1 Big Reason Caterpillar Inc. Stock Jumped 10.2% in April Despite a Lower EPS Outlook

What happened

April was, by far, the kindest month for Caterpillar Inc. (NYSE: CAT) investors this year, as the heavy-machinery maker's first-quarter report sent its stock soaring 10% to fresh 52-week highs. The company not only smashed analysts' expectations, but also raised its revenue and adjusted earnings-per-share guidance for the full year. What matters to shareholders, though, is its GAAP EPS. Interestingly, Caterpillar downgraded its full-year EPS guidance -- something that the market chose to overlook, but for a big reason.

So what

With Wall Street divided over Caterpillar stock after its dazzling run since the election, investors were awaiting the company's Q1 numbers to guide their course of action. Caterpillar didn't disappoint, as highlights from the report reveal:

- 4% higher revenue; also Caterpillar's first year-over-yearsales growth in 10 quarters

- Twofold jump in adjusted earnings (excluding restructuring costs) to $1.28 per share

- 2017 revenue guidance upgraded by 5% at the midpoint

- 2017 adjusted earnings forecast raised to $3.75 from $2.90 per share

Image source: Getty Images.

That's undoubtedly a good set of numbers from a company that has been struggling for several years, but Caterpillar also downgraded its 2017 EPS forecast to $2.10 from $2.30 at the midpoint of sales, citing "significantly" higher restructuring costs as the reason. Caterpillar now projects that its restructuring costs will amount to $1.25 billion this year, compared to its previous expectation of $750 million.

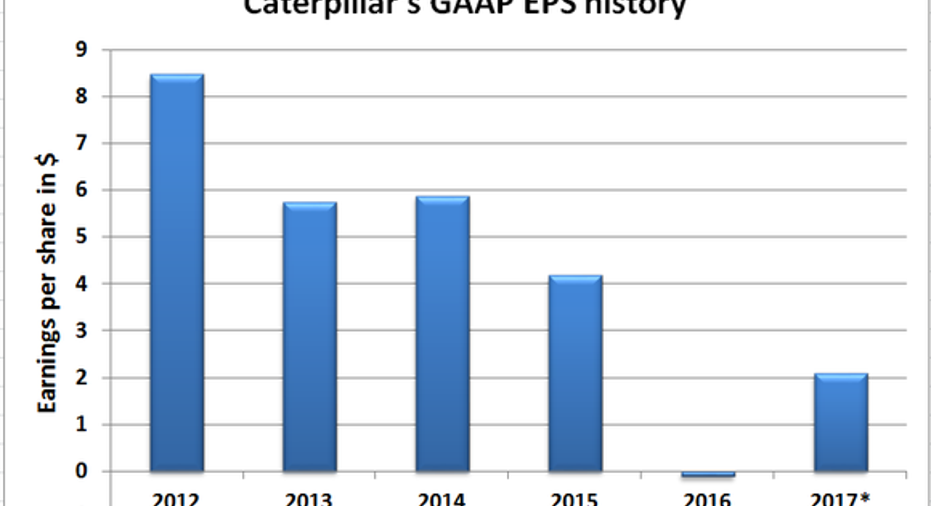

This ongoing aggressive restructuring suggests that end markets aren't strong enough, which is why the company is still cutting costs to boost margins. So why didn't the market pay any heed to this, nor to Caterpillar's EPS downgrade? This chart might reveal the answer:

Data source: Caterpillar financials. Chart by author. *2017 per Caterpillar's projections.

Do you see how good Caterpillar's projected 2017 EPS of $2.10 suddenly appears when compared to its 2016 losses of $0.11 per share? Not surprisingly, investors didn't care about the EPS downgrade and chose to bid the stock up. The question now is: Are Caterpillar's fortunes really turning around?

Now what

There's another important takeaway from the above chart: Caterpillar's projected EPS is just about one-quarter of what it earned at its peak in 2012. Back then, it was strong demand for heavy machinery -- especially from the mining industry just after the top of the commodities boom -- that pushed Caterpillar's sales and earnings higher. Fast-forward to last quarter, when Caterpillar credited aftermarket sales, as opposed to demand for equipment, for its 4% revenue growth. Clearly, end customers are still wary of purchasing new machinery, and are instead paying out for repairs, rentals, and used equipment.

On the flip side, aftermarket demand has traditionally been a leading indicator of recovery in equipment markets. Moreover, it isn't Caterpillar-specific: Companies across the industry reported high aftermarket sales in the past quarter. Cummins, for instance, which serves several common industries with Caterpillar, credited strong aftermarket demand from miners and the oil and gas sector for the 9% growth in its power systems revenues last quarter.

One conclusion I can reach based on these facts is that business conditions are, finally, improving for Caterpillar. The recovery, however, could be slow due to several factors, including the recent price slides of iron ore and oil. Unless commodity prices stabilize, oil and gas companies and miners will likely postpone big projects, and put off any related investments such as in heavy machinery. Remember, the energy and transportation markets in particular are crucial for Caterpillar, and their health will have a big impact on its ability to navigate a turnaround.

The biggest potential catalyst lurking over the horizon -- anticipation of which has already played a major role in lifting Caterpillar shares -- is the infrastructure spending plan that President Donald Trump has promised. When that might arrive, or what it will look like if it does, is anyone's guess. And the fact that Caterpillar management itself hasruled out any material impact from such infrastructure spending on its business until at least 2018 is something the company's bulls can't afford to ignore.

I'm not surprised that investors have found hope in Caterpillar's Q1 report, but going by the company's projections, 2017 will be its one of its worst years ever in terms of net profits. Given the stock's strong rally in recent months, I'd be cautious; I don't expect much upside in Caterpillar shares in the near term.

10 stocks we like better than CaterpillarWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Caterpillar wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017

Neha Chamaria has no position in any stocks mentioned. The Motley Fool owns shares of and recommends Cummins. The Motley Fool has a disclosure policy.