Veterans borrowing VA loans at a record pace, study shows: Is this mortgage option right for you?

1.2 million veterans tapped into their VA home loan benefits in 2020, and even more are expected to do so this year. See where retired military service members are taking out VA loans at the highest rate, and learn more about the eligibility requirem (iStock)

Military veterans have access to low-interest home loans through the U.S. Department of Veterans Affairs (VA). The VA has said it backed a record-breaking 1.2 million loans in 2020, and a new study suggests it's already on pace to break that record again in 2021.

Average consumers and military veterans alike have been able to take advantage of home buying and mortgage refinancing while rates are low. VA refinancing loans were up 76% in the first half of 2021 compared to this time last year, and the demand for VA purchase loans increased by 10% during this same time period, according to a new study by Veterans United Home Loans. The study also analyzed the top cities for VA homebuyers to find out where veterans are moving.

Keep reading to learn more about the housing market trends among veteran homebuyers, and learn how to take out a VA loan for refinancing or buying a home. And if you're unsure about your loan eligibility, you can visit Credible to get in touch with experienced loan officers and have your mortgage questions answered.

HOUSING MARKET SHOWS SIGNS OF COOLING, WHICH IS GOOD NEWS FOR HOME BUYERS

Veterans are tapping into VA home loan benefits across the country

Military veterans are entitled to a number of benefits, including VA home loans. These loans don't require a down payment or private mortgage insurance (PMI), which is typically required if you don't put money down. VA loans are also lenient when it comes to debt-to-income ratio (DTI) and minimum credit score requirements, so they may be an option if you have fair credit or bad credit.

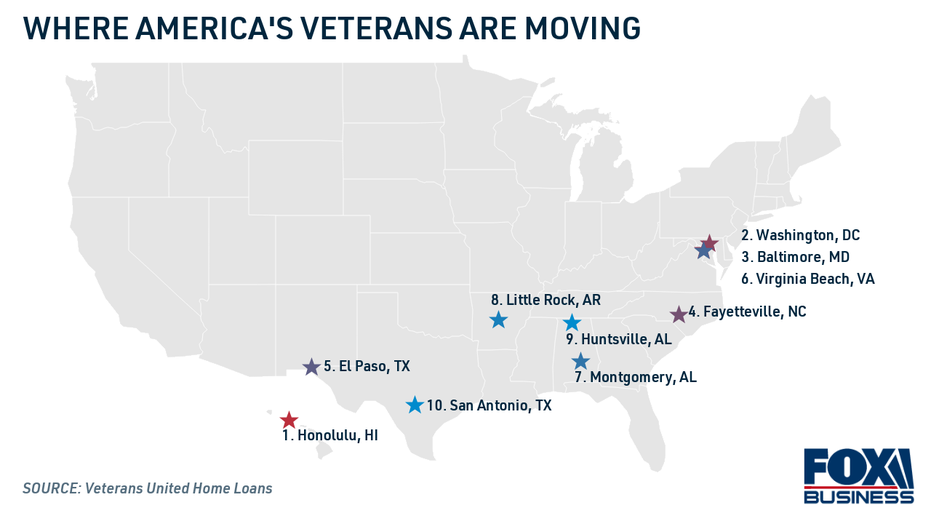

After their military service, many veterans are taking advantage of these VA home loan benefits by settling down in sunny climates, according to the study. The No. 1 metro area for VA loan growth is Honolulu, Hawaii, where loan activity nearly doubled year-over-year. Retired service members are also seeking the warmth of the South, flocking to states like Texas and Alabama.

Additionally, the study showed that veterans are taking out more VA loans in our nation's capital and the surrounding areas. Here is a list of the top 10 cities for VA loan growth:

- Honolulu

- Washington, D.C.

- Baltimore, Md.

- Fayetteville, N.C.

- El Paso, Texas

- Virginia Beach, Va.

- Montgomery, Ala.

- Little Rock, Ark.

- Huntsville, Ala.

- San Antonio, Texas

MORTGAGE REFINANCES RISE FOR SECOND STRAIGHT WEEK – HOW TO GET THE MOST OF OUT OF YOURS

Veterans aren't just putting down roots in new places; many are using their entitlement to refinance their existing loans to a lower interest rate with a VA loan, the study said.

Mortgage rates are currently low across the board for VA loans as well as conventional mortgages, which makes it a good time to finance a home regardless of your military status. And with home values increasing at a breakneck pace, it may be a good time for borrowers to take advantage of extra home equity with a cash-out refinance.

If you're thinking of buying a home or refinancing your current mortgage, you should explore your options by visiting the online loan marketplace, Credible.

HOW MUCH MONEY DO YOU REALLY NEED TO BUY A HOUSE?

Eligibility requirements for VA refinancing and home purchase loans

Taking out a VA loan is similar to taking out a conventional mortgage, as long as you meet the service requirements. Here are the VA loan eligibility requirements for military service and reserve members:

- You served at least 90 consecutive days of active duty during wartime or 181 days during peacetime, or less if you were discharged due to a service-related disability.

- You served 24 months of non-active duty during the ‘80s or ’90s, or less if you were discharged due to a service-related disability.

- You're the surviving spouse of a veteran who was killed in the line of duty, went missing in action or is a prisoner of war.

- You served in the National Reserve or National Guard with 90 continuous active-duty days of service or 6 years of service.

When you apply for a VA loan, you'll need to provide a certificate of eligibility (COE) so the lender knows you're eligible for this program. Your COE may be a copy of your discharge papers or a signed statement of service, depending on your military status.

Like a traditional mortgage, a VA loan requires you to buy a habitable home that meets minimum property requirements. You'll need a VA-certified home appraisal to confirm the value of the home.

STUDENT LOAN OPTIONS FOR US MILITARY MEMBERS, VETERANS

It may make sense to take out a conventional mortgage

Although the VA home loan benefits are significant, it's important to consider the drawbacks. VA loans can only be used to purchase a primary residence, so you can't use one to buy a second home, vacation home or investment property, Plus, the VA funding fee can add thousands to the cost of your mortgage.

If you decide to borrow a conventional home loan instead, you may be able to put as little as 3% down. And since mortgage rates are near historic lows, you'll likely get a low interest rate even without taking out a VA loan.

Military veterans should exhaust all their financing options when buying a home, so it's important to check mortgage offers across multiple private lenders and loan types. You can get prequalified for a conventional mortgage on Credible in just minutes to see offers tailored to you without impacting your credit score.

HOW TO REFINANCE A MORTGAGE AFTER HARDSHIP FORBEARANCE ENDS

Have a finance-related question, but don't know who to ask? Email The Credible Money Expert at moneyexpert@credible.com and your question might be answered by Credible in our Money Expert column.