Why Women Need to Save More...a Whole Lot More

Women, listen up. It is not an equal playing field when it comes to money and retirement for men and women. Here’s the harsh reality: women earn about 77 cents on the dollar compared to men. Their earnings often peak out at an earlier age and women tend to opt out of the workforce sooner than men. Women also tend to live longer. So for many women, they are earning less, saving less for retirement due to fewer working years and they may need to stretch out their retirement savings over a much longer period of time.

Save & Start Young

To make up for these shortcomings, financial advisors say it is crucial for women to build up their retirement savings and start early. Jocelyn Wright, Director of the Center for Women and Financial Services at The American College, says women should aim to save at least 15%-20% of their income, ideally starting in their 20’s. “This would set the stage, so as you earn more, you’ve already been accustomed to putting that money aside. The sooner you can do it, the better. It’s much more difficult, the older you get,” Wright says.

Financial Game Plan

Wright recommends setting a financial game plan starting right after college or in your 20’s. Aim to live within or below your means. Begin paying off any student loan debt. Start putting money towards retirement in a 401(k) or IRA account. As your salary increases, begin to increase the amount designated for retirement.

In Your 30's:

Negotiate and earn more. Make sure to max out retirement contributions and take advantage of matching contributions from employers. Start to set aside money beyond retirement savings. Set up emergency savings—three months of expenses if married and six months of expenses if single.

In Your 40's:

Earnings may peak soon so aim to maximize wages. Consider insurance including long-term care and life insurance to protect your retirement savings. Don’t sacrifice your retirement savings to fund your child’s college education.

In Your 50's:

Look to pay down debts and continue to max out retirement contributions. Add $6000 a year to your 401(k) as a catch-up contribution. Consider extending working years, find ways to increase earnings.

In Your 60's:

Navigate your retirement options. Seek financial advice to figure out when to retire and when to file for Social Security. Companies including XY Planning Network offer financial advisory services on an hourly basis.

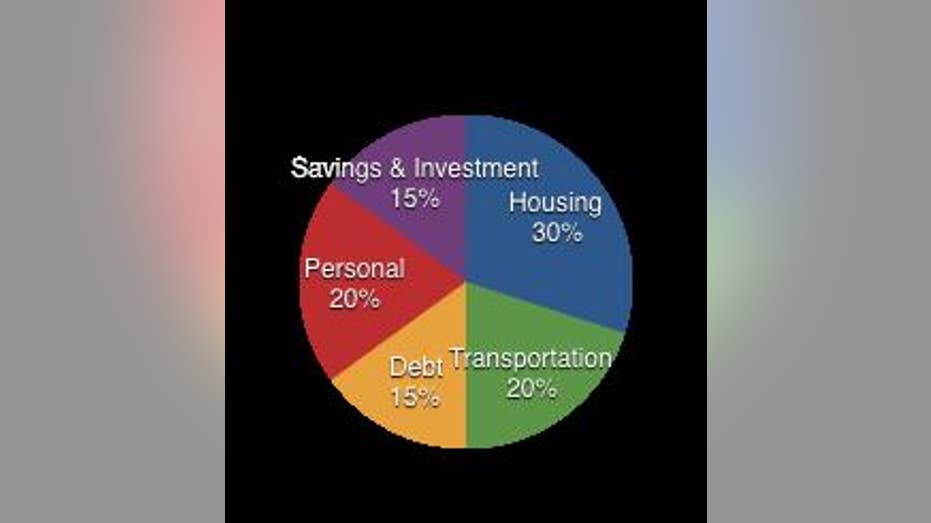

When setting a financial game plan, Wright also says it is important for women to monitor their daily spending habits and set a basic budget to keep expenses and savings on track.

Aim to Work for 35 Years

As for Social Security, women tend to receive lower Social Security benefits than men according to AXA. Social Security benefits are calculated, in part, by using the highest 35 years of earnings. If you haven’t work that long and many women fail to reach that mark, Social Security will calculate zeros for the unemployed years up to 35 years. This will likely bring down your monthly benefits. Bottom line for women: aim to work 35 years to maximize your Social Security payout.