Heal Your Wallet After the Holidays

The wrapping paper is strewn across the floor. The kids have raced to the far corners of the house to try out their new gadgets. And suddenly the thought hits: Just what did Christmas cost this year?

In the frenzy of shopping and gift-giving that marks the holiday season, it's not unusual to go overboard. If you find yourself in the wake of excessive spending with bills piling up all around, don't despair. Here are five steps to bounce back from a holiday spending spree:

1. Evaluate the situation

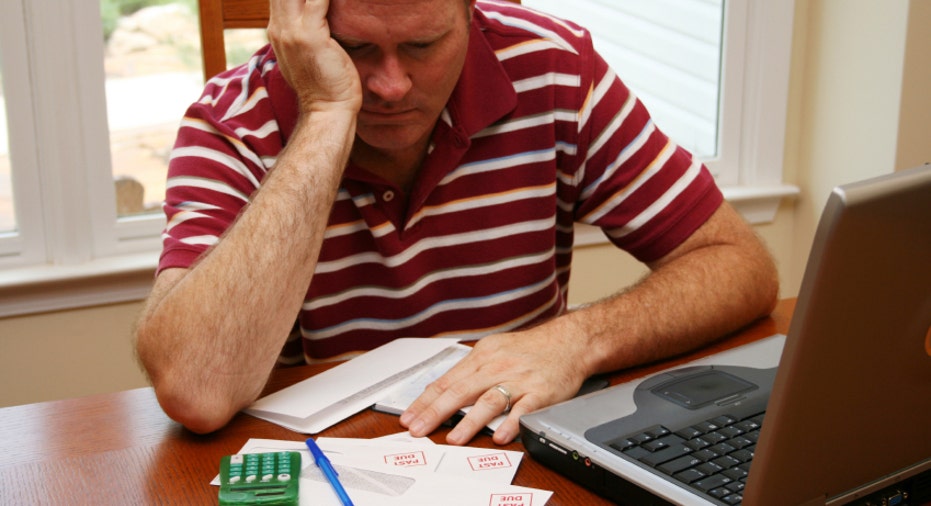

Ignorance may feel like bliss, but avoiding the painful reality of your holiday spending does little to improve your situation. Take a deep breath, pull out the receipts and prepare to face the cold, hard numbers.

Once the initial shock of the total cost wears off, break down your bills into groups. For example, calculate how much you spent for each family member or group of recipients. Don't forget to include incidental expenses such as wrapping paper, tape and food when totaling the cost of your Christmas celebration.

2. Minimize the damage

Did you pay for your Christmas with cash? Then congratulations, you can skip this step! Otherwise, it is time to determine how to avoid paying any more than necessary in interest and fees. Review the interest rates on your credit cards and any deferred payment plans used to finance purchases. Then consider whether you can transfer balances to other cards with lower interest rates. Now is the time to take advantage of those low introductory rate offers that may be arriving in the mail.

3. Create a plan of attack

Once you know what you owe, your next step will be to determine how best to pay off any outstanding balances. List the balances in order of interest rate. Starting with the highest rate, divert any extra money you have to that payment. Once bill number one is paid off, roll that payment amount into the minimum payment due for the next highest-rate bill on the list. Using this "snowball" technique can work to quickly knock out outstanding balances.

If you paid for the holiday with money from your savings accounts, you'll want to replenish that amount as soon as possible. Review your budget to see where you may be able to reduce expenses and send more to a high-interest savings account to help rebuild your stash of cash.

4. Scout out extra dollars

Of course, this process will go more quickly if you can find extra money to pay down your debt. While it is important to maintain a healthy savings account for emergencies, it doesn't make sense to have extra money sitting in savings if you are paying high interest rates on credit cards. If appropriate, consider pulling some money from your savings account to pay off those card balances.

Another way to find extra money is to simply look around your house. Most families are practically surrounded by cash just waiting to be found. Old movies, exercise equipment, video game systems and more can be sold for cold, hard cash. If your beloved gave you the latest smart phone for Christmas, sell the old one. The same is true for practically every item in your house. Get creative and watch the money start to flow in as your old, unwanted stuff goes out.

5. Resolve to do things differently

Perhaps the most important step is to avoid making the same mistake over and over again. If you charged your holiday, look for savings accounts with high interest rates to store next year's funds or open a Christmas Club account. Divide your total cost for this year by 12 and put that much away into the account each month.

If your budget can't absorb that much, then it is time to reevaluate your spending. Go back to step one and review the numbers. Do you really need to spend $30 on the cousin you see once a year? Does Christmas dinner really have to cost $75? Decide which amounts make sense based upon your relationships and budget. Then write it down and commit to spending that much -- and only that much -- next year.

The holidays don't have to harm your budget. You can't go back in time to correct what went wrong this year, but you can be proactive for the future. Take the time to carefully review your holiday spending habits and resolve to head into 2012 with a wiser approach.

The original article can be found at SavingsAccounts.com:Heal your wallet after the holidays