5 Things You Didn't Know About Cameco Corp.

If you've invested in uranium stocks or follow the uranium industry, you've almost certainly heard of Cameco Corp. (NYSE: CCJ). It was all set to make the most of an anticipated rise in global demand for nuclear power when 2011's Fukushima Daiichi nuclear disaster cut short its dreams. It has been an uphill battle for the uranium producer ever since, but Cameco not only survived, it grew to become the world's largest pure-play publicly traded uranium stock today.

With that basic background out of the way -- and with Cameco set to report its earnings later this month -- here are five fascinating facts about the uranium giant you may not know.

1. Cameco is the world's largest uranium producer

With nearly 415 million pounds of proven and probable reserves, and 27 million pounds in production last year, Cameco is the world's largest uranium producer in the world. Through its mines in Kazakhstan, the United States, and Canada, the companyproduces nearly 17% of the world's uranium supply.

Uranium fuels nuclear power plants. Image source: Getty Images

In fact, the McArthur River mine in Canada -- in which it holds 70% stake -- is the world's largest and highest-grade uranium ore mine in existence today. Cameco estimates its ore grade to be worth "100 times the world average." In the business of mining, owning high-grade ore mines is, perhaps, the biggest competitive advantage.

2. It won't be easy to dethrone

Cameco might already be the leading uranium producer, but it also has several projects in the pipeline ready to develop that could be pushed to production levels as the uranium market recovers. Key properties include Yeelirrie and Kintyre mines in Australia, and the Millennium deposit in the Athabasca Basin of Saskatchewan, Canada.

While Cameco has scaled back development at all these sites, it has its plans in place to ramp up production from them in line with demand or to replace depleting resources. Put another way, Cameco's solid asset base will likely ensure the company remains at the top of the game for years to come.

3. It was once a gold miner

During the 1990s and early 2000s, Cameco operated a subsidiary called Cameco Gold, which had major stakes in several gold mines including the Kumtor mine of Kyrgyzstan and the Borro and Gatsuurt mines in Mongolia.

In early 2004, Cameco spun off and publicly listed that gold-focused subsidiary under a new name: Centerra Gold. In December 2009, Cameco decided to become a uranium pure play and disposed of its entire stake in Centerra Gold, thus exiting the gold business. Today, Centerra Gold is among Canada's largest gold miners. That gets me thinking about where Cameco would be today had it retained its gold business, especially given uranium's fate -- though I must give credit to the company for the way it kept its head above water after a devastating event turned its industry upside down.

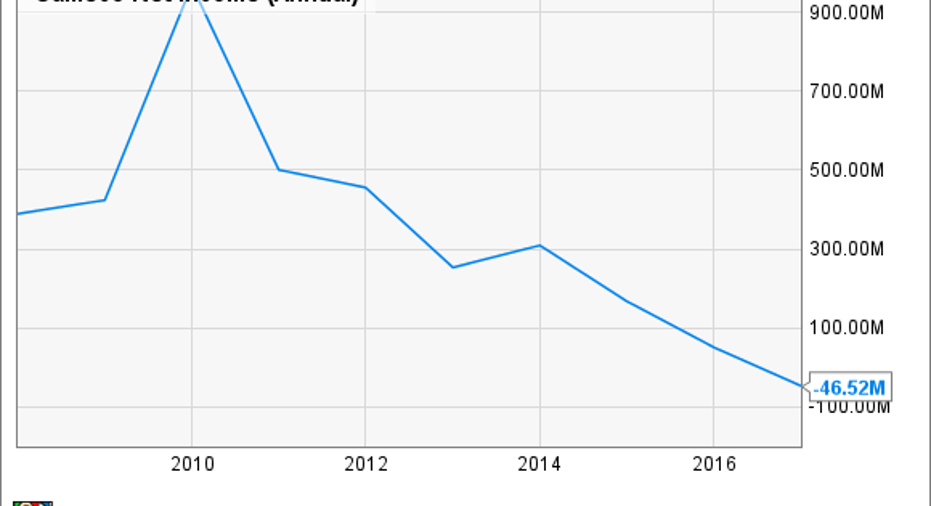

4. It was profitable even during its worst days

Given the enormity of the Fukushima disaster, the consequent shuttering of nuclear reactors in Japan, and the crash in uranium prices, it's incredible that Cameco has remained profitable through the years since -- except for 2016, when one-time impairment charges on production curtailment at its Rabbit Lake operations ate into the company's bottom line.

CCJ Net Income (Annual) data by YCharts

Cameco's track record is, perhaps, the best in its industry, given that smaller players like NexGen Energy Ltd.(NASDAQOTH: NXGEF) and Denison Mines aren't profitable. In fact, mining giant Rio Tinto's (NYSE: RIO) uranium assets, which it owns in the form of 68.4% stake in Energy Resources of Australia Ltd. aren't making any money either. Energy Resources owns here major uranium assets in Australia.

5. Cameco has paid dividends throughout uranium's post Fukushima trough

If Cameco's profit record is admirable, its dividend history is even more impressive. Its free cash flow drifted into negative territory after the industry meltdown, but the company didn't stop paying dividends. It had bumped up its annual dividend by 43% in 2011, but Cameco didn't roll it back. The payout has held steady at $0.40 per share a year ever since.

Of course, Cameco has been paying out more than the cash flow it generates -- a precarious position -- but with its capital expenditures expected to taper off, and a comfortable cash balance for support, the company should be able to maintain its dividend unless uranium prices fall off a cliff.

10 stocks we like better than CamecoWhen investing geniuses David and Tom Gardner have a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

David and Tom just revealed what they believe are the 10 best stocks for investors to buy right now... and Cameco wasn't one of them! That's right -- they think these 10 stocks are even better buys.

Click here to learn about these picks!

*Stock Advisor returns as of April 3, 2017

Neha Chamaria has no position in any stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.