Better Buy: Silver Wheaton Corp vs. Royal Gold, Inc

Silver Wheaton (NYSE: SLW) and Royal Gold (NASDAQ: RGLD) are among the top stocks to invest in if you're seeking exposure to precious metals. That's because both are "streaming" companies: They buy gold and silver production from miners at a fixed price in exchange for the upfront funding they need to operate a business model that has proved more lucrative than traditional mining as Silver Wheaton and Royal Gold can buy gold and silver at low prices without bearing any of the expenses associated with the capital and labor-intensive business of mining.

What's more, both Silver Wheaton and Royal Gold are among the top metal streaming companies in the world. Silver Wheaton is, in fact, the world's largest precious metals streaming company.

Image source: Getty Images

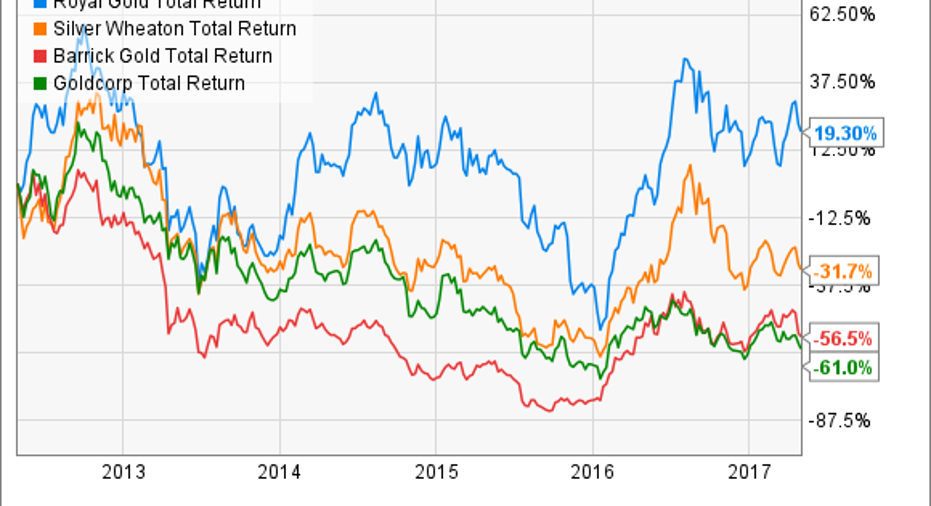

There's a key difference between Silver Wheaton and Royal Gold, though: One is more leveraged to silver and the other to gold, as their names reflect. A larger exposure to the yellow metal is, perhaps, one of the reasons why Royal Gold's stock has crushed Silver Wheaton in recent years. That both stocks -- despite Silver Wheaton losing substantial value -- have outperformed their pure mining cousins Barrick Gold(NYSE: ABX) and Goldcorp (NYSE: GG) isn't surprising given the high-margin nature of the streaming business.

RGLD Total Return Price data by YCharts

Silver Wheaton's dynamics, however, have changed dramatically in recent years: The company now expects gold to make up 45% of its production through 2021. Does that mean investors are better off buying Silver Wheaton stock now, or should they stock with Royal Gold? It's a tight call, but one metric makes Royal Gold a clear winner.

Silver Wheaton is facing a problem

From an operational standpoint, investors in Silver Wheaton and Royal Gold don't have much to complain about, what with both companies wrapping up their fiscal 2016s with record production and revenues. But there's something worrisome going on at Silver Wheaton: Its silver production is trending downward, so it was only its gold streams that drove its silver equivalent ounces higher last year.

Neither of these companies has any control over production because they buy gold and silver from the actual mine operators. If production at those third-party mines declines, streaming companies suffer -- and that's exactly what's happening to Silver Wheaton. For example, silver production from Goldcorp's Penasquito mine which is also Silver Wheaton's primary mine -- slipped 25% during the fourth quarter because of lower grade ore. Silver Wheaton's streaming agreement with Goldcorp entitles it to 25% of the silver produced for the life of mine.

Silver Wheaton even boasts an enviable list of partnerships, but the problem is that some of its existing streams are either nearing expiration or facing hurdles like Barrick's Pascua-Lama mine, where work was halted by the Chilean government over environmental issues. This may have compelled management to focus on gold instead. However, Silver Wheaton is almost entirely dependent on Vale's Salobo mine for gold, and its oncoming gold stream may not suffice to offset the losses from declining silver production elsewhere. How else do you explain Silver Wheaton's muted average production outlook of 29 million silver equivalent ounces for the next five years when its production was a little over 30 million ounces in 2016?

If you trace the trends in profits and cash flows, you also realize that Silver Wheaton has experienced greater volatility than Royal Gold over the years.

RGLD Net Income (TTM) data by YCharts

Note that sharp drop in Royal Gold's 2016 free cash flow is because the company invested in several new streams, and not because of a decline in profits. The volatility in Silver Wheaton's cash flows explains why its dividend policy is so different from Royal Gold's. And that's exactly where Royal Gold handily beats Silver Wheaton.

Royal Gold scores high on dividends

Silver Wheaton pays out a quarterly dividend that equals 20% of its average operating cash flows for the trailing four quarters. While this policy of linking dividends to cash flow has a higher return potential than a traditional miner offers think Barrick, which finally increased its dividends by 50% earlier this year after several years of low or reduced dividends -- it also means Silver Wheaton's payouts can be unstable.

Royal Gold, on the other hand, pays dividends much like a miner, but its dividend streak is among the best in the gold industry: It has increased its dividend for 16 straight years, growing it at a solid annual compounded clip of 20% since 2001.

Image source: Royal Gold's presentation at the European Gold Forum, April 2017.

Foolish takeaway

From a valuation standpoint, Silver Wheaton is trading cheaper at 15 times price-to-cash flow versus Royal Gold's 19 times P/CF, but given that Silver Wheaton's cash from operations has declined during the past five years at a time when Royal Gold has grown its own by almost 50%, I'd bet my money on the expensive stock any day. I'm not suggesting Silver Wheaton isn't worthwhile, as management should be able to find ways to boost sales. But Royal Gold offers greater visibility in terms of growth potential and dividends, which I believe makes it a better stock to invest in today.

10 stocks we like better than Silver WheatonWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Silver Wheaton wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of May 1, 2017

Neha Chamaria has no position in any stocks mentioned. The Motley Fool owns shares of Silver Wheaton and Vale S.A. The Motley Fool has a disclosure policy.