How to Survive a Financial Storm

Dear Dave,

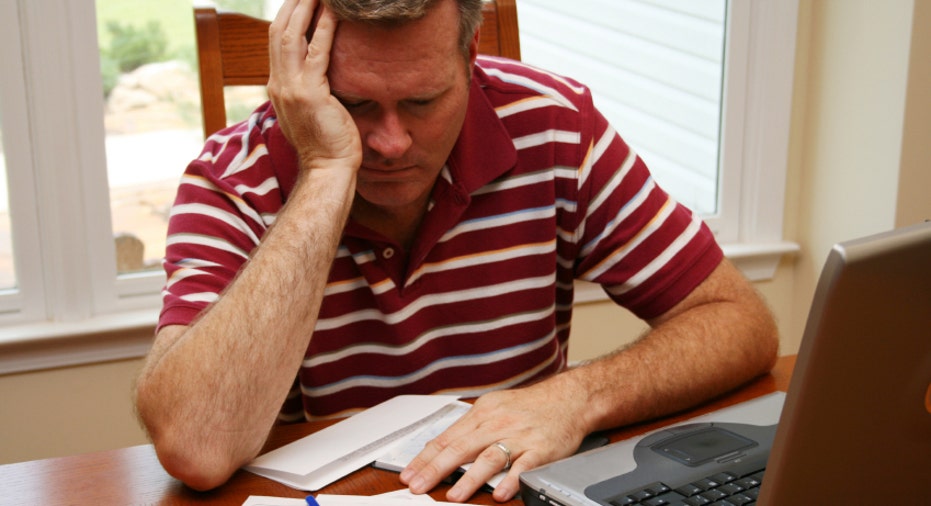

Recently, my husband had to quit his job due to an old back injury. We have $25,000 in debt, but I’ll be receiving a $38,000 inheritance in a couple of weeks. Should we use the money to pay off our debt, or hold on to it in case he needs surgery?

Kristen

Dear Kristen,

Now is the time to keep the cash piled high. You’re in the middle of an emergency, and that means you push the pause button on your Total Money Makeover and stop paying extra on debt. Surgery is a possibility at this point, plus you may need some of that money to live on until his job situation improves.

Then, the moment he returns to work and things are stabilized, you jump back into getting control of your finances. Use whatever is left of the $38,000 to pay off debt that very day. But right now you don’t need to worry about becoming debt-free, only to turn around and be in a mess in the event he has trouble finding another job.

Let me give you a warning too. Thirty-eight thousand dollars is a great gift. If someone handed me a check for that amount, I’d cash it in a heartbeat. But it’s not $380,000 or $3.8 million. It’s easy to develop a false sense of security if you’ve never received a check of that size. This kind of money is enough to keep the wolf away from the door for a while, but it’s nothing to retire on.

This little nest egg is a real blessing, Kristen. Just make sure you handle it wisely, and take into account all of the possibilities over the next couple of months. In a best-case scenario your husband won’t need surgery, he’ll find a job pretty soon, and you guys won’t have to dig in to the inheritance money. Hang on to as much as possible, though. This sounds like a time of personal and professional transition for you both, and having that kind of extra cash around could be a lifesaver!

-Dave

Dear Dave,

My husband and I are on Baby Step 2 of your plan. We move every two or three years due to our jobs, so would it ever make sense in our situation to buy a house?

-Janelle

Dear Janelle,

In most cases like this it doesn’t make sense to buy a house, especially if the real estate market in your area is lethargic. Some markets have bounced back and are doing very well, while some are worse than slow. It all depends on where you’re moving.

Here’s the big question: Can you get the place sold quickly the next time you have to move? Another thing to consider is whether or not you can sell it for more than it cost when the time comes. If not, you’ll be writing a check for home ownership, and that’s not a good plan.

As a general rule, a two- to three-year window is not enough time to own a home. There are rare exceptions to this rule, places where you have a hot, escalating price market. But if you’re not careful you’ll end up leaving behind a rental property and playing landlord, whether you want to or not!

-Dave

* Dave Ramsey is America’s trusted voice on money and business. He has authored four New York Timesbest-selling books: Financial Peace, More Than Enough, The Total Money Makeover and EntreLeadership. The Dave Ramsey Show is heard by 6 million listeners each week on more than 500 radio stations. Follow Dave on Twitter at @DaveRamsey and on the web at daveramsey.com.