Employers Add 163K Jobs as Unemployment Rate Increases to 8.3%

U.S. employers in July hired the most workers in five months, but an increase in the jobless rate to 8.3% will probably keep expectations of additional monetary stimulus from the Federal Reserve intact.

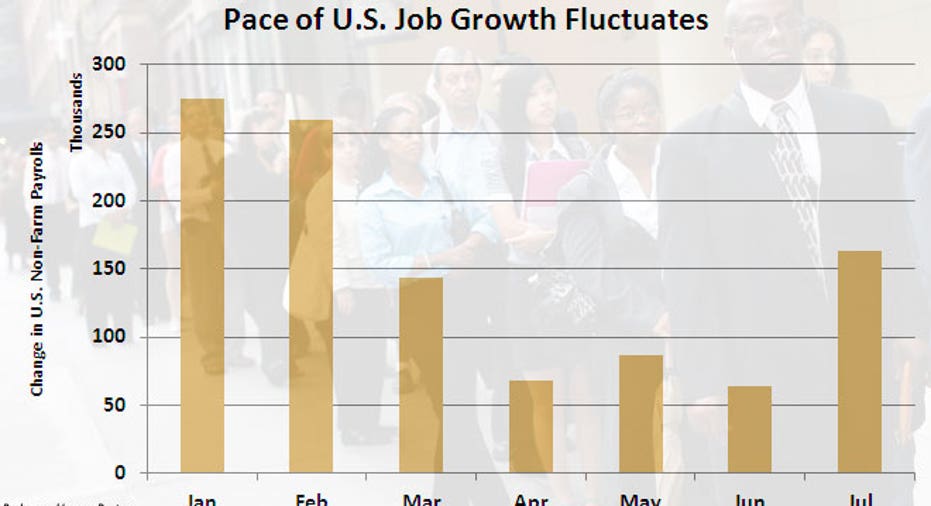

Nonfarm payrolls rose 163,000 last month, the Labor Department said on Friday, beating economists expectations for a 100,000 gain. The report was dimmed somewhat by the increase in the jobless rate from 8.2% in June, even as more people gave up the search for work.

In addition, employment for May and June was revised to show 6,000 fewer jobs created than previously reported. The closely watched employment report comes two days after the U.S. central bank sent a stronger signal that a new round of major support could be on the way if the faltering recovery does not pick up. Most economists expect the Fed will launch a third round of bond purchases, possibly at its next policy meeting on Sept.12-13.

That's despite the approach of the U.S. presidential and congressional elections in November, which could leave the central bank open to criticisms from Republicans who have made the weak economy a centerpiece of their campaigning. The Fed has held interest rates close to zero for nearly four years and pumped about $2.3 trillion into the economy. At the Fed's next meeting in September, policymakers will also have had a chance to see August's payrolls report.

The labor market slowed sharply after strong gains in the winter, spelling trouble for President Barack Obama. A recent Ipsos/Thomson Reuters poll showed 36% of registered voters believe Republican presidential candidate Mitt Romney has a better plan for the economy, compared to 31% who had faith in Obama's policies. The unemployment rate has been stuck above 8% for more than three years, the longest run since the Great Depression.

Fears of deep government spending cuts and higher taxes that are due to begin in early 2013 and fears that Europe's debt crisis could get worse have dissuaded employers from hiring, economists say. Economists say the biggest factor weighing on sentiment is fear that politicians in Washington will be unable to avoid the so-called fiscal cliff at the turn of the year.

LIMITED JOB DESTRUCTION

"We are not seeing large scale layoffs, so job destruction is pretty limited,'' said Scott Brown, chief economist at Raymond James & Associates in St Petersburg, Florida. "The problem all along has been a lack of hiring and we expect that the uncertainty about the elections, the fiscal cliff and Europe may restrain the pace of hiring as well as capital spending,'' Brown said before the release of the report.

Data last week showed the economy grew at an annual pace of 1.5% in the second quarter, far short of the 2.5% rate needed to keep the unemployment rate stable.

The private sector again accounting for all the job gains, adding 172,000 new positions. Government payrolls dropped by 9,000, as local governments laid off teachers. Construction employment dipped 1,000, despite increases in home building. Manufacturing payrolls increased 25,000, largely because of fewer layoffs in the auto sector as manufacturers kept production lines running during the month.

Within the vast services sector, employment gains were widespread. Temporary help services increased 14,100. Businesses are hiring temporary workers due to the uncertain outlook. Hiring in the utility sector was restrained by a strike at a power firm in New York last month. Average hourly earnings increased 2 cents last month, suggesting consumer spending will struggle regain steam after it slowed sharply in the second quarter. The average workweek was unchanged at 34.5 hours.