3 Big Changes to Social Security on the Horizon

Social Security provides a valuable financial safety net to 60 million Americans. But payments to recipients are outstripping revenue collected from payroll taxes, and that means changes to the program are coming. The three changes below are among those on the table -- and while they may not be desirable, they may also be necessary to make sure Social Security is around when workers retire.

No. 1: Higher taxes

Social Security is a pay-as-you-go system. Revenue collected in the form of a 12.4% payroll tax, split between employees and employers, is used to make payments to current Social Security recipients.

That worked just fine when the number of working baby boomers far exceeded the number of retired Americans. But it's not working so well now that those baby boomers are retiring to the tune of 10,000 per day.

Because the impact of retiring baby boomers will further strain the program, many think an increase in tax revenue is needed. However, that doesn't necessarily mean that the payroll tax rate will go up.

Presidential hopefuls Hillary Clinton and Bernie Sanders, for example, have proposed raising the limit on income that is subject to the payroll tax. Currently, the payroll tax is only collected on income up to $118,500.

Clinton proposes exempting income between $118,500 and $200,000 but taxing any income above that level. Sanders agrees, but his plan calls for a tax break for income between $118,500 and $250,000.

No. 2: Higher ages

Social Security calculates your monthly benefit based on your 35 years of highest earned income and then uses actuarial tables to determine how much you'll receive in monthly benefits depending on when you claim.

100% of your monthly Social Security benefit is payable at your full retirement age. Currently, that age is 66. But the later you were born, the higher your full retirement age, which may be up to 67.

Depending on when someone is born, claiming Social Security earlier than full retirement age can reduce their Social Security checks by up to 30% compared to their primary insurance amount. People who wait to collect Social Security until age 70 can collect up to 132% of the amount they'd collect at full retirement age, depending on birth year.

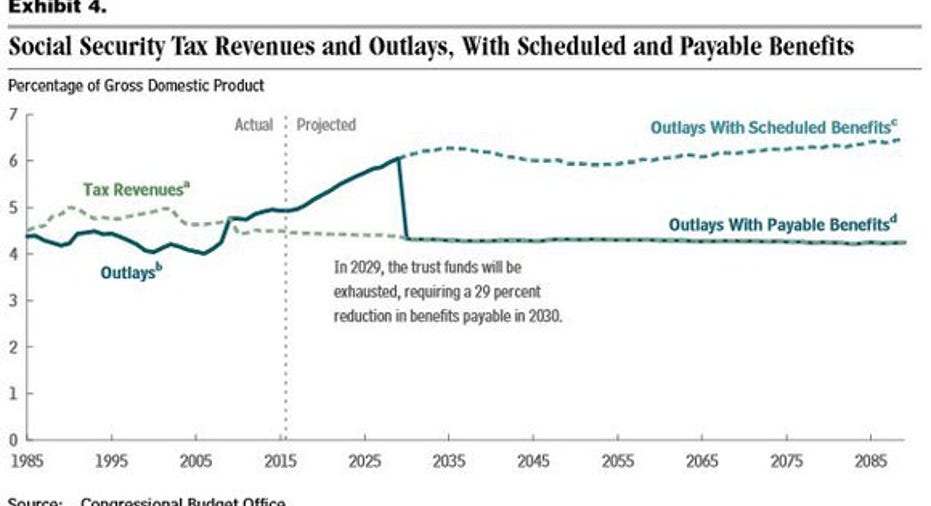

Since Social Security spending already outpaces tax revenue, and the Congressional Budget Office estimates benefits will need to be cut by 29% in 2030 absent any changes, some believe the full retirement age should be increased from 67 in order to 70 to reduce the program's annual spending.

Shifting the full retirement age higher may make some sense, given that when Social Security was designed, Americans' average lifespan was far lower than it is today. Nonetheless, any change to the full retirement age would likely be made slowly so that people near retirement aren't affected. This idea won't win many fans among people in their 30s, who will understandably recoil at the idea of working longer than they had hoped.

No. 3: Lower annual increases

The Social Security Administration adjusts the amount of income you receive depending on inflation. Currently, the SSA uses the Consumer Price Index to determine inflation rates and increases.

However, that could change in the future. Some lawmakers advocate basing benefit increases on another measure called chained CPI. Chained CPI is CPI adjusted to account for the fact that consumers tend to shift their purchases away from goods and services with high inflation rates to those with lower inflation rates.

Historically, chained CPI has increased more slowly than CPI, and therefore its use could save Social Security a lot of money. An analysis by the Congressional Budget Office in 2014 found that making this change would lower the average benefit paid to recipients in 2023 by $30. Considering that over 43 million Americans currently receive Social Security retirement benefits -- and that figure is climbing rapidly -- the savings could be considerable.

Tying it all together

Benefits will have to be cut if changes aren't made to shore up Social Security's finances. That's hard to imagine, given that among retirees, 53% of married couples and 74% of singles rely on the program for at least half of their income. In order to protect millions of retirees from falling into poverty, changes like these may be unavoidable.

The article 3 Big Changes to Social Security on the Horizon originally appeared on Fool.com.

Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.