3 Big-Cap Stocks That Are Growing Again

Image source: Getty Images.

A long-haul investing approach has been proven time and time again to outperform short-term trading, and with sales and profit ticking higher again at these large-capitalization companies, today may be the perfect time to stash them away in forever portfolios.

Big pharma, big medicine, big markets

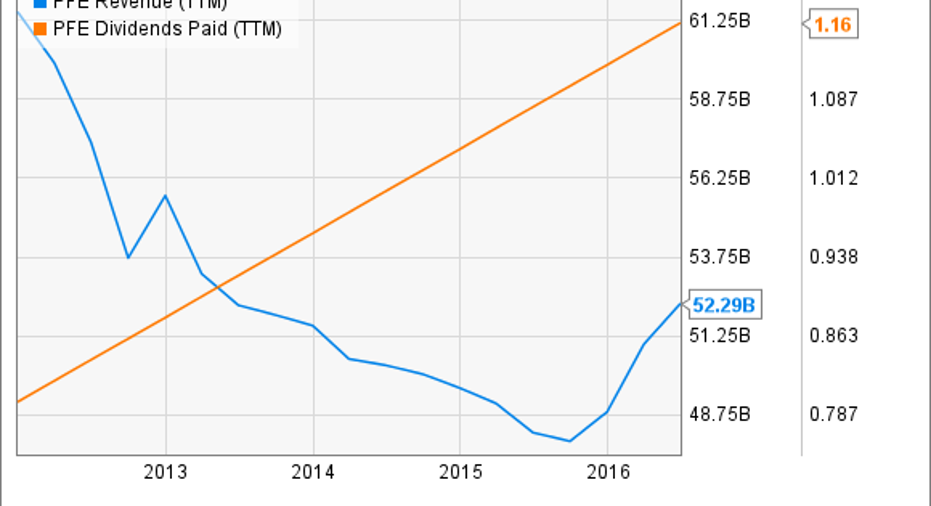

Pfizer Inc.'s(NYSE: PFE)sales have been sliding since patent protection ended on its megablockbuster cholesterol drug Lipitor, but sales have started to head higher again thanks to new drugs and acquisitions and that could make buying shares in this company savvy.

Growing use of the breast cancer drug Ibrance and the top-selling anticoagulant Eliquis have allowed Pfizer to deliver six consecutive quarters of operations growth. Global sales of Ibrance have surged to $942 million through the first six months of this year from $178 million in the comparable period of 2015. Meanwhile, Pfizer's alliance revenue, which includes its share of Eliquis sales (Eliquis is co-promoted by Bristol-Myers Squibb), has jumped 45% to $722 million through the first two quarters of this year.

The combination of rising sales for newer drugs like these and the acquisition of key companies that expand its footprint in biosimilars (via it's $17 billion acquisition of Hospira) and cancer treatment (via its $14 billion acquisition of Medivation) positions Pfizer nicely for future growth as well.

Exiting Q2, Pfizer is guiding for sales north of $51 billion this year, up from $49 billion last year. Pfizer's also targeting EPS of $2.38 this year, or more, up from $2.20 last year.If the company delivers on those targets, then it should be able to keep on rewarding investors with an above-market dividend yield, especially since management proved its commitment to income investors by upping the dividend payout when revenue was falling.

PFE revenue (TTM) data by YCharts.

Big changes fueling big profits

Microsoft Corp.'s(NASDAQ: MSFT)CEO Satya Nadella has a big vision for the global software Goliath that includes reducing its reliance on PCs and boosting revenue from cloud-based software solutions.

So far, Nadella's transformation of Microsoft is off to a solid start, and if he can continue to execute on his plan, then revenue and profit growth could make shares in Microsoft trade higher.

Thanks tosales in its productivity and business processes segment increasing 8% (constant currency) to $7 billion and intelligent cloud segment sales increasing 10% (constant currency) to $6.7 billion, Microsoft posted operational year-over-year sales growth of 5% in its fiscal fourth quarter. That's pretty darn good for a company that's been facing stiff headwinds associated with sluggish PC sales.

A big contributor to Microsoft's turnaround isOffice 365, its online productivity software suite. In fiscal Q4, Office 365 revenue from businesses grew 54% year over year. Another big contributor to top-line growth is Azure, its app building and management suite. Azure sales more than doubled from a year ago last quarter and Azure's netting 120,000 new subscribers every month.

Sales tailwinds are also offered by rising subscriptions for Xbox Live, which allows Xbox players to compete against one another online, and the integration of Bing search and Cortana throughout Microsoft's product line-up.Xbox Live membership grew 33% and search revenue improved 16% in the past year.

Overall, Microsoft thinks deeper integration within the 85% of Fortune 500 companies relying on its cloud products can help propel cloud-based revenue to $20 billion in 2018 from $12 billion today. That opportunity, a rock-solid balance sheet that boasts over $100 billion in cash, and the recent acquisition of LinkedIn could all make Microsoft a big-cap growth stock worth stashing away in portfolios.

Finally back on track

Food and Drug Administration sanctions, lawsuits, and sluggish demand have all taken a big toll on Boston Scientific (NYSE: BSX) investors over the years. However, it seems that fortunes may be improving for this beleaguered medical device maker.

BSX revenue (TTM) data by YCharts.

In Q1, sales were up 11.1% year over year and in Q2, sales jumped 15.4% from a year ago to $2.13 billion.Driving the accelerating growth was a 12.7% increase in cardiovascular sales, a 29% increase in medical surgical sales, and a 52.8% surge in defibrillator sales from a year ago.

The results led Boston Scientific to update its sales guidance for the year to north of $8.27 billion from prior expectations of more than $8.07 billion. Sales growth is also translating into gains on the bottom line.Non-GAAP EPS increased 22.7% year over year to $0.27 last quarter and that has management guiding for full-year EPS of $1.07 this year, up from guidance of $1.03 earlier this year.

Improving top and bottom lines have led to a big jump in the company's share price this year,but the rally may not be over. Management thinks it can boost its adjusted operating margin, and if so, then adjusted EPS should benefit from tailwinds in sales and cost savings next year. In 2015, adjusted operating margin was 22.3%, but management thinks it will grow to 25% in 2017 and more than 27% in 2020.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Todd Campbellowns shares of Microsoft.Todd owns E.B. Capital Markets, LLC. E.B. Capital's clients may have positions in the companies mentioned.Like this article? Follow him onTwitter where he goes by the handle@ebcapitalto see more articles like this.The Motley Fool owns shares of LinkedIn and Microsoft. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.