12 Predictions for High-Yield BDCs in 2016

A great baseball player once said, "Never make predictions -- especially about the future."

Against his better judgment, I'm here to share 12 predictions about business development companies for 2016. Some will almost certainly prove true, while others will completely miss the mark. Such is the difficulty of forecasting.

But writing down my thoughts holds me accountable while offering the ability to see just how the world can change from one year to the next. Without further ado, here's some bold and not-so-bold predictions for the BDC industry in 2016.

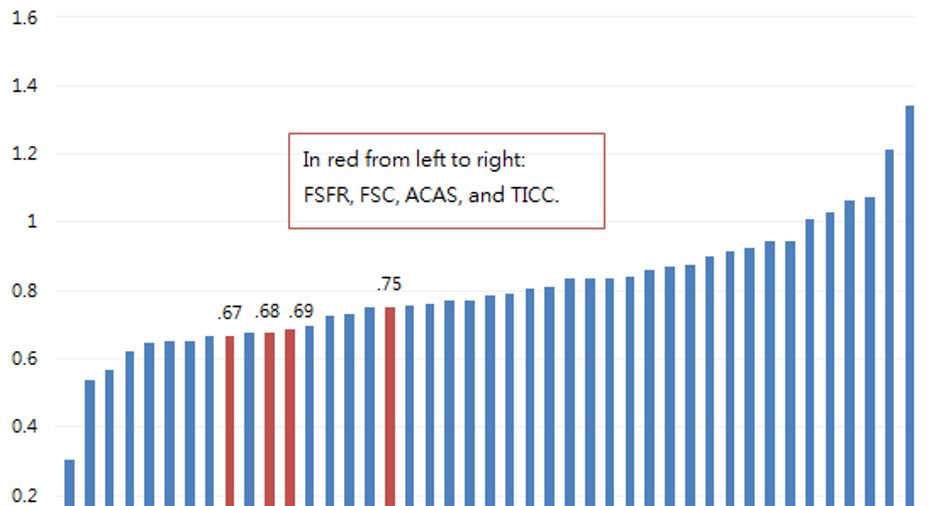

1. Activism will flourishAs the average BDC now trades at a discount of 20% to book value, activist campaigns are gaining steam. Fifth Street Senior Floating Rate Corp.,Fifth Street Finance , American Capital , and TICC Capital have already attracted activist attention. I think it's just a preview of what's to come in 2016.

The above BDCs were the "easy" targets -- large enough to justify the work and cheap enough to generate outsize returns if a campaign is successful. American Capital, TICC Capital, and Fifth Street all trade at less than 75% of book value.

Next year should bring activism to the next tier of cheap BDCs. But where two of three current activist campaigns favor big changes, like the ousting of a management team, I suspect the next round of activism may be less aggressive, pushing for middle-ground proposals like larger buyback plans.

2. We'll see the first troubled BDC takeoverThis is a pretty pessimistic prediction, but I think it'll prove true. At least one BDC will run into trouble managing its balance sheet, resulting in a "bailout by acquisition."

BDCs don't take deposits. They can't suffer from a traditional run on the bank, so to speak. But BDCs survive and thrive on leverage supplied by a revolving door of creditors.

Smaller BDCs are the likely target for an acquisition next year. As a rule, smaller companies in the industry make bigger use of fleeting credit facilities and expensive baby bonds to finance their portfolios. These are prime candidates for an acquisition, since financing expense savings add to the attractiveness of any deal.

Larger BDCs that have been graced with above-book valuations have a massive economic incentive to swap their high-priced stock for low-priced shares of their rivals.TPG Specialty Lending'scampaign to acquire TICC Capital likely won't be such an oddity next year.

3. Congress will support BDCsThe industry makes money by making loans regulators deem too risky for banks, to businesses that are too small to tap the Wall Street financing machine. A driving force behind their profitability is the use of leverage, or debt, to increase returns on equity.

Congress is considering a bill that would allow BDCs to leverage their balance sheets at a ratio of 2-to-1 ($2 of debt for every $1 in equity) compared to the current 1-to-1 limit.

I suspect that this bill will pass, though I doubt many BDCs will make the conscious decision to load up on debt -- at least not immediately. While Uncle Sam may not have a problem with higher leverage, ratings agencies (hopefully) will. Those who invest in BDC debt undoubtedly now have to worry about being "primed" by new issuance if Congress allows higher leverage.

4. Fewer new listingsIPOs are probably off the table in 2016. The "farm team" comprised of non-traded BDCs will likely remain private. FS Investment Corp , which has a number of non-traded "sister" funds, might opt to digest its private family members rather than see them go public as stand-alone companies.

This is really a matter of my own curiosity. New listings shouldn't have much impact on the industry from an investor's perspective. More is better for creating competition for investor capital, but there are already plenty of (too many?) BDC options on the market today.

5. Portfolio quality will generally deteriorateWhile I don't expect a second coming of the Great Financial Crisis, I do think we're in the late stages of a credit cycle. Deals done during frothy periods (say, the summer of 2014, when credit spreads were thin) will likely deteriorate with an additional year's time.

