3 Bargain Stocks Smart Investors Are Already Buying for Retirement

Image source: Getty Images.

Preparing one's portfolio for retirement probably means choosing different investments than you have been. Chances are, you will steer clear of high-risk, high-reward stocks and focus instead on more stable investments that will at least protect your principal and pay a dividend to supplement your income. The only thing that makes finding these kinds of investments better is when you can get them for cheap.

So we asked three of our contributors to highlight a stock they see as a great investment for those either in or approaching retirement and that can be bought at a discount today. Here's what they had to say.

Get income and greater diversification

Dan Caplinger: One key to success for wealthy investors is diversifying your investment holdings to ensure that you spread out your risk across different types of investments. HCP (NYSE: HCP) offers investors the chance to do exactly that, because the real estate investment trust's exposure to healthcare-oriented properties produces income streams that most traditional stocks typically can't match. Currently, HCP offers a yield of nearly 6%, and the prospects for the industry are such that investors can expect healthy income generation well into the future.

HCP investors need to understand that the REIT is going through a corporate transformation, with plans to spin off its portfolio of HCR ManorCare post-acute skilled nursing facilities. At this point, many expect the spun-off entity to be more conservative in its dividend policies. But the continuing HCP has incentives to sustain its generous dividend payouts into the future, especially because it was the first REIT to qualify for status as a Dividend Aristocrat because of its track record of more than a quarter-century of rising dividends. By adding real estate exposure to your portfolio by including shares of HCP, you can broaden your asset base in a way that could also increase the amount of income your portfolio generates for your personal use.

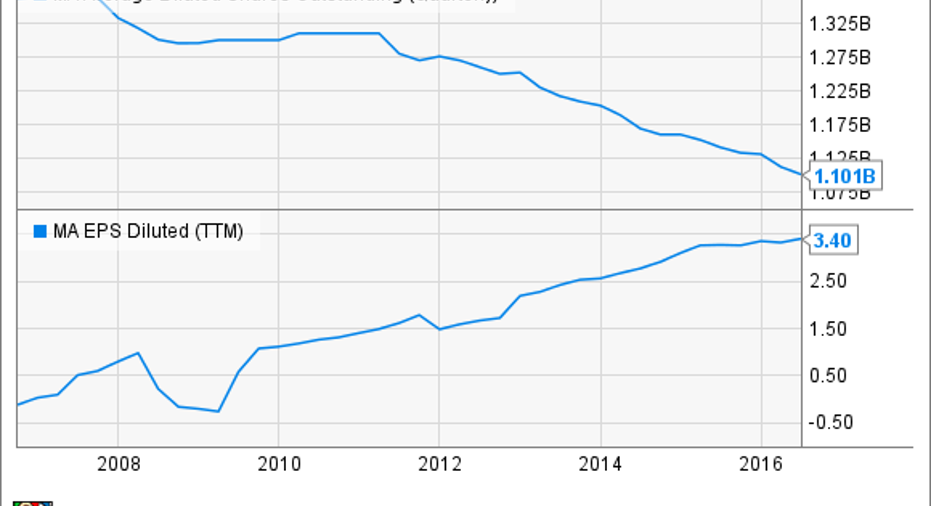

A future Dividend Aristocrat

Brian Feroldi:Futureretirees should be looking for ways toincrease their income once they stop working, and a smart way to do that is to buy stocks that should be able to boost earnings and dividend payments over long periods of time. I have high conviction that the payment giant MasterCard (NYSE: MA) should be able to pull off that feat in the decades ahead, so I think it's a great stock to buy and hold today.

MasterCard's second-quarter results reaffirmed that the company's long-term growth trajectory is intact. Revenue grew by14% excluding currency movements, thanks in no small part to the 2.3 billionMasterCard-branded cards in circulation. As consumers around the world continue to warm up to the idea of using plastic instead of cash, that number is bound to grow.

With the top line destined for long-term growth, MasterCard can use its huge financial strength to reward shareholders. Last quarter, the company bought back5 million shares for $462 million, which helped to increase earnings per share at a faster rate than net income growth. MasterCard also has a long history of buying back shares to reduce its share count, which is helping to grow EPS at a rapid pace.

MA Average Diluted Shares Outstanding (Quarterly) data by YCharts.

At 28 times trailing earnings, MasterCard may not appear to be an obvious bargain, but since 85% of transactions worldwide still occur using cash or check, I think it is well positioned for decades of double-digit growth ahead. This company's rock-solid balance sheet, stellar management team, and highly scalable business model make this a great stock for future retirees to consider.

Down but far from out for long-term investors

Tyler Crowe:What investor doesn't want a steady stream of income coming from their portfolio in retirement? The only thing that investors likely want more is a higher yield on that investment. One way to get that higher yield without exposing yourself to the risk of dividend cuts is to look for great companies that are out of favor right now. One company that fits the bill today is oil rig driller and lessor Helmerich & Payne (NYSE: HP).

By most measures, Helmerich & Payne doesn't fit into the typical category of a company that would be a steady dividend payer. It's in a very competitive market where pricing power is very much in the hands of its clients. What sets Helmerich & Payne apart in this industry is how management has handled the company over the years that has allowed it to remain strong through the ups and downs of the industry cycles. Even today, after watching oil prices drop for more than two years and drilling activity come to a near standstill, Helmerich & Payne still has more cash on hand than debt outstanding and continues to generate enough free cash flow to cover its dividend payments. This conservative approach has allowed the company to maintain a streak of 42 years of ever-increasing payouts to shareholders.

With a dividend yield today of 4.3% and a price-to-tangible book value of 1.48 times, it's not the absolute cheapest Helmerich & Payne has been in the recent downturn, but the two metrics suggest that the company is quite undervalued compared to its long history. Anyone looking to add a cheap income-paying stock to their retirement portfolio should look closely at this company.

A secret billion-dollar stock opportunity The world's biggest tech company forgot to show you something, but a few Wall Street analysts and the Fool didn't miss a beat: There's a small company that's powering their brand-new gadgets and the coming revolution in technology. And we think its stock price has nearly unlimited room to run for early in-the-know investors! To be one of them, just click here.

Brian Feroldi owns shares of MasterCard. Dan Caplinger has no position in any stocks mentioned. Tyler Crowe owns shares of HCP. The Motley Fool owns shares of and recommends MasterCard. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.