3 Bargain Stocks to Buy and Hold for a Decade

With the S&P 500 trading at all-time highs and soaring about 95% in the past five years, it's tempting to conclude that buying opportunities have disappeared. However, while there certainly may be fewer bargain investments than there were in the stock market five years ago, there are still a few enduring businesses worth buying today that could yield handsome profits for investors.

Indeed, three stocks look particularly enticing after selling off in the past year: Apple (NASDAQ: AAPL), Walt Disney (NYSE: DIS), and Netflix (NASDAQ: NFLX).

All three of these companies boast focused, enduring business models with excellent track records, yet their stocks are trading at valuations low enough to make them a buy. This isn't something that can be said every day about iconic brands consumers are using on a daily basis.

Here's why each of these stocks is worth buying and holding.

A straight-up steal

A wildly conservative valuation of Apple -- a valuation based on a forecast for growth no better than the historical rate of inflation -- pegs the stock's fair value at just under $130 per share. With shares trading at just $108 today, the stock is trading at a meaningful discount to fair value.

Image source: Apple.

But is such a lackluster forecast for the company's growth prospects realistic? In the past, the company has repeatedly wielded its brand recognition and pricing power in new segments, driving significant growth for the company -- and there's little reason to think the tech giant couldn't do it again. In addition, the same Apple garnering a higher switching rate from other smartphones to iPhone today than ever before will likely continue to attract new customers, keep existing customers around, and convince deeply entrenched users to keep buying new Apple products for years to come. Apple's seamlessly integrated ecosystem of hardware, software, and services has built the company both a "sticky" business model to retain its loyal customer base and a moat to keep competitors at bay.

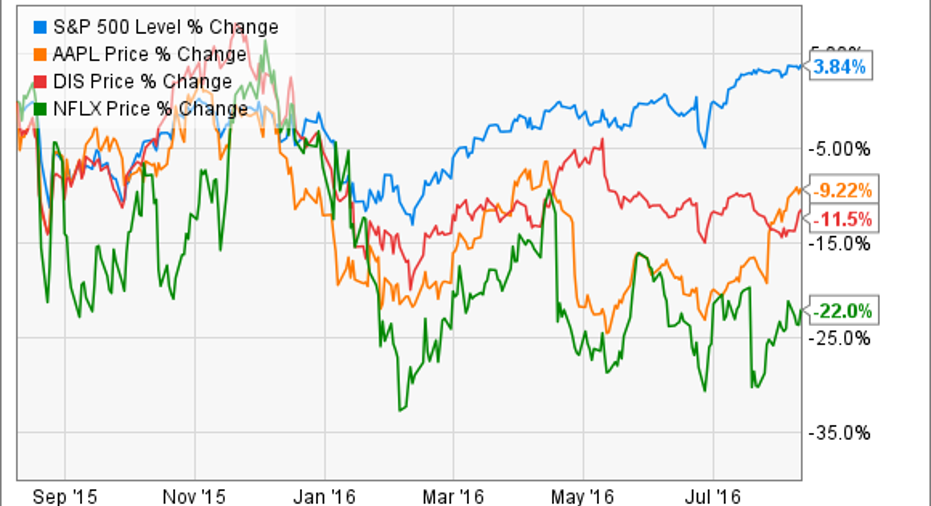

As investors fret about Apple's declining iPhone sales in 2016 as the company faces the tough comparisons to its monster iPhone 6 cycle last year, the pullback in the stock price offers investors an attractive entry point.

An undervalued collection of brands and franchises

Imagine if you could buy a slice of some of the world's hottest characters, brands, and franchises in entertainment -- think Disney, Marvel, Star Wars, Pixar, ESPN -- all at a bargain price.

You can. Thanks to the stock's underperformance recently, investors can pick up shares of Walt Disney, which owns all of these brands and franchises, for aprice-to-earnings ratio of just 18 -- a steal compared to where the stock was trading as recently as late last year.

DIS PE Ratio (TTM) data by YCharts.

A testament to these franchises' pricing power, Walt Disney's collection of powerful assets generated a record $9.2 billion in net income during in the trailing 12 months -- nearly doubling the company's $4.8 billion in net income in fiscal 2011.

Going forward, there's no reason to believe Walt Disney won't continue to effectively squeeze everything it can out of its diversified set of powerful assets. Yes, Disney's transition of ESPN from its cable roots to an Internet-streaming future may be introducing some near-term challenges, but the dominant sports network isn't going anywhere. As investors question the future of ESPN, now is a good time to buy a slice of some of the most enduring brands in theworld.

A focused bet on the inevitable transition to streaming TV

Netflix stock isn't cheap -- at least it's not when compared to its slower-growing peers. Its price-to-sales ratio of 5.4 is almost twice Disney's of 2.9. But a dominant player in the middle of a huge secular trend shouldn't be expected to trade conservatively. Fortunately, however, Netflix stock has been slammed recently, declining 22% in the past 12 months, making it more enticing than it was.

Not only is Netflix growing rapidly, but it's building out a massive library of compelling, original content. Image source: Netflix.

Living up to its valuation, the company is seeing rapid growth. On the back of an undeniable shift toward streaming TV, Netflix's total streaming members have increased from 65.6 million to 83.2 million during the past 12 months. And growth persists; in Q3 alone, the company expects to add 2.3 million more streaming members.

Longer-term opportunities look significant, too. Management expects its U.S. member base will eventually peak between 60 to 90 million members -- up from 47 million today. And with just 38 million streaming members outside of the U.S., Netflix's international expansion still has significant room to run.

Still, if the company's long-term potential truly is compelling, why are shares down 22% in the past year? The sell-off follows two arguably shortsighted concerns: Investors expected faster international adoption, and the company missed its second-quarter guidance for streaming members as extensive media coverage of the company's price increase sparked near-term headwinds in member churn rates.

These concerns are creating buying opportunity, as both are arguably worse than they seem. In international markets, Netflix is working to localize its international offerings in order to attract more customers. And the company's price increase was actually well received by the members being un-grandfathered into the higher price; it was simply confusion among other members about hyped media coverage of the price increase that prompted the worse-than-expected churn.

While they are trading lower, now is a great time for investors to buy shares of these iconic companies and hold them for the long haul. Investors who buy these stocks today may be sitting on much larger portfolios 10 years from now.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early, in-the-know investors! To be one of them, just click here.

Daniel Sparks owns shares of Apple. The Motley Fool owns shares of and recommends Apple, Netflix, and Walt Disney. The Motley Fool has the following options: long January 2018 $90 calls on Apple and short January 2018 $95 calls on Apple. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.