The pain in specific sectors like oil & gas isn't over just yet. You can be sure that all BDCs are exposed in some way to lower oil prices, if not directly, then indirectly. Companies stuffed with exotic investments like CLO equity have oil exposure, even if it doesn't show up in their industry concentration tables. Some have exposure both ways -- beaten down Apollo Investment being one such BDC with high oil and CLO equity exposure.

"Oil services" firms often sneak their way into a "business services" or "business-to-business" classifications on BDC balance sheets, somewhat obscuring a BDC's true exposure to commodities.

The story in 2016 is the end to oil price hedges. Where oil companies generally had some hedges to protect from a downdraft in prices this year, many industry executives have noted that the New Year will leave more companies exposed to the currently low market price for oil.6. BDCs will dose up on "activist repellent"I almost didn't believe it. Following its fiscal fourth-quarter earnings report,Medley Capital voluntarily cut management fees, increased its buyback authorization, and realigned its fee agreement so that management compensation is better aligned with shareholder returns.

I call it "activist repellent."

It's awfully convenient that investors might just get all the benefits of activism without the months-long proxy contests and expensive bickering back and forth.7. Speaking of CLOs ...The market has spoken. BDCs that invest in CLO equity are untouchable unless they trade at big discounts.

CLOs enable BDC management to play bigger accounting games with portfolio performance (see the most recent KCAP Financialconference call), inflate incentive fees, and expose investors to higher risks. I see no New Year reprieve for CLO-heavy BDCs that were punished with low valuations in 2015.

The condemnation of CLO equity is not a passing issue. CLOs are leveraged bets on bank loans, with the equity sitting below 10-14 times more debt that must be repaid first. When defaults are low, CLO equity returns are incredible. When defaults rise, however, the equity takes a beating. The easy money in CLO equity is gone, it seems.

8. More dispersion in performanceTake notice to dispersion in price-to-book ratios in the industry. While a rising tide generally kept all ships afloat through 2013 and much of 2014, BDCs are slowly being divided into two camps. As I write this, only six BDCs of 43 on my spreadsheet are currently valued at a premium to book value.

There are the upper-tier BDCs that have shareholder-friendly fee agreements and ample deal flow, which tend to trade in tight band relative to their reported book values. Then there is the second tier made up of BDCs that are cheap because of costly fee agreements, weaker deal flow, and emerging credit quality issues.

Fees will likely take center stage once again in 2016. But be advised: It's not about dollars and cents. It's all relative.

Investors who want their management teams to make money the same way shareholders do -- from consistent dividends and book value appreciation -- will invariably favor BDCs with shareholder-friendly fee agreements. Legacy BDCs that decide to stand pat rather than adapt will likely never make it back to book value. Note that only one BDC with an "old-school" fee agreement trades above book value.

9. Individual investors play a bigger role in governanceBDCs have been traditionally held by individual investors who, unfortunately, don't have the best record when it comes to voting at annual meetings. Next year, I suspect more investors will flex their voting power, and controversial initiatives supported by industry executives will face push back.

In particular, I expect votes on below-NAV issuance of stock to be much closer than in the past. BDCs have the ability to issue stock at below-book prices via rights offerings. Management teams ask for permission to make below-book issuance easier with at-the-market and secondary offerings. I submit that no one gains by making it easier for BDCs to destroy shareholder wealth with below-NAV stock issuance.

10. New focus by investorsNet investment income is so 2013 or 2014. Next year, I anticipate that investors will focus more of their attention to net income rather than more forgiving earnings metrics like net investment income.

As most BDCs are growth constrained, no longer will investors write off big "one-time" capital gains or losses. Capital losses that were forgivable as balance sheets grew will be doubly painful as balance sheets shrink.

11. Dividend cuts will continueThere were a number of sizable dividend cuts in the last year, primarily because several fast-growing BDCs came to a screeching halt in 2015. When BDCs slow their balance sheet growth, origination-related income sources fall, applying gravity to stretched dividend yields.

Next year, generally higher non-accruals and defaults will lead to lower returns, resulting in smaller payouts. Likewise, I think it's safe to assume many companies have already picked their winners from their portfolios, realizing their gains to fund special dividends. Special dividends some investors have come to rely on might not be so reliable next year.

If its any consolation, this isn't news. The industry is broadly priced for higher investment losses, dividend cuts, or both.

12. Not one BDC will liquidateIt remains a curious reality that BDCs simply do not liquidate. From the below-NAV sales of Patriot Capital and Allied Capital following the credit crunch to the more recent combination of MCG Capitaland PennantPark Floating Rate, precedent says that BDCs are frequently merged, but never wound down.

It's something of an annoyance for me and other investors, but the incentives for management teams make liquidations unlikely. Despite my steadfast belief that activist pressure will increase in 2016, I remain equally committed to the prediction that not one low-priced BDC will liquidate next year.

It's my view that BDCs which trade at perpetual discounts to NAV best serve their shareholders by liquidating. How long can managers justify letting dollar bills trade for $0.70 without action to create value for shareholders?

The article 12 Predictions for High-Yield BDCs in 2016 originally appeared on Fool.com.

Jordan Wathen has no position in any stocks mentioned. The Motley Fool recommends Apollo Investment. Try any of our Foolish newsletter services free for 30 days. We Fools may not all hold the same opinions, but we all believe that considering a diverse range of insights makes us better investors. The Motley Fool has a disclosure policy.

Copyright 1995 - 2016 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.