings boost last year -- outpacing the 5% revenue expansion.

Sherwin Williams might not make many income investors' radars given that its yield is trailing the broader market by a wide margin, at just 1% today. That's not due to management's holding back on payout boosts, though. In fact, the company's last hike was 25%. Those with a long-term outlook should consider building a stake in this paint giant to benefit from what could be many more similarly strong increases in the future.

10 stocks we like better than Sherwin-WilliamsWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now...and Sherwin-Williams wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017.

Brian Feroldi has no position in any stocks mentioned. Demitrios Kalogeropoulos owns shares of Sherwin-Williams. Travis Hoium has no position in any stocks mentioned. The Motley Fool recommends Sherwin-Williams. The Motley Fool has a disclosure policy.