3 Dividend Stocks That Prove Boring Is Beautiful

Even though large-cap dividend stocks can be downright boring to own at times, this group as a whole has produced far better returns on capital compared to their more exciting counterparts -- growth stocks -- in a historical context. The long and short of it is that dividends help to smooth out the rough times when the market decides to take an unexpected turn southward.

Armed with this insight, we asked three of our contributors which dividend stocks they think epitomize the tried-and-true "boring is beautiful" investing strategy. They suggested Pfizer (NYSE: PFE),Enterprise Products Partners (NYSE: EPD), andMacy's (NYSE: M). Here's why.

Image source: Getty Images.

This drugmaker's steady payout has been its saving grace

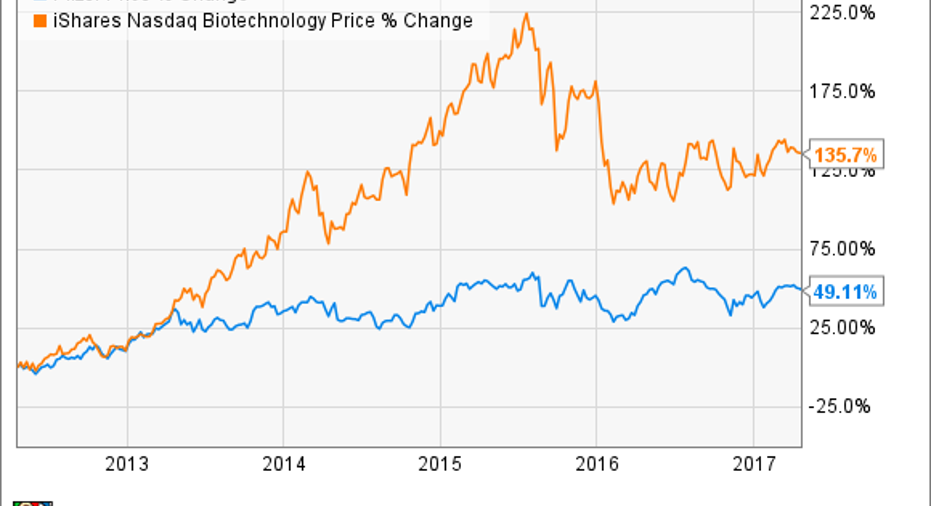

George Budwell(Pfizer): Over the past five years, Pfizer's shares have performed admirably, but have lagged well behind the high-flying biopharmaceutical industry as a whole.

Part of the problem has been the company's inability to churn out enough new blockbuster products like the breast cancer drug Ibrance to offset the parade of drugs that include former top sellers such as Celebrex and Lipitor that have been going off-patent in recent years. In addition, the drugmaker has arguably been a follower, and not a leader, in several emerging therapeutics areas such as immuno-oncology that have caused the valuations of many companies to swell of late.

Despite these headwinds, however, the company's remarkable history of paying a dividend for 313 consecutive quarters has still helped its shares outperform the broader markets in terms of total return on capital over this time period. In fact, Pfizer's total return on capital to shareholders over just the last quarter-century is close to a whopping 500% -- proving that its somewhat boring approach to creating value for shareholders is truly a thing of beauty.

PFE Total Return Price data by YCharts.

The most intriguing part of Pfizer's story, though, is arguably yet to come. With a sizable war chest to execute game-changing deals and a political climate that may reinvigorate so-called "tax inversions,"this drugmaker is poised to continue to produce above-average gains for its shareholders for the long haul.

51 straight quarters and counting

Matt DiLallo(Enterprise Products Partners):Pipeline and processing company Enterprise Products Partners isn't the most exciting company you'll ever come across. Its bread-and-butter business is operating pipelines that act like toll booths and processing plants that provide a fee for service. However, these assets generate very consistent cash flow, the bulk of which it distributes back to investors each quarter. Enterprise currently yields 6% and has increased the payout to investors 60 times since going public in 1998, including the past 51 consecutive quarters.

That streak isn't likely to end anytime soon. That's because the company has $8.4 billion of primarily fee-based growth projects under construction that should enter service through the end of the decade. That's up from $5.3 billion in projects at the start of the year thanks to several recent additions to the backlog. Meanwhile, it has more projects under development, which should keep it growing for the next several years.

In addition to clearly visible growth, Enterprise has a rock-solid financial foundation. Not only does the company generate very consistent cash flow since 92% comes from stable fees, but it retains a portion of it (usually around 20%) to finance growth projects. It combines that cash with a healthy balance of debt and equity to fund growth, which has kept its leverage ratio toward the low end of its peer group range. That's one reason why it has the highest credit rating among master limited partnerships.

Needless to say, Enterprise Products Partners isn't flashy, but the company has been a dividend growth machine over the years. Meanwhile, with a strong financial foundation and a clearly visible growth pipeline, it still has plenty left in the tank.

You can practically taste the Muzak

Rich Smith(Macy's): Is there anything more boring than a department store? As a husband who's been dragged on his fair share of shopping trips to the mall, I'm inclined to answer "no." But here's the thing:As a head of household responsible for keeping track of the credit card bills and monitoring where my family's personal share of consumer spending flows into the American economy, I'm also beginning to wonder if Macy'sdepartment store is a stock that proves boring is beautiful.

Priced at just under $9 billion in market capitalization, Macy's is not a terribly expensive stock. Even factoring net debt of $5.6 billion into the equation, Macy's stock still sports an enterprise value under $15 billion. At the same time, Macy's generates annual free cash flow of $1.2 billion -- nearly twice its reported net income and enough cash to give the stock a temptingly low enterprise value-to-free cash flow ratio of just 12.2.

Examining Macy's stock from the perspective of a value investor, I believe that Macy's robust 5.1% dividend yield justifies nearly half the EV/FCF valuation on this stock. Meanwhile, analysts quoted on Yahoo! Finance and finviz.com both agree that Macy's is likely to grow its profits at an above average, 18% annual rate over the next five years. (Mind you, not all data aggregators agree on this point. In particular, I note that over on S&P Global Market Intelligence, the growth estimate for Macy's is a disturbingly low 4%.)

That S&P-posited growth rate, if it proves correct, would seriously dampen my enthusiasm for this stock. On the other hand, if the other sites prove right, and Macy's grows at 18% over the next five years (or indeed, anywhere near that fast), this stock could prove to be an incredible bargain -- and demonstrate for investors just how beautiful boring can be.

10 stocks we like better than PfizerWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Pfizer wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017

George Budwell owns shares of Pfizer. Matt DiLallo owns shares of Enterprise Products Partners. Rich Smith has no position in any stocks mentioned. The Motley Fool recommends Enterprise Products Partners. The Motley Fool has a disclosure policy.